Managerial accounting entails gathering and analyzing the financial data being used by various departments in formulating their strategies and arriving at sound decisions. A bit of complexity is involved here; but having access to a managerial accounting guide helps clarify some of the grey areas.

How it All Began

Management’s use of accounting data sprung from the early 1900’s cost accounting initiatives, which were introduced by the principles of scientific management.

However, in light of the present-day developments in managerial approach, a distinction between managerial and cost accounting concepts should be established. The former pertains to financial data gathering and its analysis. It involves the generation of reports, which serve as tools used in various operational activities of business organizations. Cost accounting, on the other hand, represents the tools, approaches and methodologies being used to generate key financial data for production costs.

Later developments after World War II came to include not only the reports about variance analysis between budgeted manufacturing costs and actual expenditures but also information about backlogs on sales orders, and inventory management in relation to customers’ demands. The review of internal resources and their capacity to provide such demands also came to the fore.

Let us first delve into the evolution and development of managerial accounting functions, and how the concept came to cover broader areas of performance measurement. The following articles have been rounded-up to give readers a more in-depth view of the circumstances that gave birth to the concept of traditional managerial accounting:

- The Evolution of Performance Cost Measures: History and Recent Developments

- Scientific Management and Its Principles - Their Relevance in Today’s Business Trends

- Explore the History of Time Management

- Goldratt’s Theory of Constraints

Understanding the Significance of Cost Accounting Standards

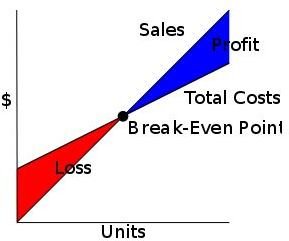

Cost accounting tools and approaches remain vital components to operations management and its accounting requirements. They include specific processes for determining and evaluating different production costs. First, there is the matter of pre-determining standard costs, to which actual costs incurred are being compared. More importantly, there is the need to determine the sales levels and the cost volume at which the “break-even point” can be achieved.

The following articles offer comprehensive explanations about these concepts:

- What is Cost Object: 3 Estimators for Translating Raw Data

- How Are Standard Costs Developed?

- Best Practices in Evaluating Standard Costs

- Standard Costing Techniques

- Break-Even Point Analysis Example in Managerial Accounting

- Perform a CVP Analysis to Determine Your Break Even Point

Cost Data as Bases for Product Pricing Strategies

Cost accounting broaches different approaches by which manufacturing expenditures are being established, distributed and calculated in order to determine product cost per unit. The objective is to determine the ideal costs on which to base the selling price, which a willing customer would pay for a particular product.

There is also the matter of pinpointing the actual cost drivers by departing from the traditional absorption costing method. Modern-day managerial accounting views are more inclined toward the adoption of activity based costing approach and the establishment of cost centers. Other aspects to consider include concerns over costs and pricing strategies for unique job orders as against products of a more homogenous type.

Learn more about the different perspectives presented by various cost data by exploring the explanations in the following articles:

- Types of Costs in Managerial Accounting

- Product Costs versus Period Costs

- Typical Examples of Period Costs

- Examples of Production Input Costs or Manufacturing Overhead Costs

- Job Costing vs. Process Costing

- Pros and Cons of Process Costing

- Examples of Absorption Costing Calculations

- Pros and Cons of Activity-Based Costing

- Examples of Variable Costs for the Layman

Analyzing Productivity Variances and Rates of Efficiency

Conventionally, all these financial data are presented as performance reports that contain the results of their corresponding variance analyses. The reports are aimed at providing a clear picture of how each department contributed in the operational activities of the manufacturing company.

Gathering financial information is not only for the purpose of evaluating the effectiveness of pricing and selling strategies but also for assessing the efficiency by which demands for the products are met. Here, managerial accounting also gives analysis reports pertaining to inventory levels since large amounts of inventory denote capital funds that are still tied-up in unsold goods.

Learning all these requires a deeper understanding of the theories governing the premises on which the analyses tools are based. Readers can derive this information from the following articles:

- Analyzing Variance: Tips, Examples & Calculations

- Example of How Manufacturing Cycle Efficiency is Calculated

- Improving Productivity Rate –Eliminating Lost and Idle Time in Production Cells

- How Does Downtime Influence Manufacturing Efficiency?

- Identify Waste and Process Inefficiencies the Easy Way

- Performing Bottleneck Analysis - A Matter of Applying the Right Theories and Techniques

- Determining Sales to Fixed Assets Ratios

Present-Day Operations Management and Its Solutions

In today’s present business management trends, the use of financial data and its analysis tools have been integrated into a framework known as the Balanced Scorecard. The objective is to align all initiatives toward the achievement of business goals by making the managerial accounting reports more comprehensible to everyone involved. That way, each organizational member has a clearer perception of his or her role and contributions.

Gaining internal support is of utmost importance for any changes implemented by management to improve productivity and efficiency. Analysis results are useful only if the recommended solutions will have the full-dedication and support of all the stakeholders.

