Before digging into the dirty details of each of these major accounting scandals, we’ll take a look at some of the tools that were used to first detect them – including sophisticated accounting systems and advancements in high-tech communication.

Technology Fighting Against White Collar Fraud

Looking back at the 10 major accounting scandals that changed the business world, it was noted that most of their unraveling came about during the turn of the new millennium, which was a time when the American trade and industries were beginning to experience the benefits and detriments of high-tech computerization.

Information storage and communication became sophisticated, which made possible the compilation of hordes of information in an instant. Recording and verification of accounting transactions in realtime were made easier and more accurate, which facilitated the reconciliation of supporting documents versus sources, with very little effort needed.

Federal regulators were provided with data that revealed the corrupt practices of high-profile companies and their CEOs. Their bankruptcies became inevitable as the Securities and Exchange Commission (SEC) and financial analysts began to see the signs of irregularities among numerous companies. When the SEC ordered the restatement of their financial reports in accordance with the GAAP rules , it turned out that these companies were mostly founded by inflated revenues and negative financial conditions.

Soon enough, their reputations and financial credibilities began bursting like bubbles, in the wake of the ensuing investigations.

Investors once again lost their trust and confidence in America’s publicly traded companies, which eventually led to more bankruptcies. As a result, multitudes became jobless, and the trend went from bad to worse throughout the decade.

The Accountants’ Connivance in the Celebrated Accounting Frauds

In the midst of all these accounting anomalies, the accountancy profession and the role it plays came into focus. Accountants helped in misleading the public by certifying that the financial reports of fraudulent companies were true and correct .

Investors placed their faith in the accompanying audit reports, which served as certifications that the reported income and expenses as well as the assets, liabilities, and stockholders’ equity in the publicly traded companies had been verified and assessed. Basically, the certification carried a statement that the results of the business operation (net income) were all accounted for, by using generally accepted accounting standards and procedures, in accordance with the generally accepted accounting principles .

As we list the ten major accounting scandals, one glaring factor surfaces — six out of the ten companies were handled by Arthur Andersen, LLP, which was then considered as one of the top five US accounting firms. As the external auditor of client-companies, the firm’s auditors did not discover the accounting anomalies. In fact, it turned out that the firm was even responsible for the cover-ups as part of its extra-services as consultant.

In view of this, and before delving into the scandals themselves, this article will first examine what drove the accounting firm of Arthur Andersen to disregard its ethical and moral responsibilities.

The Underlying Factors That Gave Rise to Andersen Accounting’s Connivance

The Profit Conflict between Andersen Consulting and Andersen Accounting

Arthur Andersen, the person, had nothing to do with all the accounting anomalies that were attached to his name. He was the Northwestern University professor/accountant who founded Andersen Accounting (AA) firm, but he died in 1947. Years after his death, his accounting firm was reorganized into two divisions: Andersen Accounting and Andersen Consulting. Andersen Accounting was referred to as the main culprit involved in most of the major accounting scandals.

The timelines in AA’s history revealed that as early as 1986, it was already suffering from a chain of million dollar lawsuits filed by companies and securities investors for the firm’s failure to uncover internal frauds. All these led to the AA firm’s loss of reputation and loss of clients and to settlements that ranged from $30 million to $1.1 billion prior to the 2000 to 2003 accounting scandals.

Due to the accounting firm’s inability to generate company profit and heavy losses from the lawsuit settlements, the Andersen Consulting firm broke away in year 2000 and became a separate entity that now goes by its new name as Accenture. On the other hand, the Andersen Accounting division was left to face the numerous lawsuits on its own, and with only a few clients.

