An accounting cycle is defined as the entire set of processes and methodologies performed within an accounting period. However, commerce is quite complex, and learners need definitive guidelines, which they can get via this article’s collection of accounting definitions, procedures, and tutorials.

Origins of the Procedures and Processes

The origins of the accounting cycle can be traced to the Renaissance Era (14th - 16th century) through the works of an Italian Franciscan friar by the name of Luca Bartolomes Pacioli.

The bookkeeping instructions were included in Fray Pacioli’s book The Summa, which contained 36 chapters about bookkeeping. It was not introduced as an accounting discipline but as part of mathematical procedures, which merchants could utilize in monitoring their assets, liabilities and investment exposure (capital).

It basically involved the acts of journalizing, posting and balancing the journalized entries in the ledger by way of the double-entry system of recording. However, the procedures culminated with the trial balance preparation since trading during those days was not as complicated as it is today.

The current accounting cycle has progressed beyond the day book, the journal, the ledger and trial balance, which the Franciscan friar devised during the Renaissance Era. Readers will gain insight about the factors that gave rise to the evolution of Fray Pacioli’s bookkeeping system by reading these articles that tell about historical developments in the field of American commerce:

- Performance Management: Its Origins and Measurement

- Significant Developments That Brought Changes to Operations Management

- Past Value of the Dollar and Causes of Change

- Why Natural Monopoly is Regarded as a Necessary Evil

Learn more in this collection of accounting definitions, procedures, tools, methodologies and other related information. Gear-up for a comprehensive exploration of the basic steps being performed and completed as a cycle by starting with the following articles:

- Explaining the Accounting Cycle Flowchart

- Misconceptions about the Accounting Cycle

- Why Follow the Accounting Cycle?

Where Does It Start?

The cycle starts with the identification process. This task refers to the act of identifying if a transaction is attributable to the business organization. It should be properly established that it is not a transaction or matter pertaining to personal deals entered into by the business owner or of a company officer.

To perform this accounting procedure, there should be a source document from whence the details of the transaction are extracted. These are also known as supporting documents since it is important for a transaction to be legal, appropriate and valid as evidenced by written or documented proof. Know the different types of source documents used in identifying a transaction as well as the information required.

- An Overview of Accounting Source Documents

- Understanding the Features of a Check

- What Info Should a Donation Receipt Include?

- Sample Bill of Sale Forms & Templates

- Important Information Found in an Invoice – How to Create an Invoice

- For How Long Should Source Documents Be Retained ?

After identifying a transaction as one that is attributable to the business, the next important step is to analyze the result. What accounts are affected? Which of the affected accounts will be debited and which one will be credited ? Will it have an increasing or decreasing effect?

However, the analysis process is not as simple. There are accounting principles that should be carefully considered when analyzing transactions. These are (1) Revenue Recognition (2) Matching Principle (3) Cost Recognition (4) Going Concern and (5) Conservatism.

1. Revenue Recognition

Revenue recognition principle pertains to income that is recorded in the books of accounts once the goods have been delivered or the services have been rendered. This is regardless of the payment conditions, to which the actual receipt of cash may take place on the day of delivery or on some later date or even after the accounting period.

Income transactions also have to be analyzed if they are for the current accounting period or if they include incomes that are still unearned. Learn more from the following articles and be steered in the right direction when analyzing revenue transactions::

- What Is Accrued Revenue?

- The Revenue Recognition Principle: Explanation & Examples

- Various Methods of Revenue Recognition

- A Guide to Accounting for Revenue Earned in a Prior Period

- Revenue Recognition Principle vs. Matching Principle

- Journal Entry for a Prepaid Liability – One of Several Methods to Recognize Revenue

- Unearned Revenue: Examples & Explanation

- Accrual Basis vs. Cash Basis Accounting: What’s the Difference if the Business Uses One or the Other?

2. Matching Principle

This principle serves as the guideline in determining the expenditures to be recorded in an accounting period. Similar to the revenue recognition principle, the matter of analyzing costs likewise includes the evaluation of expenditures that are current or prepaid. There is also the matter of determining whether or not goods or services acquired via credit deals should be recorded as outright expenses.

In adhering to the principle of matching revenues against costs, there is much emphasis in recording only the costs that were incurred in relation to the generation of income. Otherwise, the accounting entries should put into effect the capitalization of costs or recognition of an asset account. This is in view of the future years’ benefits that can be derived from the cost incurred.

Be guided by the explanations set forth in these articles:

- The Matching Principle: Explanation & Examples

- The Importance of Matching Principle in Accounting

- What Are Period Costs in Accounting?

- Product Costs versus Period Costs

- Actual Examples of Explicit Cost

- Accounts Payable vs. Accrued Expenses

- Examples of Production Input Costs or Manufacturing Overhead Costs

- What Is the Difference Between Cost and Expense?

