In the world of financial accounting you really can’t produce accurate financial statements without a trial balance. What is the importance of a trial balance in financial statements? Jean Scheid offers some insights.

What is a Trial Balance?

The trial balance is part of almost every financial accounting system. It is formed via information from journal entries made into a general ledger, journals or schedules. A correct trial balance means that all the debits and credits equal from those journal entries. If debits and credits do not equal, financial statements such as a profit or loss (income and expense statements) and the balance sheet will be inaccurate and shouldn’t be printed or analyzed because they aren’t accurate.

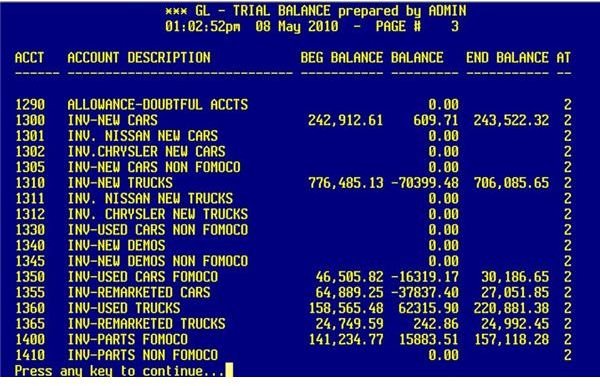

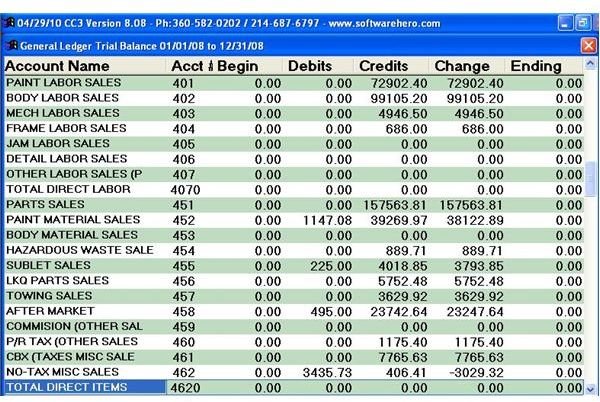

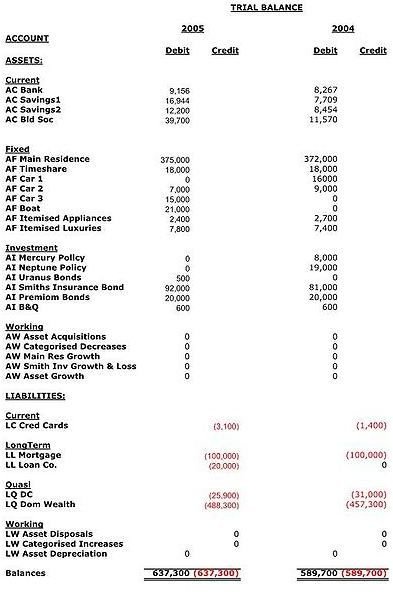

To begin our in depth look into the trial balance, click on the image to the left to see a portion of a trial balance for an auto dealership. In addition, you can download and print a sample trial balance found in our Media Gallery. The sample trial balance in our Media Gallery shows how debits and credits do not equal. To help you better understand why they do not equal, read, Guide to Preparing a Trial Balance .

If you search on the Internet for the importance of a trial balance in a financial statement, unless you’re an accounting expert, you could get lost. After all, if you’re a business owner, when banks or investors ask for your financials they typically mean the balance sheet and income and expense statement and perhaps a cash flow statement. They never seem to ask for the trial balance so why is it even important?

In essence, the lack of a trial balance or a correct trial balance means you are only estimating your income and expenses along with the summary totals on your balance sheet. Even for small or mid-sized companies, it’s impossible to estimate or guess your financial status, unless your business is an all cash business.

What Happens in a Trial Balance?

Let’s take two examples, a summary total from our balance sheet and a summary total from our income and expense statement.

