Knowing the consequences of excess contribution to Roth IRA should stir awareness among account holders that over-contributions could be costly if left unchecked. This article goes beyond providing information about its tax implications, by furnishing pointers on how to avoid the unnecessary taxes .

The Consequences of Excess Roth IRA Contributions

Excess contribution to Roth IRA does happen and quite frequently so. If left unchecked and where tax returns have already been filed for the year, the account holder will have to pay 6% excise tax on the excess amount. This will be multiplied by the number of years that the excess amount was retained in the Roth IRA account.

In the event that the account holder has no other recourse but to withdraw the excess amount, the withdrawal shall be treated as an early distribution. A 10% withholding tax in addition to the 6% excise tax, has to be paid as additional tax obligation.

Remedies to Correct the Excess Contributions to the Roth IRA Account

The easiest remedy to correct an excess contribution is to withdraw the amount prior to one’s filing of tax return during the year that the over-contribution occurred. Inasmuch as no statement or report has been submitted yet, the excess contribution can simply be withdrawn as if it did not take place.

Otherwise, any of the following remedies may be taken accordingly:

1. If the taxpayer-account holder has already filed his tax return for the year, he still has 6 months, counting from the due date of the tax return, to remove the excess contribution from his Roth IRA investment. However, this action requires the filing of an amended tax return for excess contribution to Roth IRA and properly labeled with the notation “Filed pursuant to Section 301.9100-2” written at the top.

The amended return shall contain the necessary changes related to the excess contribution withdrawn from his Roth IRA account and shall be accompanied by a separate explanation for the withdrawal. This in effect, will reduce the total contribution as if no excess amount took place during the tax year.

2. In the event that the excess contribution was discovered after the deadline, and after the 6 months grace period for filing of tax returns and its amendment, the excess amount can be withdrawn and applied as contribution for the succeeding year. The taxpayer however, should make sure that this remedial action will not result to another excess annual contribution.

The 6% excise tax is now enforceable and the amount due shall be computed as follows:

Example: Excess contribution of $500 made in 2008 – rectification was made in January 2011; deadline for filing of tax return is April 18.

Amount of Excise Tax to be Paid on or before April 18, 2011 = ($500 x 6%) x 3 years = $90.00

3. If the account owner’s combined contributions for his entire IRA investments do not exceed the maximum allowable contributions, he can perform the so-called re-characterization procedure. This denotes the conversion of one type of IRA investment into another. As a remedial course of action, therefore, the excess amount will be added as contribution, usually to the traditional IRA account. Still, the 6% excise tax shall be due and payable during the tax year that the corrective action was made.

4. If the withdrawal of the excess amount will result to another round of over-contribution once applied and added to the subsequent year, the taxpayer’s remaining course of action is to withdraw the excess amount. However, this will be treated as an early distribution and a 10% withholding tax shall be paid. This is in addition to the 6% excise tax due as penalty for contributing beyond the allowable limit; all of which shall be paid during the tax year that the corrective action was taken.

As a note, the withdrawal in this case, is not included among those provided as exceptions to the 10% withholding tax.

Using the same example as above, the $500 excess amount will be subject to a 10% withholding tax, which is equivalent to $50. The total amount of tax due on or before April 18, as a result of this remedial action is $140, comprising $90 for excise tax and $50 for withholding tax.

After knowing the consequences and the remedies for excess contributions to Roth IRA account, your next area of concern should be the preventive measures to avoid its recurrence.

Find out how by proceeding to the next page.

How to Avoid the 6% Excise Tax on Excess Contributions to Roth IRA Accounts

To maximize the benefits of the Roth IRA, the learning process should go beyond knowing the consequences and remedies of the excess contributions. A Roth IRA owner’s next aim is to learn how to prevent its recurrence; in which case, he should:

- Gain knowledge on how to calculate the annual maximum allowable contributions and ascertain the correctness of one’s total contributions before the year ends. Consider that the easiest remedy to correct excess contributions is to withdraw the amount prior to the filing of one’s income tax return.

In line with this, kindly view a separate article entitled “What are the 2011 Roth IRA Contributions Limit” , which enlightens the readers with a set of step-by-step simplified guidelines on how to calculate the maximum allowable contribution for the year. A related Roth IRA Contributions Worksheet can be downloaded at Bright Hub’s Media Gallery.

Some others try to play it safe by arbitrarily reducing their previous year’s contributions. However, this might not prove to be a foolproof method, since the reduction will be based on taxpayer’s latest modified AGI. The surest way is to calculate the maximum amount by determining how much of the taxpayer’s IRA Roth eligibility has been phased out or eliminated.

-

If a Roth IRA contributor still couldn’t figure out the calculations on his own, it would be best to ask someone who knows how to check the amount of the contribution reduction for the year. That way, and before filing his income tax return for the year, the taxpayer can ascertain if his total IRA contributions for the year are within the allowable limits, .

Advertisement -

Take note that common mistakes committed in calculating the phased out limit or reduced contribution limits, are mostly on the following premises.

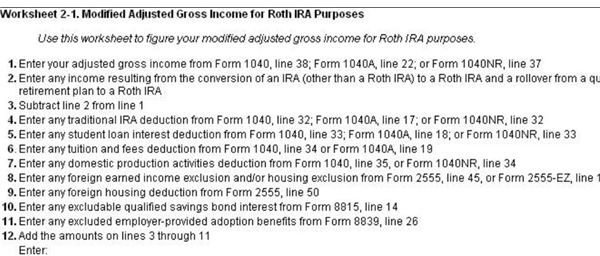

1. The correctness of the items subtracted and added to the AGI in order to arrive at the modified adjusted gross income. To make sure that proper modifications are made, IRS Publication 590 furnishes a list of these items in their Worksheet 2.1 Modified Adjusted Gross Income (MAGI) for Roth IRA purposes.

(Kindly click on the screen shot image for a larger view of the worksheet).

2. Deducting the other IRA contributions from the maximum allowed limit of $5,000 or $6,000 (for those aged 50 and above). Keep it in mind that these maximum contributions are to be spreadout for all types of IRA investments, to which the traditional IRA has the first priority.

If in case the account holder and his spouse has a total of $3,000 traditional IRA contributions made during the year and his Roth IRA contribution reduction for the year is $1,500, the account holder’s Roth IRA contribution limit for the year is computed as follows:

- Maximum Contributions Allowed - $5,000

- Less: Total IRA Contributions - $3,000

- Less: New Contribution Reduction - $1,500

- Allowable Roth IRA Contributions (New) - $500

If the owner’s total contribution to his Roth IRA account for the year exceeded $500 because he did not take his other IRA contributions into account, he can still withdraw the amount prior to his filing of tax returns and thus avoid the hassles and the 6% excise tax.

3. A similar mistake often committed is the non-inclusion of spousal IRAs for couples who are into filing joint tax returns.

Summary:

The complexity in handling Roth IRA accounts, stems from the constant changes in the annual contribution limits, as it gives first priority to the traditional IRAs . Not knowing the new contribution reduction often results to excess contributions to Roth IRA and the incurrence of the 6% excise tax.

Roth IRA owners, therefore, should make it a point to check their total IRA contributions for the year, prior to one’s filing of the annual income tax return. That way, excess or over-contributions, if any, can be simply withdrawn from the account.

Resources

Sources:

- Roth IRA lifted from https://www.irs.gov/publications/p590/ch02.html#en _US_2010_publink1000230977

Image Credit:

- Protecting Earned Benefits via wikimediacommonsVcarman

- IRS Worksheet 2.1 Screen shot image was created for this article by the author.