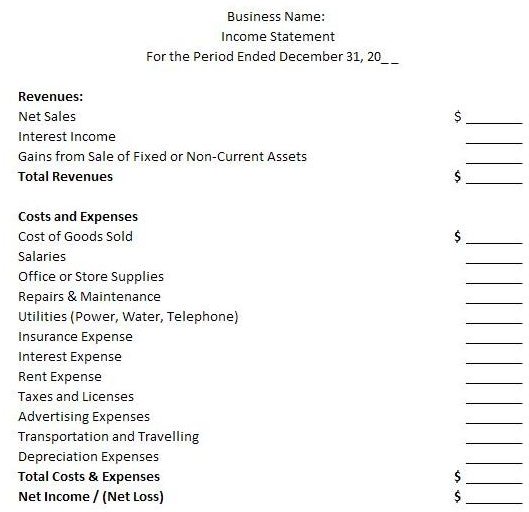

Provided in this article is a free Income Statement template in the Single-Step format, often used for businesses employing basic income and expense accounts. Be guided on how to complete the Income Statement’s fields with examples and explanations about each account and what it includes.

Income Statement Definition

An Income Statement is a summary of all revenues and expenses related to business activities whether actively or passively gained or incurred, collected and recognized within a specific accounting period, where the difference between the revenue and expenses is reflected as the result of its operations. Results may be positive or negative and it presents a measure of performance for the business as a whole. A positive result is called Net Income while a negative outcome is labeled as Net Loss.

As we proceed to the succeeding sections that provide the guidelines on how to prepare the Income Statement, it would be best if you secure a copy of the free income statement template to serve as your reference. The sample can be downloaded at Bright Hub’s Media Gallery: Free Income Statement Template: Single-Step Format.

Guidelines on How to Prepare the Income Statement

Financial Statement preparation is the final step of the accounting transaction cycle as the financial reports represent the final summary of the General Ledger accounts. It is important that accounts are arranged and organized in a report form, since this will be utilized by different users who may be internal or external to the business entity.

In preparing the sample income statement featured in this article, it is presumed that the figures used were all proven and balanced in the year-end Trial Balance Worksheet where post adjustments and post closing entries were already applied.

Basic Information

(1) The first line of the heading should be properly labeled using the business name and not the name of the proprietor, to distinguish the summary of income and expense transactions as those that are related only to that particular business’s operations.

(2) The second line of the heading should be properly identified as Income Statement or other appropriate titles by which it is known, i.e.: Statement of Income and Expenses, Profit and Loss Statement, Profit & Loss Summary, Statement of Revenues & Expenses, Statement of Net Earnings and all other appellations used that are synonymous to Income and Expenses.

(3) The third line of the heading is the year-end date of a particular accounting period. There are two types of accounting periods observed by businesses, (a) Calendar Year and (b) Fiscal Year. Your choice should be based on what is most suitable to the nature of your business operations. In some cases, interim Income Statements are prepared, and these refer to the revenue and expense reports prepared even before the calendar or fiscal year is completed.

The Calendar Year is commonly used to conform with the traditional 12-month period starting from the month of January up to December; hence, most income statement date lines are captioned as “For the Year Ended, December 31, _ _ _ _.”

The Fiscal Year becomes applicable if the business operations commence and end according to a period dictated by regulations, i.e. educational institutions, whose starting and closing months are based on the school year opening and closing of the region or country they operate in.

You will further note that it is different from the Balance Sheet date captioned as, “As of December 31, _ _ _ _”, in as much as the values being reported in this statement represent the balance from the business’s inception date up to the most recent year end. As opposed to the Income statement, where the values presented are only for a specific period.

Revenue

The first component of the Income Statement is Revenue, which refers to all sales transactions consummated whether in cash or on credit terms, received or extended to customers. Revenues also include monies received coming from business-related sources, realized or gained from capital investments.

Others prefer to be more specific by using the caption Gross Revenue or if there are no other sources of income to report, Gross Profits or Gross Sales or Gross Income or Gross Collections.

