Queries about moving IRA accounts offshore are being raised by future retirees who plan to retire overseas or by those being enticed to invest their retirement funds on offshore properties. Offshore investing is touted as a viable vehicle for tax avoidance –how true could this be? Read on.

The Legality of Moving Your IRA Account to Offshore Investments

Moving IRA accounts offshore or to a foreign county is considered legal for as long as federal and taxation rules are observed. Foreign tax treaties are entered into by the U.S. government regarding the taxation of foreign nationals working in the United States. Most agreements basically entail the understanding that the similar tax treatments are afforded to U.S. nationals who are working or residing in foreign countries.

Accordingly, most treaties have a “Saving Clause”, which allows the US to tax its nationals as if there is no treaty being recognized to prevent its citizens from abusing the provisions of the tax agreements.

Foreign Tax Treaties: General Rule in the Taxation of Foreign Pensions and Annuity Distributions

As a general rule, tax treaties for foreign pension or annuity allow the country of residence to tax the pension or annuity under its domestic laws. As specifically stated in the IRS publication for “Taxation of Foreign Pension and Annuity Distributions”:

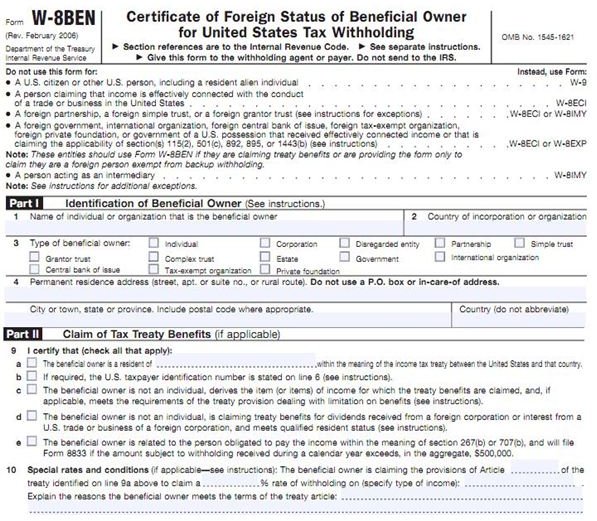

“If you live in a foreign country and receive a pension/annuity paid by a U.S. payor, you may claim an exemption from withholding of U.S. Federal Income Tax (FIT) under a tax treaty by completing Form W-8BEN and delivering it to the U.S. payor. You must report your U.S. Taxpayer Identification Number (TIN) on Form W-8BEN for it to be valid for treaty purposes.”

This simply means that in the event that you decide to retire in a foreign country and receive IRA annuities paid by a U.S. entity, you can only claim exemption from the 30% withholding tax imposed on ”employer-deferred compensation plans delivered outside of the U.S”, if you submit Form- W-8BEN, to the U.S. entity paying your annuity. The completed W-8BEN must contain your US Taxpayer Identification Number and U.S. Residence Address to render the form valid for tax treaty purposes.

Taxes on income earned by your IRA investment if imposed by the foreign country of residence can be treated, either as a reduction or as a tax credit that will reduce your U.S. tax liabilities.

However, IRS further states that each tax treaty is unique in the sense that a treaty that is recognized in one country does not necessarily denote its applicability to all other countries. Thus, the IRS emphasizes the need to read the Protocols of any such treaty, particularly about residency rules and the “Saving Clause”. In addition, you also have to consult with local state authorities whether they allow or honor the treaty provisions.

To learn more about tax treaties entered into by the United States with other countries, the IRS publication for “United States Income Tax Treaties - A to Z”, contains links to the treaty documents. (See our reference section for the related link).

Still, the matter of moving IRA accounts from the US requires careful study, inasmuch as certain IRS rules governing IRA investments could be violated if transfers are not properly executed.

Moving IRA Accounts Outside of US Territories

The following points of consideration require careful evaluation by seasoned tax professionals, in case you’re planning to move your IRA to offshore territories:

-

As a rule, the bank holding the IRA trust account may withhold a 30% Flat-rate Withholding Tax, if (1) employer-deferred compensation plans, (2) individual retirement plans and (3) commercial annuities are to be delivered outside of the U. S. Exemption from the withholding tax may be allowed only after satisfying Form W-8BEN and other requirements. See IRS 54 US Tax Guide for U.S. Citizens and Resident Aliens Abroad – (find the link in this article’s reference section).

Advertisement -

The offshore transfer of traditional funds from trustee to another is not considered a rollover and the transfer is tax free, if the foreign bank handling the account is an international bank with branch offices in the U.S. and provides IRA services.

Please proceed to the next page for more of the important points to consider when moving IRA account to offshore territories.