If we look at a balance sheet that had an inventory total of $50,000, what is that $50,000 comprised of? That’s where the trial balance comes in. Here’s a look at journal entries made first in your general ledger:

Date / Description / Debit / Credit

- 5/2 – Write Check 1001 / Debit Inventory $1,000 / Credit Cash in Bank $1,000

- 5/3 – Buy Inventory / Debit Inventory $1,000 / Credit Accounts Payable $1,000

- 5/4 – Sell Widget from Inventory / Credit Inventory $500 / Debit Sales $500

As you can see, all of our debits and credits not only equal in the journal entry, they provide the detail for each transaction made to the inventory account. When this pulls to the trial balance, these journal entries don’t just pull to the inventory account, they affect many accounts. Of the accounts utilized above, your trial balance may look like:

Account Name / Beginning Balance / Balance / Ending Balance

- Cash In Bank $10,000 / $-1,000 / $9,000

- Inventory / $48,500 / $1,500 / $50,000

- Accounts Payable $11,000 / $-1,000 / $9,000

- Sales Account / $5,000 / $500 / $5,500

A closer look will show you that in this above trial balance example, all the debits and credits equal from the journal entry detail pulled to the trial balance. While the trial balance doesn’t show the detail of the journal entries, it can detect if it is out of balance. Upon a further look, for our inventory account that had an ending balance that pulled to our balance sheet of $50,000: We had a $48,500 beginning balance, debits and credits equal a positive $1,500 balance for an ending balance of $50,000.

For the income and expense statement, if we use the same journal entry made above, we see we had a debit to sales of $500:

Date / Description / Debit / Credit

- 5/2 – Write Check 1001 / Debit Inventory $1,000 / Credit Cash in Bank $1,000

- 5/3 – Buy Inventory / Debit Inventory $1,000 / Credit Accounts Payable $1,000

- 5/4 – Sell Widget from Inventory / Credit Inventory $500 / Debit Sales $500

So in the trial balance, our sales account would look like:

Account Name / Beginning Balance / Balance / Ending Balance

- Sales Account / $5,000 / $500 / $5,500

The result of a correct trial balance is that from every journal entry detail that is pulled to the trial balance, if all the debits and credit from those journal entries do not equal, your trial balance will be incorrect. Following that, your balance sheet would have inaccurate summary totals and your income and expense statement would be off perhaps showing an inaccurate profit (or loss).

Why So Important in Financial Statements?

While a financial report like the balance sheet does have its limitations , when it comes to selling your business, finding investors and having an accounting professional prepare your annual tax return, the trial balance is key in finding out if you are in a sense, “cooking the books,” or just making mistakes in your journal entries. The importance of a trial balance in financial statements ensures that the accounting cycle is followed correctly and that every transaction in your business is recorded accurately.

If, for example, in your trial balance, the debits and credits did not equal, the trial balance would show an offset account that revealed the difference in the credits and debits. From there, you would have to research your journal entries, ledgers, schedules or journals to find the errors, make the appropriate journal entries, and re-run an adjusted trial balance.

Only once the trial balance is equal can financial reports be printed that are considered to be accurate.

Some business owners may say, “So what, I’m off here and there?” Those little “heres” and “theres” will go far at year-end, especially when it comes to declaring actual income and expenses. Say your bookkeeper forgot to enter over $10,000 in various expense account ledgers? If you didn’t check your trial balance or even run a trial balance, you wouldn’t get credit for those expenses on your tax return. Further, what if your company was being audited by the IRS or state government agency? These organizations do employ financial auditors who can indeed figure out if you are cooking the books or just making mistakes. We all know that incorrectly reporting income and expenses could result in fines, even hefty fines.

How Is a Trial Balance Run?

Most businesses implement some sort of accounting software system such as Quickbooks , Quicken or other industry-specific software. Once all your journal entries are made for the month or year, a trial balance option is available in your financial reports section.

No matter what the accounting period, month or year, you must run and review a trial balance to ensure accurate financial records. The next time you wonder what is the importance of a trial balance in financial statements, you’ll have the answer. Better yet, you’ll know how those numbers got there and how to review and fix them prior to running your final reports for the accounting period.