What important lessons can be learned in revisiting the key milestones in the history of accounting? Here, readers will come to understand that even in the earliest levels of civilization; humans devised methods of keeping track of events and transactions for making important economic decisions.

Prehistoric Roots – Around 35,000 BC

Accounting by its most basic definition is a method of recording economic transactions, which allows users to arrive at judgments, projections and reasonable conclusions. The first accounting artifacts were uncovered in the city of Jericho in Israel from among the ruins that date as far back as 7,000 years ago.

However, as archaeologists unearthed numerous artifacts in different parts of the world, additional evidences about the origins of accounting show proof that the discipline takes its roots during the prehistoric era known as the Paleolithic period.

The discovery of prehistoric caves in Czechoslovakia (1937) and in some parts of Africa produced evidences of how cavemen devised their own system of recording economic transactions. The jawbone of a wolf found in the Czechoslovakian cave revealed fifty-five notches carved into groups of five. Although the significance of the number is unexplained, the pattern of the carvings denoted a form of tally system.

In 1960, archaeological finds in the buried remains of a small African community in Congo included a piece of animal bone bearing similar carved-markings grouped in 11, 13, 17 and 19. This was later called the “Ishango Bone”, which was named after the African farming settlement that was known to have existed in the area but was later buried under tons of volcanic debris

Thirteen years later, the 1973 excavation report of the artifacts found in the Border Cave of Lebombo Mountains in Swaziland revealed a more discernible style of tally system. The fibular bone of a baboon showed notch-carvings in groups of 29. The notches were believed to be a way of recording the number of days or nights that pass before the moon re-appears. Many interpreted this as a method of counting the number of months until harvest time.

The Middle-Ages and the Earliest Known Civilizations

Through the passage of time, the livelihood among primitive people was said to have transformed from that of hunters to that of farmers , which brought certain changes in mankind’s way of life. This included the exchange of goods for crops or vice versa since this afforded a better alternative to hunting. Thus, it came to a point that these farmers convened at some trading places where they could trade by way of barter.

Mesopotamia and the City of Sumeria

Advancements into the earliest known civilizations were spurred by the spreading out of agricultural practices, particularly in Mesopotamia. This ancient region used to lie between the Tigris and Euphrates River in the Middle East, and was once fertile and capable of producing numerous crops before it became a vast tract of arid desert land.

In most of the archaeological sites in this area, tokens in varying geometric forms were found and were surmised to have been used as a means for establishing the equivalent quantity of a bartered item. Accordingly, the tokens were widely used for about 5,000 years before a more sophisticated system of numbering was conceptualized in 3,500 B.C.

The Sumerian Scribes, Their Clay Tablets & the Cuneiform

The artifacts discovered in the ancient city of Sumeria, in the Mesopotamian region, revealed a more complex economic system that existed around 8,000 B.C. The city is deemed to have served as the trading hub for merchants and manufacturers of metal, lumber and stone wares.

The improvements in the use of tokens and markers were evidences that the Sumerian scribes invented a hieroglyphic or symbolic system of writing transactions called “cuneiform”. The clay tablets found were interpreted to be inventories for the temple warehouses. Some appeared to be a form of wage lists for agent artisans. Others seemed to belong to merchants and traders, who took stock of their wares by using clay tablets incised with wedge-like cuneiform symbols.

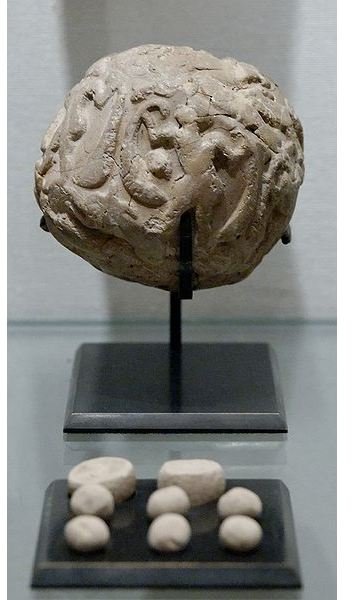

Around 3,500 B.C. the writing and recording systems developed by the Sumerian scribes had improved and included a globular clay envelope. The device was said to have permitted traders to enter into a form of forward contract agreement to deliver and to pay for goods at some future time. Tokens were baked into a globular clay vessel to indicate the quantity of goods to be delivered and the date on which said goods were to be delivered.