Moving IRA Accounts Outside of US Territories (continued)

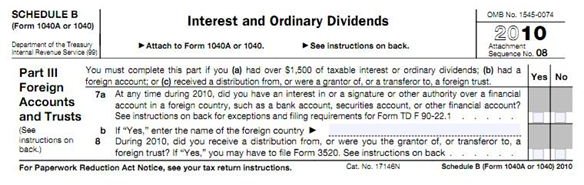

According to expert tax planners, there is no truth to the popular belief that offshore trusts present viable vehicles for tax avoidance. IRS requires the submission of Form IRS Form 1040, Schedule B, by April 15 each year. The form serves as a report of all existing offshore financial account over which you have direct or indirect control. The latter denotes those that you own even if placed in the name of a legal entity you control, such as a corporation, trust or LLC.

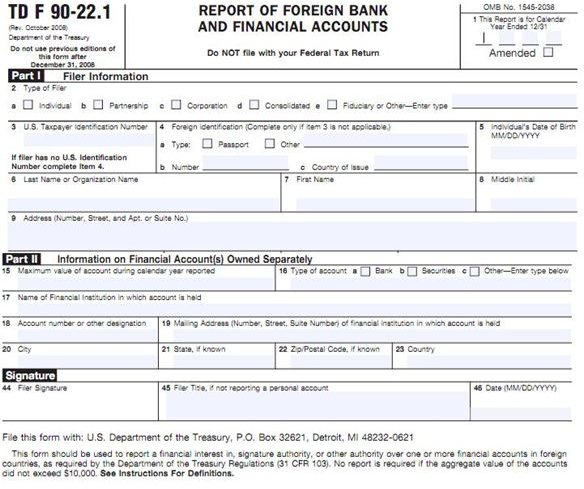

US Treasury also requires the submission of Form TDF 90-22.1 annually by June 30 from any U.S. person who has “a financial interest in, or signature authority over bank, securities, or other financial accounts in a foreign country which exceeds $10,000 in aggregate value”.

In fact, moving of IRA accounts to offshore units increases your visibility and exposure to IRS scrutiny, since numerous US income tax requirements related to transfer of assets and annuity transactions are in place. See IRS 575 Pension and Annuity Income – (find the link in this article’s reference section).

These include tax provisions for Transfers of Annuity Contracts, wherein the movement may be treated as tantamount to receiving a non-periodic distribution of the IRA account.

There is also the matter of observing the regulations pertaining to lump-sum distribution particularly if the IRA account is being moved to a non-qualified offshore account in a single tax year. Certain qualifying conditions have to be met for a transfer to be considered as not a lump-sum distribution.

A qualified distribution for Roth IRA, for example, is subject to the condition that it is made after the 5-year period, which commences on the first taxable contribution made to set-up the Roth IRA account; and that it is made on or after the owner has reached 59 ½ years of age. In fact, there’s a host of exceptions to consider in avoiding the 10% tax for non-qualified distribution.

Traditional IRA owners on the other hand, may have to pay 25% additional tax if a simple IRA is withdrawn or used before age 59 ½.

A retiree, who may be enticed by an offshore corporation to invest his IRA funds in a real estate property as a means to avoid offshore financial reporting, is not a foolproof tax avoidance guarantee. U.S. controlled offshore corporations are likewise required to submit their own reportorial requisites to support their income statements and balance sheet figures and your IRA investment may surface among those reports.

Summary:

The IRS requires all U.S. payers of annuities for employer-deferred-compensation plans, individual retirement plans and commercial annuities delivered outside of the U. S. to withhold a flat rate of 30% withholding tax, unless the documentations and conditions for tax treaty purposes are met.

Every U.S. citizen is taxed on all income categories even if one chooses to retire overseas since the IRS requires the reporting of all non-U.S. financial accounts held, owned and totaling $10,000 or more.

In the event that an IRA account is invested in real estate holdings outside of the U.S, any sale or transfers of ownership could be traced through other reporting requirements submitted by the party who facilitated the buying and selling of the property.

Moving an IRA account offshore is legal and could be simple. However, once your investment account starts earning income offshore, it would be best to consult with a professional tax planner to ensure compliance with all legalities and tax regulations.

Resources

Sources:

- Publication 590 -IRA –https://www.irs.gov/publications/p590/ar01.html

- Publication 575 - Pension and Annuity Income -https://www.irs.gov/pub/irs-pdf/p575.pdf

- The Taxation of Foreign Pension and Annuity Distributions –https://www.irs.gov/businesses/article/0,,id=187083,00.html

- US Tax Guide for U.S. Citizens and Resident Aliens Abroad - https://www.irs.gov/pub/irs-pdf/p54.pdf

- United States Income Tax Treaties - A to Z – https://www.irs.gov/businesses/international/article/0,,id=96739,00.html

Image Credits:

- State Department – via wikimediacommons/Gunnar_Lund

- IRS Tax Forms - Screenshot images were created for this article by the author.