When looking at a financial statement, do the numbers just seem to be a jumbled mess? There actually are specific methods you can use to analyze the information, and this guide will walk you through the steps of the process with realistic samples.

Interpreting the Numbers

In learning how to perform a financial statement analysis, you need to acquaint yourself with the accounting tools commonly used for comparing and interpreting the elements of a financial report. Inasmuch as your goal is to establish growth, trends, performance, profitability and the liquidity of the company, you will have to examine not only the current but also the previous reports.

These reports are best presented in formats known as common size financial statements (FS), in which the relationships and changes between current financial components and their historical costs are vertically or horizontally assessed.

Two separate articles entitled

- Comparative and Common Size Financial Statement: Explaining the Difference

- Analysis of Common Size Financial Statement

provide a set of comprehensive guidelines on how to use common size formats for evaluating past and present financial data, in order to determine performance trends or business growth as well as structural compositions of a company.

Another separate article, captioned as Common Formulas for Accounting Ratios , furnishes the formulas used as tools to analyze behaviors in terms of performance results, turnovers and efficiency.

Determining the Objectives of your Analysis

In performing your financial analysis, you have to have a clear objective about the information you want to extract. Keep in mind that you don’t have to sink your teeth into numerous variables and percentages, unless you’re into performing a deep accounting analysis of the financial statement components.

Financial statement analysis is different in the sense that you take into consideration the critical areas that create material impact in the results of the business operations. The relationships between components, their increments and denouements, can reveal the efficiency of the strategies implemented, as well as the health and growth of a company’s financial conditions.

Kindly click on the screen-shot images of the financial statement examples, in order to get an enlarged view.

Horizontal Financial Statement Analysis

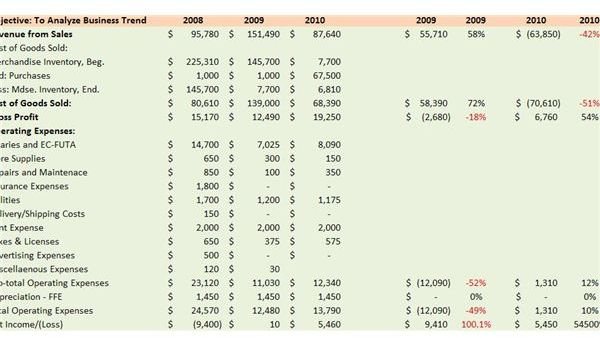

Objective: To Analyze Business Trend

The analysis used for this purpose was the horizontal method of comparing year-to-year trend results.

Study the screen-shot image of our sample template, which aims to determine how the subject company fared during the height of the recession; this was from 2008-2009. Since the company survived the financial difficulties of those periods, our interest would be on the trend results and the strategies that were used.

Understand the correlation between Sales, the Cost of Goods Sold, the Merchandise Inventory and the Gross Profit; examine the increase or decrease of these components.

-

Take note if the increase in Revenue from Sales (cash-in) in 2009 is met with a similar increase in Gross Profit. In our example, there was a 58% increase in sales but the corresponding gross profit decreased by 18%. This denotes that the company did not add enough price value mark-ups to the products they sold in 2009.

-

Study the increase or decrease in the Cost of Goods Sold and the Merchandise Inventory End. An increase in sales denotes a corresponding increase in costs, but we should also establish whether such costs entailed the procurement of new purchases or if the goods sold came from old stocks.

Advertisement -

Our sample financial statement shows that the 2009 Cost of Goods Sold increased by 72%, which confirms our previous analysis about the selling price of the products sold during the year. In this case however, it appears that the cost of the product was even higher than the selling price. Was this a wise move? What could be the rationale behind this strategy?

-

Examine further that the Merchandise Inventory at the beginning of 2009 was $145,700 and dropped to $7,700 at year end. Purchases were minimal and amounted to only $1,000. This indicates that the majority of the products sold during the year were from old stocks and that the company deemed it best not to make additional purchases. Since the cost of goods was higher, we can surmise that their old stock was sold at discounted prices.