- If there are several sources of income, they will be classified into sub-components described according to the nature of the industry activity. Wholesalers, retailers or any industry involved in selling or trading commodities use the term Sales, since this activity is the main mode of income generating activity. The important thing is to aptly describe the nature of the business operation, e.g. Rental Income, Professional Fees, Services Fees among others, just to mention a few.

Please continue reading on to the next page for more guidelines on what to include in each account.

Continuation of Guidelines on How to Prepare the Income Statement

Revenues:

-

In our free Income Statement template using the Single-Step format, the revenue from sales is immediately presented as Net Sales, without going into details as to what was deducted in order to arrive at the net figure. Usually, the total amount of Sales Returns and Allowances, as well as the total amount of Sales Discounts granted during the year, are deducted from the total Sales to arrive at the Net Sales presented in a Single-Step Income Statement.

-

Related income realized and earned by investing or depositing the business funds in income generating accounts or investment instruments, is also a sub-component of the Revenue item. the aim is to distinguish them as secondary revenues from the main or primary revenue source. This is quite important, especially if income taxes have been previously withheld upon receipt of the proceeds. In doing this, the IRS return can be easily reconciled with the Income Statement .

Advertisement -

However, if you have to submit financial reports specifically required as strictly prepared according to GAAP standards, it may be necessary to prepare a different set of financial reports based on US GAAP guidelines. Income earned from fund deposits or investments are reported as part of income from operating activity under GAAP’s reporting standards.

-

The same is true with the matter of realizing gain from sale of fixed assets that were retired or replaced and this item is a bit tricky or more complex. Whereas IRS would prefer this type of income to be classified and specified in the financial reports submitted as attachments to an entity’s tax returns, GAAP rules specifically prohibit realizing gain from sale of fixed assets. Due care should be exercised in presenting Income Statements if you have this kind of transaction, especially if the gains involved are substantial.

Advertisement -

IRS is interested with income derived from selling fixed assets, in order to collect the tax due, while GAAP standards on the other hand are concerned in preventing the use of such transactions to bloat the reported income of an entity.

-

Income accounts normally carry credit balances; hence, a Net Income although positive in concept will be imputed on the credit or right side of the basic accounting equation Assets = Liabilities + Capital. A credited entry to the Owner’s Equity or the Retained Earnings of the Stockholders’ Equity will produce a positive effect which is increment. It follows therefore that Net Loss will be recognized if the outcome of the income report is a debit balance and will still be imputed in the appropriate Capital account. A Net Loss, will have a reducing effect on the equity accounts via a debit entry.

Advertisement

Costs and Expenses

The Costs of Goods Sold account includes all the expenses incurred and clearly identified as directly related in acquiring the merchandise traded or sold. Similar to the revenue component, the title can be modified in order to aptly describe the nature of the business activity, i.e. Cost of Services Rendered.

Included under the Costs of Goods Sold account are the actual amounts paid for the merchandise upon purchase and net of discounts, the delivery fees, freight charges, the direct labor, material and overhead costs, if the products sold were internally manufactured. However, since this is an Income Statement in single-step format, the more complex method of presenting costs of goods sold is not necessary since this type of income statement presentation is used for simple business processes.

Salaries are reported at gross and the related accounting entries will take care of reporting all other costs related to adjust the salary expenses against all deductibles like SS and insurance premiums, withholding taxes, cash advances and the likes.

Office and store supplies are considered expendable items, which mean they are immediately recognized as expenses upon purchase. However, there is still the need to maintain subsidiary ledgers to monitor additions and issuances for control measures.

Repairs and Maintenance expenses refer to all minor costs related to fixed assets, including housekeeping necessities of the business premises. If there is substantial diversity in the maintenance costs of fixed assets, it would be best to provide subsidiary ledgers to monitor the repairs and maintenance costs of the fixed assets that have the most contribution or the most frequently incurred expenses.

