Unearned revenue, if considered by its title alone, could mislead a learner into treating it as an income account. However, accounting rules dictate that this should first be recorded as a liability. Our explanations and examples focus on this to help the reader understand why and how this is.

How Do You Define Unearned Revenue?

The best way to define “Unearned Revenue” is to delve into the nature of a given transaction and understand the factors that give rise to the creation of a liability instead of income. It is understood, however, that unearned revenue stems from advance payments received by an entity or an individual.

First off, the advance payment received is only a potential profit on the part of the recipient since the transaction cannot be considered as consummated. What was created was a liability because in receiving the money, the receiver becomes liable for breach of contract in case there is failure to deliver or render the goods or services at the time they are promised or expected.

However, the money received will be recorded in the entity’s books according to the nature of the income, for which the business stands to gain as revenues.

Hence unearned revenue is defined as payment or monies received in advance by a person or a business entity from its customers; the act of recognizing the income is deferred, pending the performance or delivery of goods or services. Until such time that the applicable period has lapsed and that the service is considered as rendered, or the actual delivery of goods has been made, only then will the unearned revenue be recognized as income.

Unfortunately, the SEC and the IRS have different interpretations on how this account should be treated to serve their individual purposes. The IRS requires all payments received as taxable whether earned or unearned, while the SEC, which operates under GAAP rules, requires that a company should report as income only those monies that have been actually earned.

To illustrate the accounting treatment for this particular account, the proceeding sections provide different examples of business activities that usually require the collection of advance payments:

Insurance Companies and Premiums

The easiest examples to cite are the insurance premiums paid in advance by a policyholder to an insurance company, usually for a one-year period.

As an insurance provider, the company receives advance premiums from its policyholders, in exchange for the promise of providing the latter assurances that they can recover a portion of any loss sustained as contained in the policy agreement.

The assurance for this coverage is extended by the insurance provider on a monthly basis; hence the policyholder is required to pay premiums computed on a per-month basis but collected in advance by insurance companies for at least a year.

Upon receipt of the payment, the insurance company then becomes liable, and the advance premium payments received will be temporarily lodged under the Unearned Premiums account. The term “premium” best describes the nature of the potential income to be realized in the transaction.

Assuming that all other charges were taken-up in a separate book entry, the accounting entry for the premiums received in advance would be:

Dr. Cash __________ $xyz

Cr. Unearned Premiums __________ $xyz

In each passing month, the Unearned Premiums account would have a correlated entry in order to recognize the part of the premium already earned. The following entry will be taken-up in the books of the insurance company every month-end of the policy coverage, until the entire one-year prepayment has been fully recorded as income.

Dr. Unearned Premiums __________ $xyz

Cr. Revenue from Insurance Premiums __________ $xyz

If the policy holder is satisfied with the services provided by the insurance company, the policy will be renewed and another one-year prepayment will be paid to the insurance company.

Subscriptions for Publications or Advertisements

Companies engaged in providing publications like magazines, digests, or providing spots or spaces for advertisements likewise receive advance payments for subscriptions. It may be on a quarterly, semi-annual, or annual basis. Their liability is to deliver the publication promised on the periods agreed upon; otherwise, the potential income will take actual form as a liability if the customer files claims for refunds in cases of non-delivery or non-provision.

The entry follows the same format but with a different description as unearned revenue.

(1) T_o record subscription fees received in advance_

Dr. Cash __________ $xyz

Cr. Unearned Subscriptions__________ $xyz

(2) To recognize the subscription earned for the month

Dr. Unearned Subscription __________ $xyz

Cr. Income from Subscriptions __________ $xyz

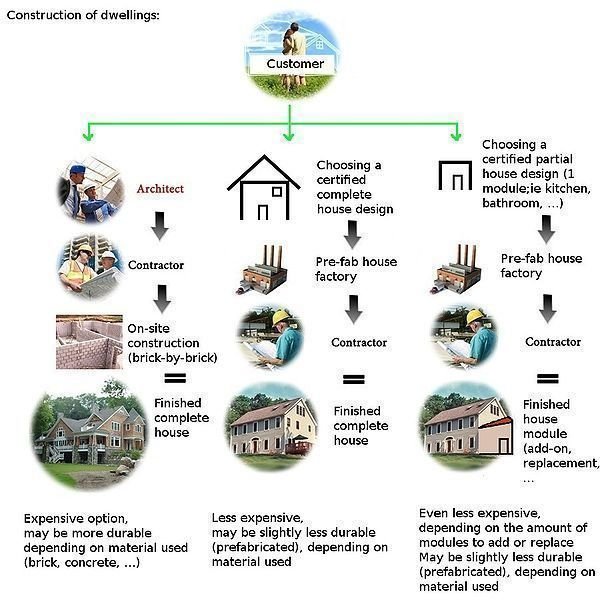

Professional Work Based on Percentage of Completion

A house contractor may ask a homeowner to pay at least 25% of the contract price before construction work commences. Since part of the money will be used to buy construction materials and pay for labor, the deposit received cannot be recognized as the contractor’s income.

The contractor can claim the succeeding advance payment from the homeowner if the agreed portion of the house under construction has been satisfactorily completed. This would mean that the money previously received has been exhausted in order to attain the completion, although a portion of this deposit was already projected by the contractor as his potential income for the completed segment of the construction job.

To illustrate how the unearned revenue is recorded, the following are given as examples:

The contract price for the house is $100,000, 25% advance payment for 25% completion. The 25% advance payment for 25% completion is allotted as follows: $12,000 is for materials, $5,000 for labor, and $3,000 for miscellaneous expenses. This leaves $5,000 free from allotment and thus become the contractor’s potential income from the 25% completion.

(1) Accounting entry to record the advance deposit received:

Dr. Cash __________ $25, 000

Cr. Advances for Cost of Materials and Labor __________ $12,000

Cr. Advances for Cost of Labor __________ $5,000

Cr. Advances for Miscellaneous Expenses __________ $3,000

Cr. Unearned Revenue from Construction Project __________ $5,000

(2) Upon completion of the portion for which the deposit was made, the following entry will be taken-up to recognize the expenses and the earned income:

Dr. Advances for Cost of Materials and Labor __________ $12,000

Dr. Advances for Cost of Labor __________ $5,000

Dr. Advances for Miscellaneous Expenses __________ $3,000

Dr. Unearned Revenue from Construction Project __________ $5,000

Cr. Cash __________ $20,000

Cr. Income from Construction Project __________ $5,000

Note to this entry: Only $20,000 is recognized as reduction against the $25,000 cash originally deposited, as it represents the costs paid for materials, labor, and miscellaneous expenses. The $5,000 balance remains intact as the contractor’s actual income for the 25% completed project.

Summary

Keep in mind that the unearned revenue account is a liability of the person who receives the advance payment and will become actual income only if the services or goods for which it was paid have been delivered.

This should not be confused with prepaid accounts like prepaid insurance, prepaid subscriptions, or advance deposits, since the accounting for prepayment is being done by the person who made the advance payment.

Reference Materials and Image Credit Section

Reference

- US FAAP Accounting Study Guide from CPAClass.com

Image Credits