Advertisement -

The business strategy adopted was to sell the products at lowered prices in order to recover, even in part, the procurement costs. This then allowed the entity to convert its inventory stocks into cash, to improve its liquidity during the period of recession.

-

In addition, it appears that its operating expenses were greatly reduced, including manpower costs, which could denote salary cut-backs and layoffs. Nonetheless, the company was able to meet a break-even result during the 2009 operations, instead of continuing the net loss trend of 2008.

Advertisement -

By the year 2010, most of goods from the old inventory were sold off, because of which the company found it necessary to make additional purchases. The investment was profitable because the enitity was able to gain a minimal net income of $5,450. Based on this analysis, the business strategy made it possible for the entity to maintain continuous customer patronage, by selling products that were in demand and at affordable prices.

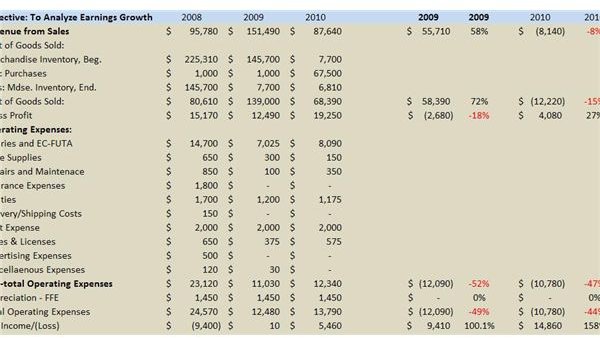

Objective: To Analyze Earnings Growth

In learning how to perform a financial statement analysis, learn of another concept for which horizontal analysis is used — for analyzing earnings growth. This is to gauge an organization’s ability to improve the results of its operations, from a specific base year period.

In this example, the base year to which growth was compared is 2008, while the business earnings growth are measured from the point of base year to current year. This is different from the trending analysis method of comparing on a year-to-year basis.

The results of our earnings growth analysis confirm our earlier evaluation of the business trend that transpired. The increase in earnings coming from a net loss of $9,400 in 2008 resulted in a break-even performance in 2009 and in profit in 2010. Albeit minimal, such progress is still notable in a period of recession.

We can therefore surmise that the company is quite effective in devising strategies for coping with business setbacks .

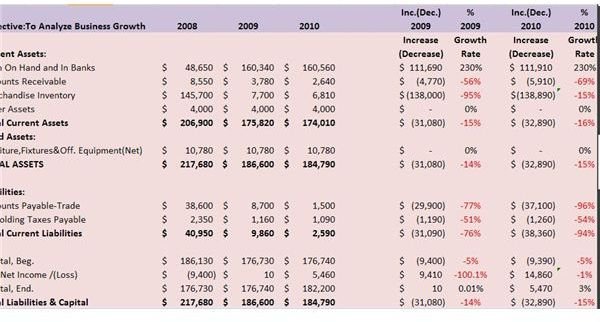

Objective: To Analyze Business Growth

Understand the use of horizontal analysis for balance sheet reports. Since growth pertains to comparisons using a base year, our analysis will again make use of 2008 in evaluating growth.

In this aspect, we explored the effects of the income statement results in the company’s assets, and the following information and their inferences were gathered:

-

Overall growth of assets in 2009 and 2010 disclosed negative results, at -14% and -15% , respectively.

-

This can be explained due to sales increments that did not actually generate profits but only yielded break-even returns and a minimal residual income. Hence, cash that was generated was basically used to meet the day-to-day expenses of the company.

-

Despite the negative impact, the company’s accounts payable was greatly reduced by the funds generated from the year’s sales results.

-

The decrease in accounts receivable denotes collection and was used as additional funds to meet the company’s cashflow requirements during the years 2009 to 2010.

Although the company can be considered liquid, it’s still necessary for the organization to invest its resources in more profit-generating ventures. Otherwise, said resources will eventually be depleted, because the company has to pay fixed overhead costs as an on-going business venture.

The information furnished on the next page is about learning how to perform a financial statement analysis using the vertical method of evaluating financial reports.

