What are internal service funds and how are they recorded in the general ledger? If your company has multiple departments, chances are these departments perform work or offer products or services to each other. Because these can be expenses and losses, the correct journal entries are necessary.

Defining Internal Service Funds

For the most part, the accounting for internal service funds is utilized more in government agencies where one agency purchases services or products from another. An example might be a federal form supplier selling (or giving) forms to another government agency requiring the forms—both agencies really being under the umbrella of one entity—the government. If you utilize any sort of internal service funds, journal entries must be made accurately in order for your accounting books to be correct.

For the most part, internal service funds are internal expenses and losses—unless the departments categorize them as sales revenues and expenses. Most industries with multiple departments only looking at long-term profit for the company as a whole will keep track of internal service funds with journal entries —even if it’s just for inventory adjusting and losses.

In the auto dealership business, the parts department may offer up cans of brake cleaner to the technician in the service department. However, the parts department posts these cans of brake cleaner as a shop supplies expense where the service department adds the cost of the brake fluid to their customer invoice, making a profit.

Simple Journal Entry

The world of financial accounting is so complex, and missing these types of important journal entries for internal service funds can leave business owners scratching their head—especially if the appropriate revenue isn’t achieved.

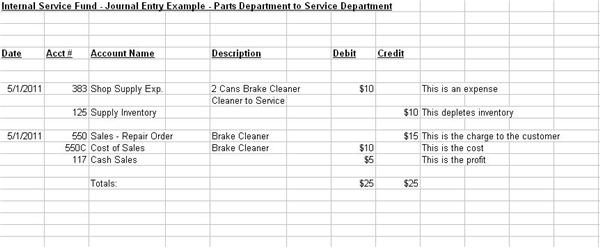

Let’s use our brake cleaner example to show our first journal entry example:

First click on the screenshot to the right to enlarge. Here you’ll see how this transaction works. When the service department requests the shop supply (brake cleaner) from the parts department, the parts department does the following:

- Debits Shop Supply Expenses – This is a parts department expense.

- Credits Shop Supply Inventory – This depletes the inventory.

On the service department side, the journal entry:

- Debits – Sales Repair Orders – The mark-up to the customer is shown on the repair order.

- Credits – Cost of Sales Repair Order – The actual cost of sales for the brake cleaner.

- Debits Cash Sales – The difference between the sales and cost of sales is revenue.

In the above example, while the parts department must look at the brake cleaner as an expense and lower inventory on shop supplies, the service department actually makes a profit on the trade or internal service fund. Keep in mind even internal service funds require debits and credits to equal .

On the other hand, what if each department wanted to make a profit?

Complex Journal Entry

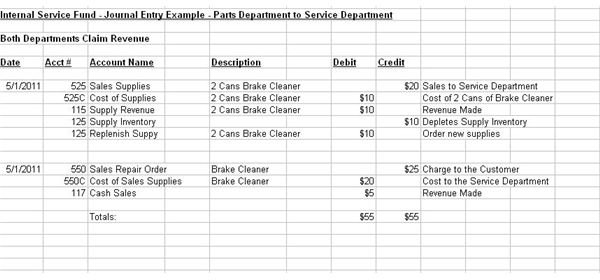

In this internal service fund journal entry example, both the parts and service departments want to show sales revenues. Again, click on the screenshot to the right to see how to post this journal entry .

The parts department:

- Credits sales for shop supplies.

- Debits the cost of the brake cleaner.

- Debits revenue made.

- Credits shop supply inventory.

- Debits new inventory purchase replacement.

The service department:

- Debits the Repair Order or cost to customer.

- Credits the cost of the brake cleaner.

- Debits revenue made.

Important Tips to Remember

With internal service funds, no matter if one department or division makes a profit or not, most internal costs or expenses are discounted at internal rates and have dedicated internal accounts in which these postings appear.

In the business world, if you have more than one division or department, consult with your tax professional to see if making a profit in each department is feasible or if the internal service funds should be aligned as revenue for one and a loss (expense) for the other.

In the long run, business owners want to see profits in every department; however, with internal service funds, journal entries that are incorrect or not recommended may lead to over-stating or redundancy to envision profits to more than one department for something used internally to make the sale in the first place. Further, making a profit internally may not follow the Generally Accepted Accounting Practices (GAAP).

These internal service fund journal entries are a simple way of understanding what these types of funds are and how they should be accounted for in the general ledger.

References

The author has experience as a business owner using internal service funds.

Image Credits:

Accounting cycle - Wikimedia Commons/club oracle

Journal entry screenshots created by author

Pencils - Wikimedia Commons/Dmgerman