Keeping an accurate set of financial records means one needs to understand the importance of adjusting journal entries (AJEs)! AJEs are used on all sorts of accounts whether it is to correct a bookkeeping error or to adjust expenses or assets. Jean Scheid explores AJEs.

What Are Adjusting Journal Entries?

The Accounting Study Guide describes adjusting journal entries (AJEs) as “An adjusting journal entry is a journal entry prepared to adjust account balances.” They also note, “The only way of changing account balances is to make journal entries.”

That pretty much tells you right off what the purpose of an AJE is, but what is the importance of adjusting journal entries, when do you utilize them, and what happens if you fail to check the necessity of AJEs before you close an accounting period?

Image Credit (Freedigitalphotos )

Reasons for AJEs

There are many reasons a company may need to make AJEs. They include

- Errors in posting on regular journal entries

- Change in a sale or cost of sale

- Change in dollars received based on cash sales

- Depreciation adjustments to fixed assets

- Adjustments to inventory

- Adjustments to officer/owner or capital accounts

- Retained earnings for a given period—these are usually offered up by a tax professional

Failure to consider journal entries that correct errors or change an account’s balance can mean incorrect financial statements such as the income statement and the balance sheet—and your trial balance may not balance without these adjusting journal entries.

Examples of AJEs

As a car dealer, I often find we have many AJEs that are needed in month! Most of these do not come from bookkeeping errors (although some do) but from other circumstances. For example, say my new car sales finance department enters a deal into the accounting system that offers an inaccurate commission due to the salesperson. Or, what if my bookkeeper entered the daily cash sales of $1,000 when they should have been $10,000?

These examples reflect the importance of adjusting journal entries and why you need them to make your accounting books accurate.

Wrong Commission AJE

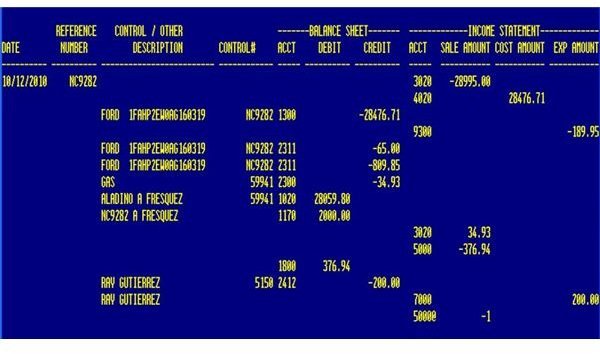

In this example, the new car sales transaction shows salesman Ray was to get a commission of $300, however, the finance manager entered the amount incorrectly as $200. When the sales transaction is looked at from the new sales journal side, it won’t balance for one, so there are a couple accounts that need to be adjusted. (Click on the Journal Example to the right to enlarge).

In the journal example we see that salesman Ray Guiterrez the following posted to these accounts:

- Credit to Account #2412 – Accrued Sales Commissions Payable (-$200)

- Debit to Account #7000 - New Sales Commissions Expense - $200.

We already know that Ray is due a commission of $300, not $200 so how does this journal get adjusted? The AJE would look like this:

Account Number – Account Name – Amount – Debit or Credit

- 2412 – Accrued Sales Commission Payable - $100 – Credit

- 7000 – New Car Sales Commissions Expense - $100 – Debit

This adjusting journal entry will now show the correct commission and also the correct cost. Keep in mind that even in adjusting journal entries, your debits and credits must equal.

Screenshot courtesy of author - personal business accounting journal.

Correcting Errors With AJEs

If your bookkeeper has made a journal entry reflecting the day’s cash deposits that were $10,000, but only entered $1,000, how would you adjust this journal entry?

The initial journal entry would look like this:

- Debit to Bank Account 1000 - $1,000

- Credit to Cash Sales 1117 – (-1,000)

The bookkeeper realizes the error and now it needs to be adjusted so the AJE would look this way:

Account Number – Account Name – Amount – Debit or Credit

- 1000 – Bank Account - $9,000 – Debit

- 1117 – Cash Sales - $9,000 – Credit

We would now have the correct adjusting journal entry to make the day’s cash deposits correct. But, what if that $10,000 was not all cash sales and some were charge accounts that had to be posted as an accounts receivable ?

Image Credit (Freedigitalphotos )

Fixing Multiple Accounts With AJEs

You can fix the $10,000 error that was posted as $1,000 for cash in bank, but what if of that $10,000, $3,000 was charge account customers, meaning a post to your accounts receivables.

Remember this is our initial incorrect journal entry and we are off by $9,000:

- Debit to Bank Account 1000 - $1,000

- Credit to Cash Sales 1117 – (-1,000)

Now, let’s take a look at how it’s easily adjusted to reflect the entire $10,000 with $3,000 going to accounts receivables.

Account Number – Account Name – Amount – Debit or Credit

- 1110 – A/R Sales - $3,000 - Credit

- 1117 – Cash Sales - $6,000 – Credit

- 1001 – Cash in Bank - $9,000 – Debit

Here again, our debits and credits equal, we now have the appropriate cash in the bank and have adjusted the accounts receivables and cash sales. AJEs are usually entered into a general journal or an adjusting journal.

The importance of adjusting journal entries is essential for accurate financial records and to ensure your reports such as your balance sheet, income statement, and trial balance are corrected. Often bookkeepers will print an initial trial balance to see if all the debits and credits equal and if not, research the error, make the necessary AJEs and then reprint an adjusted trial balance.

Failure to follow the general accounting principles meaning all debits and credit must equal and that account balances can ONLY be adjusted via adjusting journal entries is key in maintaining accurate accounting records.

Image Credit (Freedigitalphotos )

This post is part of the series: All About Journal Entries

Find tips and advice on how to record journal entries for all types of transactions along with free, downloadable forms you can use for a variety of accounting purposes.