How to Perform a Vertical Financial Statement Analysis

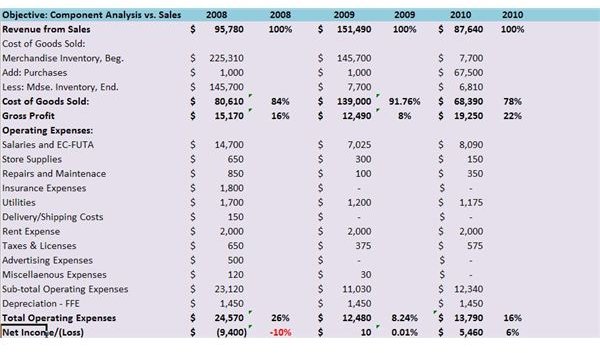

Objective: Component Analysis of Sales

After establsihing the subject company’s performance trends and growth from 2008 to 2010, our next objective is to determine the impact of the income and expense components. Our focus will be the critical points that made it possible for the entity to survive a general condition of economic downturn.

In order to extract the information we needed, we performed a vertical financial statement analysis of the income statement, from which we gathered the following:

-

The 2008 net loss of $( 9,400), was brought about by the incurrence of operating expenses at a total amount that was greater than the gross profit margin. The 2008 Revenue from Sales generated a gross profit of only 16%, yet the proportion of the total operating expenses as a component of sales, was 26%. Naturally, this resulted to a 10% net loss.

-

In 2009, the company deemed it best to generate sales from its slow moving stocks by selling them at discounted prices, instead of purchasing new stocks. This can be gleaned by looking at the proportion of the Cost of Goods Sold during that year, which was calculated at 91.76% of the Revenue from Sales. Thus, the gross profit margin was even lower at 8% or thereabout. However, the company reduced its operating costs from the previous year’s proportion of 26%, by keeping it within the 8% gross profit margin at the least. This strategy made it possible for the company to achieve breakeven results despite the lowered selling prices of the goods sold during the year.

-

In 2010, most of the remaining stocks were sold but additional purchases were made, and the selling price appeared higher than that of 2009. Take note of the proportion of the Cost of Goods Sold for the year, which was at 78% of the Revenue from Sales. This generated a gross profit yield of 22% from out of the revenues. As a result, the company was able to increase its manpower costs, which likewise increased the proportion of the total operating expenses to 16% and the remaining 6% was retained as residual net income.

-

In learning how to perform a financial statement analysis, you will have a better understanding of the components that comprise the Revenue from Sales, being the main goal to achieve in a business operation. By way of a vertical financial statement analysis, we were able to evaluate the critical points, which affected our subject company’s sales performance.

-

Moreover, it also enabled us to arrive at an understanding that the entity may not have performed well in terms of income generation, which was common to most businesses during the periods; but its management was quite efficient in containing and curtailing further losses.

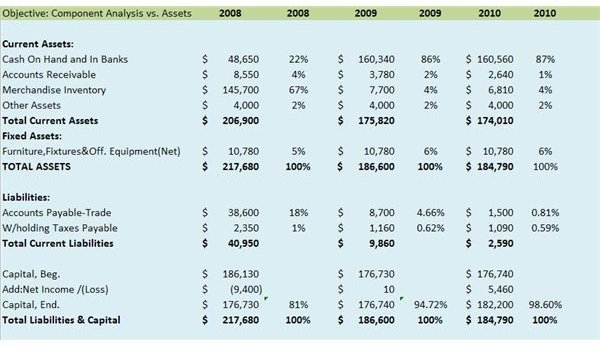

Objective: Component Analysis of the Assets

The vertical method of financial analysis can likewise be used in determining how the sales performance affected the company’s assets or resources.

As of 2008, management must have been aware that its current financial condition was precarious, since cash, which was 22% of the assets was almost equivalent to the total current debts of 20% (19% +1%).

This dilemma was resolved in 2009, as money was generated from selling old stocks and was preserved by not purchasing new goods for resale . Hence, the company was able to payoff its maturing debts.

