A SEP-IRA is a tax-advantaged small business retirement plan. Like many other qualified plans, the limits on contributions are changed from time to time. Have there been any changes in the 2011 contribution limits?

Contributing to a SEP-IRA

A SEP is a simplified employee pension . It gives employers a way to contribute to an employee’s retirement without the complexity and overhead of a 401(k) plan or traditional pension plan.

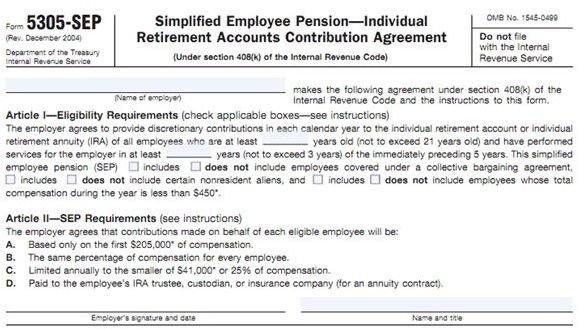

A SEP plan is setup by the business. Typically, the business uses the model IRS SEP created by Form 5305-SEP Simplified Employee Pension - Individual Retirement Accounts Contribution Agreement. In turn, each employee opens his own IRA account to be used with the SEP. This account is the SEP-IRA. A SEP-IRA is a special type of IRA account that allows for contributions to be made by someone other than the account owner. In this case, the employer contributes funds to the employee’s SEP-IRA according to the SEP plan document. Unlike traditional IRAs, Roth IRAs, and SIMPLE IRAs, employees do not contribute to the SEP-IRA.

Self-employed? If you set up a SEP-IRA for your business and need to know how much can I contribute to my SEP-IRA account, the rules are still the same. The contributions technically still come from the business and not you.

In all other ways, a SEP-IRA is the same as a traditional IRA. All funds within the account grow tax-deferred. When money is withdrawn, it is taxed as ordinary income, and if withdrawals are made before age 59 1/2, the owner may be subject to a 10 percent tax penalty. When the account owner reaches age 70 1/2, she must begin taking required minimum distributions, or RMDs from the account.

SEP-IRA Contribution Limits 2011

Contribution limits for a SEP-IRA may be changed each year based on annual cost-of-living adjustments. However, the index used by the IRS to determine the change in the cost-of-living did not increase enough to warrant any changes to the contribution limits for SEP-IRAs for 2011. Therefore, the limits on SEP-IRA contributions are the same for 2011 as they were for 2010.

The maximum contribuiton to a SEP-IRA is 25 percent of compensation. However, in 2011, as in 2010, only the first $245,000 of compensation may be considered when calculating contribution amounts. For example, if a person earns $300,000 per year at a business that contributes 6 percent to its employee’s SEP-IRA accounts, the maximum contribution to his SEP-IRA is $14,700, which is 6 percent of $245,000. The remaining earnings of $55,000 may not be used in the SEP-IRA contribution calculations.

There is also a $49,000 maximum contribution limit for both 2010 and 2011 for SEP-IRAs regardless of what percentage the company contributes or how much the employee makes.

There is no provision for catch-up contributions to SEP-IRAs like there are for other IRA retirement plans.

Finally, if the employer has another defined contribution retirement plan, such as a 401k, an annual limitation of $49,000 (for 2010 and 2011) for contributions to all qualified retirement plans applies. In other words, if the employer offers both a SEP-IRA and a 401k plan, the total combined contributions may not exceed $49,000 for the year.

Reference: IRS - Retirement Plans FAQs regarding SEPs

Image: IRS: Form 5305