There is also the need to raise awareness about gaining customers’ satisfaction as an important factor in improving the financial health and stability of the company. Readers should increase their own awareness by understanding the true significance of the balanced scorecard and several change management initiatives. Exploring the contents of the following articles will elevate one’s perception of their potentials in improving operational performance:

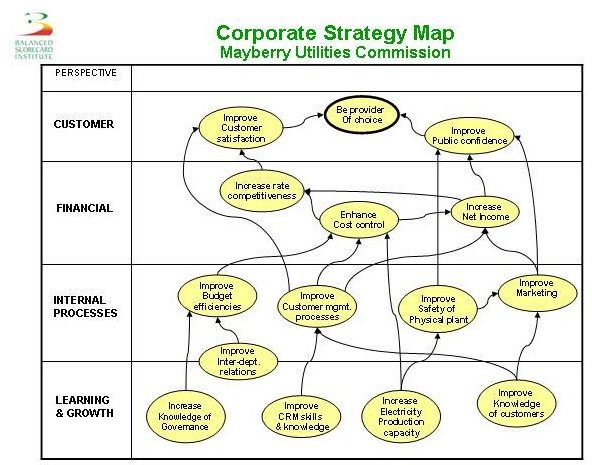

- Should Your Company Use Balanced Scorecards?

- Working Examples of a Balanced Scorecard

- Overcoming Resistance, Ignorance and Denial in Change Management

- Effects of Total Quality Management (TQM) on Profitability and Productivity

- What Does Kaizen Mean in Relation to Process Improvements

- Principles of Just-in-Time (JIT) in Improving Quality and in Eliminating Wastes

- Technological Advances that Support the Goals of JIT

- Advantages of the Kanban System – How Kanban Improves Production and Response to Demand

- Seven Tips to Manage Your Business During Economic Slowdown

Study how all the bits and pieces of information pulled together in this managerial accounting guide, project a clearer vision of how successful business organizations make use of accounting data in achieving their financial goals.

References

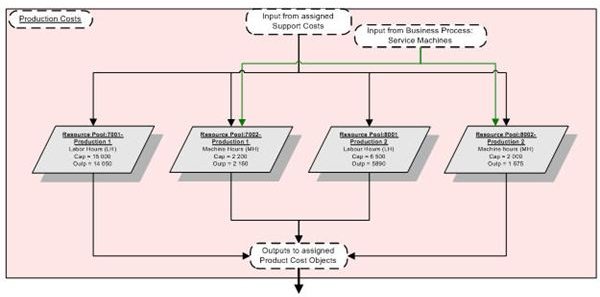

- Image: Figure 10 - Storyboard, Production Costs by B england CCA-SA 3.0 Unported.

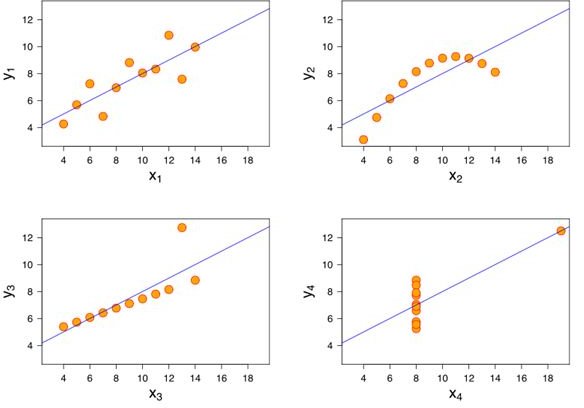

- Image: This graphic represents the four datasets defined by Francis Anscombe for which some of the usual statistical properties (mean, variance, correlation and regression line) are the same, even though the datasets are different.By Anscombe.svg: Schutz CCA-SA 3.0 Unported.

- Image: Cost-Volume-Profit diagram, showing Break-Even Point as point where Total Costs equals Sales.By Nils R. Barth under public domain.

- Image: Example of a balanced scorecard strategy map for a public-sector organization by Parveson under public domain.

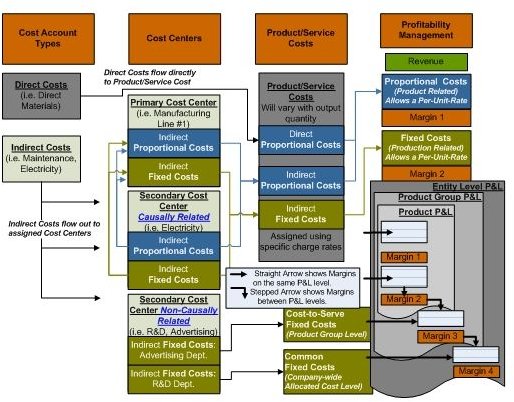

- Image: GPK Marginal Costing Structure Flow of Grenzplankostenrechnung; the German costing system flowchart for managerial accounting.By B england CCA-SA 3.0 Unported.