3. Cost Recognition

This accounting rule pertains to the recognition of historical cost as the value by which a capitalized asset should be recorded. Whether tangible or intangible, fixed assets that pose future years’ benefits are being presented in the balance sheet based on its acquisition costs. Learn more from the following articles about analyzing transactions based on this concept. In most cases, this requires accounting entries for cost allocations via depreciation or amortization:

- What is the Historical Cost Principle?

- Comparing Historical Cost Accounting with Alternative Methods

- Generally Accepted Accounting Principles for Cost Capitalization

- Acquisition of Fixed Assets

- Accounting Rules of Fixed Assets

- Understanding Intangible Fixed Assets

- Depreciation of Fixed Assets

- Difference Between Amortization and Depreciation

4. Going-Concern

This principle addresses issues pertaining to long-term assets, long-term liabilities, and how they form part of the company’s capitalization fund while operating as a going-concern. The basic assumption when analyzing is that all transactions entered into by a business entity are geared toward long-term objectives to prolong an entity’s legal and sustainable existence.

- Saving vs. Investing: What’s the Right Balance?

- Understanding Accounting for Stock Transactions

- Capital Losses and Tax Deductions

- What Are Long-Term Liabilities?

5. Conservatism

This principle governs transactions based on cost estimates but only to keep the account balances closer to the real state of affairs. Examples of these are the accounts receivables already recorded as income. Since some accounts are no longer collectible, such accounts merit valuation entries to reflect a more realistic income . Otherwise, reports could mislead financial statement readers when making business decisions. Perceive the importance of this principle in analyzing business transactions by reading:

- Allowance for Doubtful Accounts: Examples and Explanation

- Got Bad Debts? Learn How to Write Them Off

- How Financial Distress Affects the Book Value and Market Value of Liabilities

Analyzing Special Accounts

There are various types of industries, which require different approaches in analyzing transactions. Several articles have been rounded-up to serve as guides on how to evaluate special transactions:

- Fund Accounting Guidelines for Non-Profit Entities

- Trust Accounting Basics Explained

- Pension Accounting: IFRS vs. US GAAP

- Basic Grant Accounting Standards

- How to Correctly Post Internal Service Funds

Journalizing

After the transaction has been analyzed, the accounting entries are journalized in the General Journal book. The latter serves as the master record of all explanations, entries and references of the amounts posted in the General Ledger.

The use of accounting software makes this function easier to perform as it automatically generates the accounting entries. Nevertheless, it is best if the person handling the bookkeeping functions ascertains that the generated entries are accurate.

Here are some resource materials that provide examples of how entries are journalized:

- Typical Examples of Journal Entries

- Sales Rebates: Examples of Journal Entries

- How to Make a Guaranteed Payments Journal Entry

- How to Make Journal Entry for Outside Payroll Services

Posting the Entries to the General Ledger (GL)

This is the second to the last step of the bookkeeping process; hence, due care and diligence should be applied when posting the entries. The general ledger is best kept as error-free as possible since it is often referred to as “the book of accounts” and mirrors the recording methodologies of a business entity.

An immaculately maintained GL book denotes that proper accounting procedures are being observed through the use of certain accounting tools like T-accounts and trial balance. Get tips and guidelines from the following articles on how to keep the GL balanced and free from alterations:

- Explaining T Accounts with Working Examples

- Tutorial on How to Create Templates for T-Accounts

- Preparing a General Ledger

- Basics of a General Ledger

- Lost on Account Reconciliation ?

- How to Reconcile Accounts Payable: GL Balance vs. Subsidiary Ledgers

- General Ledger Applications That Will Make Your Life Easier

- General Ledger Templates for MS Excel

Keeping the GL Book Balanced

Proving the GL balances is the final step in the process of recording accounting entries but not necessarily the culmination of the present-day accounting cycle. It makes use of the accounting tool known as the trial balance in order to prove the equality between the total GL debit balances and the total GL credit balances. Know the significance of this tool and get tips on how to go about the process of proving the totals via these articles:

- Guide to Preparing a Trial Balance

- Importance of a Trial Balance in a Financial Statement

- What a Trial Balance Doesn’t Tell to Prove Accuracy of Financial Data

Closing the Book at Year-end

The set of bookkeeping steps and procedures begins with identifying, continues on to analyzing, journalizing, posting and then ends by proving the equality of the GL balances. These actions are repeated as a sub-cycle throughout the entire accounting period. On the final month and before the year ends, preparations for the closing of the GL books take place.