The Scribes and Papyrus of Egypt

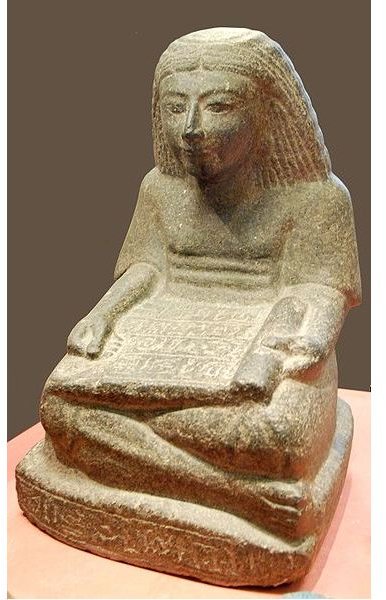

It was also during this period that the Egyptians invented a more sophisticated form of writing material, which we all know as “papyrus”. Egyptian scribes were chosen to act as administrators of palaces and temples and overseers of the Pharaoh’s many projects. They kept records of grains, stocks, copper implements, and various forms of materials withdrawn from royal warehouses by keeping ledgers in the form of scrolls.

Through the use of Egypt’s own hieroglyphic system and the papyrus material, scribes were likewise tasked to impose and collect taxes from among the members of Egypt’s society. They organized armies, conducted audits, and calculated the number of bricks and slaves needed to build temples and tombs. One such scribe named Imoteph became quite famous as the architect and administrator in-charge of building the Step Pyramid Complex at Saqqara, Egypt.

Hence, other civilizations, particularly the Greeks and Romans, likewise made use of this light material for their writing and documentation purposes and replaced the cumbersome clay tablets and geometric tokens popularized by Mesopotamia. In later years, other forms of writing materials such as parchment and linen paper originating from China reached Baghdad and subsequently replaced the once popular papyrus.

From Abax to Abacus

More artifacts from the city of Sumer showed that trading activities made use of the Abax, which was a table covered with dust and pebbles used for counting and calculating. The table later evolved into a flat surface enclosed in a wooden frame. Attached to the frame were several wires strung with ten beads each and were used for making calculations. “Abax” is a Greek word for dust

China came up with its own version of the Abax between the 12th and 13 century A.D. Traders referred to the Chinese device as abacus, and it was modified into having only seven beads in each row. Two of the beads in each row were placed separately in an upper deck, while the other five beads were in a lower deck.

Money and Its Origins

Further developments in ancient civilizations showed signs that barter trade came to be regarded as cumbersome. A trader who had a specific need had to seek for merchants who would be willing to accept the goods he or she had to offer as a medium of exchange. Consequentially, both merchants and traders realized that bartering for goods was a slow and at times an unfruitful process.

Hence, a special article of trade considered valuable to everyone was invented, and it initially came in the form of ingots, rings and bullion made from bronze, copper and silver. In other parts of the world, the Chinese traders during the same era were said to have used cowrie shells and later transformed this medium into bronze and copper cowrie-likenesses. However, these monies were considered as primitive coins or pre-coins including the gold and silver coins used by the Greeks of Ionia.

The Lydia Lion, a coin that was minted around 600 BC in a place called Lydia, in Asia Minor (now known as Turkey), is believed to be the first formal form of money. It was established that the Lydia Lion was issued in greater quantities than those that existed in the region during the said era. Other coins were surmised to have been issued by employers, noblemen and merchants for their private uses.

However, unlike the Lydia Lion coins, the privately issued coins lacked the essential features of a formal medium of exchange. They did not bear the marks or features of money that was recognized by the authorities of a state or governing body. Greek historians believed that the Lydian society was among the first to exhibit a successful transformation from agricultural barter economy to an urban monetary economy.

