Most businesses have anticipated (or expected) income, but what is the process for making a journal entry for anticipated income? Even expected income can be considered an asset; and here, Jean Scheid tells you how to make these journal entries.

What Is Anticipated Income?

Based on the type of business you own, there are different types of anticipated income. Anticipated income can be as simple as your accounts receivables or more complex such as franchisor payments and even pre-paid expenses you will gain in the future. Other types of anticipated income are seen in expected rents or predicted income and, as such, journal entries for these types of anticipated income must also be considered.

Expected income must be kept track of in your accounting books because not only does it affect your financial statements, but if you don’t keep a record of it, you may forget it’s due to the company. Or, you may be showing income you will never receive, making your financials incorrect.

Below we’ll look at different methods of making a journal entry for anticipated income. Please click on screenshots to enlarge examples.

Image Credit (FreeDigitalPhotos, jscreationzs )

Simple Entries for Anticipated Income

The most common types of anticipated income such as accounts receivables, pre-paid expenses, and–if a franchise–franchisor incentives are simpler to make than predicted income that may or may not occur.

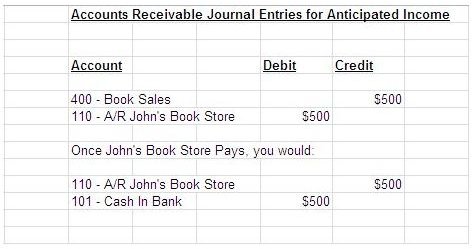

In the screenshot to the right, first is an accounts receivable (A/R) journal entry for anticipated income. Here, if your business sells to a credit customer, that income is anticipated—usually receivables are expected in net 10 or net 30 days. Once you sell to the customer, you credit your sales account and debit the A/R account. When the customer pays, a simple debit to cash and a credit to your A/R account wipes out the A/R; however, the sales credit remains on the income statement.

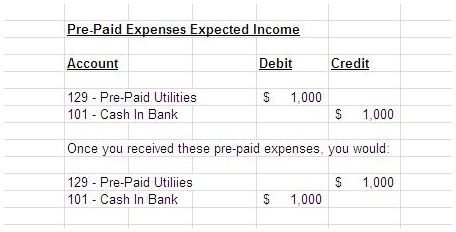

In the screenshot to the left, we see an example of a journal entry for anticipated income for pre-paid expenses. On a balance sheet , most pre-paid expenses such as utilities are shown as an asset as they are expected to be regained.

Here, the journal entry is a debit to the pre-paid expense and a credit to cash in bank. Once the pre-paid expense is regained, a debit to cash in bank and a credit to your pre-paid expense account clears the transaction for a clean balance sheet.

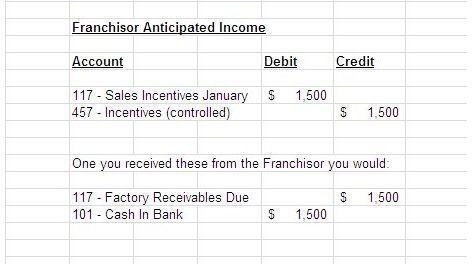

Finally, most franchise businesses expect incentives from the franchisor based on sales efforts or quotas. Here in our screenshot to the right, the franchisor incentives expected are posted in an income statement account as a credit, and a

debit goes to the franchisor receivable account. Once the money from the franchisor is received, a credit to the franchisor receivable account and a debit to cash in bank clears out the receivables due; however, the incentives earned remain on the income statement .

Screenshots created by and courtesy of author.

Other Types of Anticipated Income

Some income such as rents or predicted incomes are often posted to a receivable account and shown as income earned on the income statement. For example, an apartment complex may have anticipated rents of $5,000 for year-end based on rents due and may indeed record that as income. All or part of that $5,000 received before year-end is cleared by making a journal entry for rents due and those rents not paid would be carried over to the next accounting period—still showing as an asset.

Finally, some businesses predict income for the purposes of a better financial position to appear on their balance sheet and income statement. While this is common practice, if the predicted income can’t be achieved, it’s important to make adjusting journal entries to reflect an accurate trial balance, balance sheet, and income statement—those who fail to do this, don’t actually show true and correct income—a common misconception with journal entries and must be adjusted as required .

Follow the Rules

In the Generally Accepted Accounting Principles (GAAP), all types of anticipated income should be posted in “controlled” accounts. Controlled accounts are those where individual expected incomes, incentives, rents, etc. are controlled by a unique number for each customer or type of receivable. Controlled accounts will fall on various accounting schedules and an easy printout or analysis of schedules can show if anticipated income expected was indeed received, is still owed, or will never be realized. Making the appropriate journal entries for anticipated income and then making adjusting journal entries if income is not received is key in keeping your financial accounting records true and accurate.

Image Credit (FreeDigitalPhotos, renjith krishnan )

This post is part of the series: All About Journal Entries

Find tips and advice on how to record journal entries for all types of transactions along with free, downloadable forms you can use for a variety of accounting purposes.