Pre-closing Adjusting Entries and Post Closing Entries:

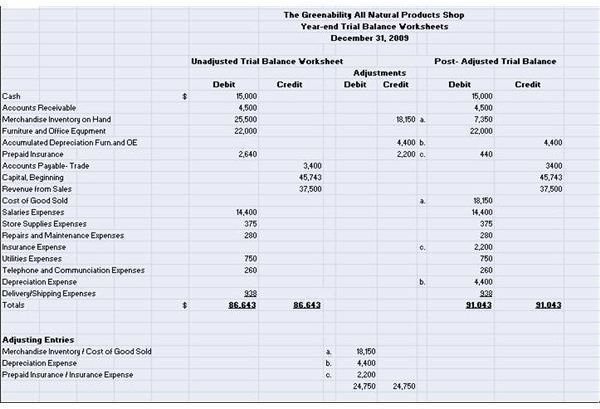

The so-called pre-closing adjusting entries will be formulated and created to take care of proper revenue and expense recognition for the entire year of operation. Reflect on the accounting principles discussed in the earlier sections and find out how the concept of accrual is addressed at year-end by delving into these articles:

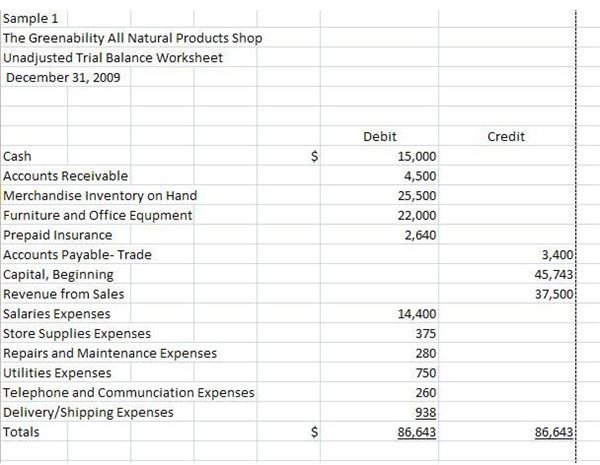

- Ensuring a Balanced GL by Preparing an Unadjusted Trial Balance

- Importance of Adjusting Journal Entries

- Detailed Examples of Adjusting Entries

- Adjusting Entries: Bringing Accuracy to Financial Statement Figures

- Reconciling Inventory Accounts With Adjusting Entries

- Calculating the COGS Formula

- Misconceptions About Adjusting Entries

The Final Stage

Winding up the year’s transactions:

The year has ended and every loose end is about to be tied-down by proving the equality of the general ledger balances one last time. The income and expense accounts are about to be zeroed-out and the real accounts will be forwarded to the incoming year’s new book of accounts. Once all these finishing touches have been completed, then the final stage is set for the preparation of the business entity’s financial statements.

Financial Statements Preparation

All things considered and when the general ledger book balanced, the final step is to prepare the balance sheet, the income statement, the statement of owner’s capital or stockholders’ equity, and the cash flow statement. Study the instructions featured in the following articles, which provide walk-through tutorials for financial statement preparation:

- An Example of a Basic Balance Sheet

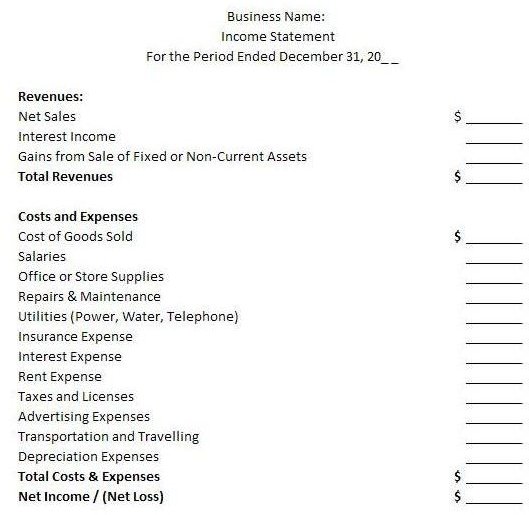

- Income Statements: Free Template and Example

- Sample Statement of Owner’s Equity

- Cash Flow Statement Sample & Explanation

- A Study Guide to Financial Statements Basics: Related GAAP Rules, Formats and Analyses

- Illustrated Examples of a Worksheet for Adjusting and Closing Entries for Trial Balances

References

- Image: Ledgers made at Cowans, Edinburgh by Edinburgh City of Print under CCA-SA 2.0 Generic.

- Image: Revenue Growth by Anup Sankaran under public domain.

- Image: In The Days Before Microsoft Excel Expenses Were Done Like This . Old expense accounts dating from 1964 litter the ground around the now derelict by Steve Reeves under CCA-SA 2.0 Generic

- Image:Jacopo de’ Barbari - Portrait of Fra Luca Pacioli and an Unknown Young Man - by Web Gallery of Art (#1269) under public domain.

- Image: VA EA Repository Introduction EA information is collected from various business and project source documents by va.gov under public domain.

- Screenshot images of trial balance , year-end worksheet and income statement template were created by the author.

- Image: Expenses by Author Unknown under public domain.