The Origins of Money Exchange

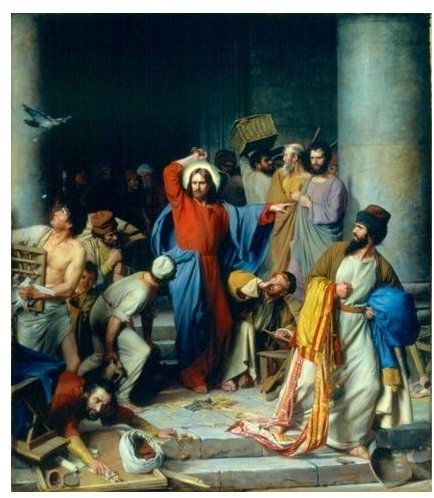

Due to the proliferation of different types of money in circulation, a new form of trade involving the exchange of money to what was acceptable came to the fore. Recall that in one of the biblical passages, Jesus was angered by the presence of money changers inside the temple. Accordingly, the only money that was recognized as valid payment for the required temple tax was a special coin called “shekelshekel”. The coin contained a half ounce of silver and had no image of a pagan emperor inscribed on it.

Thus, the money changers who appeared to have had control over the limited supply of these coins provided the market for the said coins right in the temple grounds. Moreover, they were able to manipulate the prices based on the level of demand.

Please turn to page two for more of the key milestones in the history of accounting.

The Development of the Banking System

Modern day banking, on the other hand, originated from the goldsmiths of Medieval England around 1000 -1100 A.D. Customers entrusted their gold and silver for safekeeping to their goldsmiths, who in turn, issued a receipt to acknowledge every valuable that was entrusted to them. As this became a popular practice, some customers merely traded the receipts instead of withdrawing their valuables from their goldsmith.

The system then presented an opportunity for these goldsmiths to loan out money just by issuing a receipt even if it was not backed by any gold or silver held for safekeeping. The borrower on the other hand would use the goldsmith’s receipt for his trading purposes. However, the borrower had to raise the gold to back up the goldsmith’s receipt; or the latter would seize some of the borrower’s possessions in order to raise money to buy the required gold amount.

This system was called “Fractional Reserve Banking,” which today is considered fraudulent as compared to the recognized system of “Full Reserve Banking.” The latter system requires banks and other financial institutions to put up a capital reserve in a centralized depository unit. Otherwise, the government’s regulatory body will order the delinquent bank to cease its operations and return the depositors’ money.

The Renaissance Era and the Double-Entry Bookkeeping System (1494)

The Renaissance Era came about during the Middle Ages when cultural decline and developments had been stifled by the occurrences of wars and invasions among European nations. On the other hand, growth and civilization in the Middle East were likewise marred by tribal wars and the shifting of religious beliefs and culture.

After quite some time, a group of intellectuals coming mostly from Italy sought to bring back the elements of humanism and reason in Europe. Thus, the Renaissance was considered by many as a form of rebirth and recovery from all the turmoil created by the previous wars.

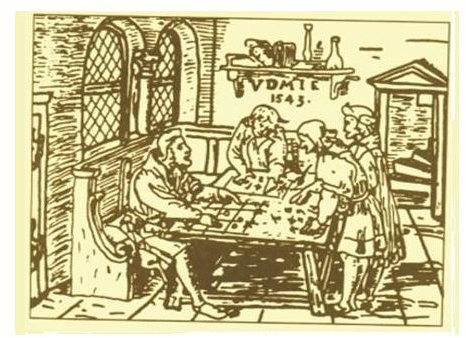

Included among these intellectuals was a Franciscan friar named Luca Bartolomes Pacioli to whom the development of the double-entry system of bookkeeping is attributed. He developed the system as a form of arithmetical procedure for merchants and traders to keep their records organized.

There are sixteen chapters from out of the 36 chapters of Fray Pacioli’s book entitled “Summa de Arithmetica, Geometrica, Proportioni et Proportionalita” that describe in details the layout of the books. Descriptions and explanations are about the merchant’s private daybook, the journal where transaction entries are to be recorded and the ledger book, which features two pages for each type of transaction. The said pages represent the debits and the credits of the double-entry method of bookkeeping. Fray Pacioli acknowledged in his book that the methods were compiled from the contributions of numerous mathematicians, which he adopted in order to come up with the accounting system still being recognized up to this date.

The Age of Industrialization and Cost Accounting

The accounting system developed by Fray Pacioli worked out well as trade and commerce expanded not only among European nations but throughout Asia and the New World or what was to become the United States of America. However, the businesses that came about during the Age of Industrial Revolution needed more than just the bookkeeping method used for simple buying and selling activities.