In line with this, some expenses inuring to the reconditioning, improvement or enhancement of some fixed assets or non-current assets may have to be capitalized. The need to allocate an expense will arise if only a portion is attributable for the current year while the rest will benefit the business through future years’ use. Please refer to a separate article entitled GAAP Rules for Capitalizing Costs for more guidelines pertaining to Repairs and Maintenance expenses that require capitalization in the books of accounts.

Final Page for Guidelines on How to Prepare the Income Statement

Utilities refer to the costs incurred to pay the energy, water and communication facilities used for the business premises. However, if the business makes use of renewable sources, it would be best to classify the cost of fuel material used as Fuel, Oil and Lubricants.

Insurance expenses, which should include premiums paid for insurance policies that cover the business premises and/or the goods covered by the policy. As a rule, this item is initially taken up as a prepaid item upon acquisition and the related expense will be recognized at year-end through the post closing adjusting entries. The principle of matching costs against revenues dictates that only the portion of the prepaid insurance incurred during the period will be recognized as deductible expenses against the reported income.

Rent Expense refers to those that are related to business operations. Due care should also be recognized when passing entries for this account if the transaction involved called for rental expenses. Clearly identify the purpose for which the rent was incurred in order to properly classify the expense account; if it forms part of an employee’s benefit or incidental to a project, then the rent expenses should be classified accordingly.

Advertising Expenses may also require the same rules that apply to expenditures that were prepaid especially if the amount involved is material and can affect the resulting outcome of the income statement. Otherwise, they can be treated as outright expenses for the year.

Transportation and Travelling - Transportation costs incurred should have direct relevance to the day-to day operations of the business. Travelling on the other hand may have to take into consideration if the travelling assignment is temporary or indefinite or if income from will be derived from the new location. The nature of travelling expenses should be checked against IRS 463 to determine the travelling expenses qualified as deductible for tax purposes.

Depreciation Expense, this is the expense account used in recognizing the depreciated portion of a capitalized fixed asset. The amount of depreciation will be computed based on GAAP recognized methods, namely straight-line, declining balance and sum-of the-year’s digits. For more information on how to compute depreciation expenses according to the different methods, the reader may refer to a separate article entitled Types of Depreciation .

There is also the matter of taking into consideration the limits allowed by IRS for depreciation expenses, which you can refer to under IRS 946 . In this aspect, the IRS is more concerned with appropriate amount to take-up as expenses and not so much on the method used to compute for depreciation.

Income Statement and the Conflicts between IRS and GAAP Rules

The IRS acknowledges the fact that there are GAAP rules that are in conflict with Internal Revenue Codes (IRC) but this does not mean that adherence to one should violate the other. Most differences lie in the matter of income recognition, inventory valuation and cost recovery methods, all of which are concerned with income and how expenses can affect its recognition.

IRC’s are implemented to ensure that near accurate income will be reported and taxed, in the same way that GAAP standards are provided to serve as guidelines to arrive at near accurate income and net worth as basis for investment decisions. Since both the IRC and the GAAP standards are concerned with near accurate figures, then the breach between the two is not too wide.

A compromise can be arrived at by preparing a separate set of reports for SEC reporting purposes based on GAAP reporting standards, if indeed the resulting differences due to conflicts between the two sets of rules are too material to ignore. Otherwise, minimal differences are not likely to influence the investors’ decision because companies are being gauged not only for profitability but also for stability and efficiency.

Thus in preparing reports to present your revenues and expenses by using our free income statement template, it would be best to heed not only the guidelines we provided but to refer to the IRC and GAAP rules we cited as well.

Reference Materials and Images Credit Section

Reference Materials:

- Income Statement — https://en.citizendium.org/wiki/Income _statement#Income_Taxes

- Create a Profit & Loss Statement— https://www.va-interactive.com/inbusiness/editorial/finance/intemp/income.html

Image Credit:

- Free Income Statement Template - Single-Step created for this article by author CSCantoria

This post is part of the series: Income Statements

Find tips on how to prepare, read and analyze income statements along with examples and free templates you can download for personal or business use.