Selling on credit was minimal since it represented only 4% of the total assets. The financial condition was further improved, as the receivables account was trimmed down to only 1% in 2010.

The last section is about using financial ratios as part of the learning process on how to perform a financial statement analysis, which readers can find in the next page.

Performing a Financial Statement Analysis Using Ratios

This section demonstrates the use of the common financial ratios in analyzing the 2010 FS, which is the latest financial report for our subject company, according to:

Liquidity:

Current Ratio = Current Assets: $ 174,010 / Current Liabilities: $ 2,590 = $67:$1

Quick Asset Ratio = Quick Assets (Cash and Accounts Receivable): $163,200 / Current Liabilities: $2,590

= $63:$1

Obviously, our subject company is quite liquid, since both ratios reveal that the entity has more than enough funds to meet every dollar of their current liabilities.

- Profitability:

Gross Profit Margin Ratio = 2010 Gross Profit: $19,250 / Net Income: $5,460 = $3.52:$1

2009 Gross Profit = $12,490 / Net Income: $12,480 = $1:$1

2008 Gross Profit = $15,170 / Net Income: ($9,400) = $1.61: ($1)

The gross profit trend reveals that the profit ratio in 2008 indicated that the company only had $1.61 margin by which it could incur operating expenses for every dollar earned as income. This critical information was overlooked, because operations resulted in a net loss during the year. Nonetheless, 2009 and 2010 showed considerable improvements as the ratios increased by reducing the operating expenses.

- Return on Equity:

2010 Net Income: $5,460 / Capital: $182,200 = $0.03:$1

There is still much to be desired as far as return on equity is concerned, inasmuch as the return on the owner’s capital investment as of 2010 is only 3 cents to every dollar invested. Based on this, if would be best if the entity reinvested its resources by purchasing more viable goods that are affordable and widely patronized by their customers.

Activity Ratios:

-

2010 Average Inventory= (Inventory Beg. $7,700 + Inventory End $6,810) / 2 years = $7,255

-

2010 Inventory Turnover= Cost of Goods Sold $68,390 / Average Inventory $7,255 = $9.40:$1

This denotes that for every $10 ($9 + $ 1) in inventory, an average of $9 in goods are sold and only a dollar’s worth is held as inventory. By this, it means most of the procurements during the year are sold, and that profits are realized.

-

Average Accounts Receivable = (Accounts Receivable, Beg. $3,780 = Accounts Receivable End. $2,640) / 2 yrs. = $3,210)

-

Accounts Receivable Turnover = Revenue from Sales: $87,640 / $3,210 = $27.30:$1

This denotes that for every dollar sales on account, the company was able to realize $27.30 by way of selling activities.

Solvency Ratios:

- Debt to Asset - Total Liabilities: $2,590 / Total Assets $184,790 = $0.014:$1

This means that for every dollar of the company’s assets, there is only one cent of liability to contend with.

- Debt to Equity - Total Liabilities $2,590 / Total Capital $182,200 = $0.014:$1

Similar to that of the debt-to-asset ratio, the entity has only one cent of debt to worry over for every dollar of its capital investment.

There are other ratios to use and explore, but their uses are mostly for in-depth accounting analysis, as a means to determine the elements that impact the financial conditions of the organization. The ratios that were used above to illustrate how to perform a financial statement analysis, are the most common and are regarded as critical points of considerations for purposes of business analysis.

Downloadable Financial Analysis Statement Worksheet

It may interest the readers to know that the different financial statements used as illustrative samples for this article’s discussion on how to perform an analysis of financial statements can be used as templates and can be downloaded at Bright Hub’s Media Gallery.

Users can replace the cell values with their own financial data and the variables will be automatically computed in the corresponding analysis cells, thus facilitating the task of performing a financial analysis.

Image Credit:

- Screen-shot images of the financial statements were created for this article by author cscantoria.

- Image credit: Wikimedia Commons, www.moneyeconomics.com

This post is part of the series: Balanced Scorecards

Thinking about developing a balanced scorecard for your business? Learn more about these important analysis tools and find examples that you can freely download for your own personal or business use.