Machineries had been invented, which permitted the invention or creation of more innovations. However, the need to account as to how much had been invested in these machineries and the raw materials requirement, became necessary. Much of the capital was being tied up in assets and raw materials, which were all new to the business owners and those participating in capital markets as investors. They soon realized that they needed the expertise of public accountants to analyze the financial effects.

However, some of these experts became willing participants in applying their techniques to create leverages for buying out competitors, instituting monopolies, and manipulating the stock market prices. The imbalance created by the unequal distribution of wealth in all levels of society brought about the Great Stock Market Crash of 1929 and subsequently the Great Depression.

Thus, the key milestones in the history of accounting during this era were represented not only by the development of a cost accounting system but also by the implementation of a uniform standard of accounting principles and practices. Through the establishment of the Securities and Exchange Commission, all public corporations were required to submit financial statements that have been duly certified by an independent public accountant. Said certifications served as proofs that the financial data presented have been verified as true representations of the company and were calculated in accordance with the uniform and generally accepted accounting principles (GAAP).

The Advent of Computerization

The advancements in computer technology made possible the development of a computerized system of performing accounting tasks. This paved the way for businesses to increase work productivity and accessibility of financial data in summarized forms. Information became readily available in real-time, which permitted business owners and managers to make quick decisions based on fresh and current data.

However, to the detriment of those who were still submitting financial reports that were not in accordance with the generally accepted accounting principles, the computerized systems likewise allowed analysts to easily compare financial data against other references that could be accessed via databases and industry standards.

Thus, the advent of computer technology empowered regulatory bodies and independent analysts to uncover another round of accounting malpractices in 2001 to 2002 . Similar to the 1929 event, the unraveling of the fraudulent manipulation of accounting records and stock market prices by numerous high-profiled businesses like Enron, likewise led to the 2002 stock market crash called “The Internet Bubble”.

Accounting has been recognized as a system of recording transactions to provide usable economic information. We have revisited the key milestones in the history of accounting by following through the developments in civilization. Mankind’s need became numerous and more complex; hence, the developments in the writing systems and methodologies made the recording of events and transactions more concrete. The objective then and now is still the same: to provide reliable information on which to base sound economic decisions.

References

- Image: Homebank04 by : Benjaminevans82 at wikimedia under public domain.

- Image: Photo of the Ishango

bone from two different points of view. Science

Museum of Brussels gave the photo.Wikimedia under CC BY 2.5 - Image: Costing Continuum Maturity Mode

l by Gary Cokins Wikimedia / Used with

permission by the International Federation of Accountants , Professional

Accountants in Business Committee - International Good Practice Guidance, - By Elliott, Robert K. Remarks at Rutgers Professional Accounting Annual Alumni Reception Newark, NJ June 17, 2010 http://webcache.googleusercontent.com/search? q=cache:7JwLZqbieTcJ:raw.rutgers.edu/docs/Elliott/Elliott%2520PAMBA%2520remarks.pdf+accounting+in+the+age+of+industrialization&hl=en&gl=ph

- Image: Accountancy clay envelope Louvre

Sb1932 by Marie-Lan Nguyen (2009)/

Wikimedia under CC BY 2.5. - Image: Seated scribe with papyrus scroll

Louvre by Janmad at Wikimedia under

CC BY 3.0. - Xat.Org: The History of Money Part I http://www.xat.org/xat/moneyhistory.html

- Image: Pacioli Attributed to Jacopo de’ Barbari

/ Wikimdia under public

domain. - Image: Sialk ziggurat rendition

by unkown artist in the early 1900s. Scanned

by user Zereshk at english wikipedia from original document from Wiedener

Library, Harvard.Wikimedia under public domain. - Image: Kroisos BMC 31 by CNG Classical Numismatic Group, at Wikimedia CC BY-SA 2.5

- Image: Jesus casting out the money changers at the temple

by

Carl Bloch (1834–1890)/ Wikimedia under public domain. - World of Mathematics on Luca Bartolomes Pacioli http://www.bookrags.com/biography/luca-bartolomes-pacioli-wom/

- Image: The ground of artes 1543 by :Robert Recorde

/ Wikimedia under public

domain. - Image: Petrus Christus 003

by: The Yorck Project: 10.000 Meisterwerke der

Malerei. DVD-ROM, 2002. ISBN 3936122202. Distributed by DIRECTMEDIA

Publishing GmbH/ Wikimedia under public domain.