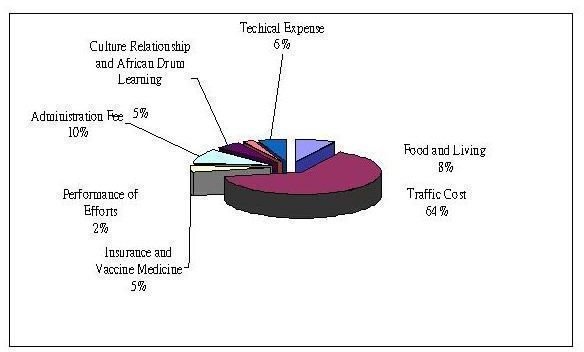

This guide discusses the essentials of non profit management and introduces the concept of cash reserves to the entry-level nonprofit professional. It briefly compares and contrasts the non profit business budget to a traditional business budget.

Nonprofits and the Budgetng Process

Budget development and oversight is a fundamental part of management’s responsibility to oversee and improve operations. Corporate and volunteer organizations alike utilize budget practices to manage financial resources on an annual, quarterly, and even project-by-project basis. (To learn the advantages of forming a corporation, please read “Four Advantages of a Corporation, over other Organizational Forms ). A comprehensive budget will effectively establish and direct spending activity for the upcoming fiscal period. Community donations, telephone expense, and staffing needs are only a few examples of the projections nonprofits consider during the budgeting process. Meaningful budget projections clearly and succinctly represent the organization’s financial objectives for a specific fiscal period. In this article, we will provide a general review of the nonprofit business budget process as well as present any considerations that specifically apply to this federally tax exempt entity.

Image Credit (Wikimedia Commons )

The 501(c)3 Designation

To qualify for the 501(c)3 designation, nonprofit organizations must apply to the Internal Revenue Service (IRS). A not for profit organization receives a 501(c)3 tax exempt designation if the IRS determines they are conducting activities that are charitable, educational, or religious in nature. Once designated tax exempt, most nonprofits are required to report annually any earned income or incurred expenses using Form 990, which is prepared annually. Consequently, the budget plays a vital role in the reporting process as the organization’s financial statements are assembled and published after comparing actual income and expenses to the year’s budget projections.

Preparing The Budget

When preparing an operating budget, nonprofits embark on a thorough and oftentimes painstaking development process. Although nonprofits are expected to create a financial plan that dually represents their service philosophy and the agency’s commitment to fiscal accountability. As with most businesses, the mission statement drives operations; therefore, the final budget must fully support its mission and vision statements.

Comprehensive budget projections include income, expense, and profit (or loss) estimations. Nonprofit organizations, as do profitable organizations, include an income section to represent any revenue projected for receipt in the upcoming fiscal year. However, amounts included here primarily include any approved grant dollars, community donations, or membership fees.

Expenses, conversely, are amounts projected as an outflow of money paid to another person or entity for goods provided or services rendered. Therefore, a nonprofit organization sheltering abused domestic animals might develop a budget that includes revenue received from funders, membership donations as well as any anticipated operational expenses such as veterinarian fees, shelter supplies, and food. (An example of a budget template used by a non-profit can be accessed here ).

Frequently, a nonprofit organization offering several programs and services has indirect costs that apply to more than one program. These indirect, or administrative costs may include professional services, rent, liability insurance, or staff time. Nonprofits often calculate these costs by calculating the percentage of the cost that applies to each program and then uniformly applying the amount based on grant stipulations.

For example, if there is a $100 rental amount charged for an office that houses 3 programs, leadership may determine that 50% of the amount should be allocated to Program A while the remaining 50% will be charged equally to programs B, C, and D.

Any remaining balance that remains once total expenses are subtracted from total income would be categorized as net income (or net loss). Unlike companies that generate traditional sales revenue, nonprofits are primarily concerned with creating cash reserves as opposed to profitability. (Please read “What are the Differences Between Static and Flexible Budgets ” to learn more about issues for profit organizations must consider during the budget development process).

For nonprofits, net income immediately translates to cash reserves that can be used to obtain new equipment or guarantee agency sustainability in future periods. For instance, the Board might decide to improve their financial position by using cash reserves to start an endowment fund, acquire program-essential equipment, or purchase mutual funds.

You can also find help for your nonprofit regarding business plans and by visiting SCORE, a division of the SBA–this organization offers great resources on how to startup, manage, and effectively run your nonprofit , including examples on non profit business budgets.