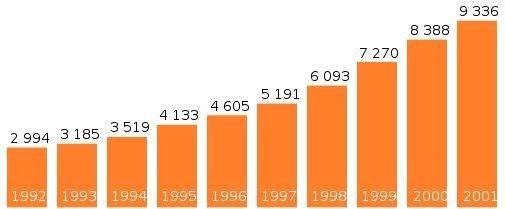

The CEO resigned right after the breakup, leaving AA and its accountants under the leadership of a managing partner named Joseph Bernardino. The accounting firm had to maintain its clients in order to survive, which entailed turning a blind eye to the accounting malpractices in exchange for hefty profits.

The chart on your left shows that Andersen Accounting was able to increase its revenues in 2001, even without the Andersen Consulting division.

Please continue to page 2 for more on accounting scandals.

The Enactment of the Public Company Accounting Reform and Investor Protection Act of 2002

At the end of the Enron investigations, the US Dept. of Justice saw it fit to charge the accounting firm Arthur Andersen and Co. with creating a system where incentives for profits goaded its employees into corrupt audit practices. As one accounting scandal came after another, this also brought to light the reality that the accounting system had no foolproof protection against connivance and conspiracy, needing to be backed up in some ways by stricter laws.

Eventually, the spate of corporate white-collar fraud made possible through fraudulent accounting practices culminated in the enactment of the “Public Company Accounting Reform and Investor Protection Act of 2002.” This law may sound unfamiliar because we all know it as the “Sarbanes and Oxley Act," after the names of its creators, Senators Paul Sarbanes and Michael Oxley.

Overviews of the Ten Major Accounting Scandals That Changed the Business World

I. Enron – Gas Trading, Stock Market Trading, and Accounting Manipulations

The root of Enron’s accounting problems was the manner by which the trading of its gas and oil products was being conducted. Investors were conned into believing that Enron was highly profitable by making it appear that the company’s energy commodities were heavily traded. The following were the highlights of Enron’s accounting scandal:

-

Enron’s selling activities were made to appear “robust” by way of “round-trip” trades and press releases about fictitious trade deals.

-

Substantial bank borrowings were channeled through bogus companies created by Enron. Through this scheme, money derived from borrowed funds were made to appear as funds derived from substantial trade deals.

Advertisement -

Enron’s stock prices rose through further trade manipulations, which included intentionally cutting off gas pipeline supply to entire regions, in order to create a scenario of limited supply but high demand.

-

Long-term trades were booked at anticipated market values. This allowed substantial profit realization upon recording of the transaction.

Advertisement -

Since round-trip trades were pre-arranged buying and selling ageements between companies to sell and buy back commodities at the same price, no actual profits were recognized. Yet trading appeared heavy, which thus enticed investors into buying Enron’s blue-chip stocks . Enron’s top officials were reaping millions in profit shares from out of the funds infused by investors and not from actual revenues earned.

-

As 2001 neared its close, the SEC noticed the irregularities in Enron’s financial statements — prompting this governing body to order the restatement of the energy company’s financial reports in accordance with GAAP rules.

Advertisement -

As SEC investigations progressed into a full audit examination, most of Enron’s key officials started exercising their stock option rights by selling their shares. Stock prices dropped from $90 to $36.88 per share.

-

Important documents were shredded at the Enron offices and at the Andersen Accounting firm, as ordered by David Duncan, the chief auditor-in-charge of AA’s Enron account.

-

As more investors withdrew their financial support, Enron subsequently declared bankruptcy by December of 2001, leaving more than 4,000 employees jobless and deprived of separation benefits, including retirement or pension funds.

-

Numerous investors were left holding wothless Enron stocks by the end of 2001.

Readers may find a more detailed description of Enron’s complex trading and accounting manipulations, in a separate article entitled “A Detailed Look at the Enron Accounting Scandal .”

.

II. WorldCom - A Case of Failed Business Projections Converted into Capitalized Costs

WorldCom was one of the largest global telecommunications companies and its long-distance telephone ventures failed heavily as technological advancements in communication took place. However, instead of recognizing as expenses the “line costs” incurred, the company’s Chief Accounting Officer, Scott Sullivan, ordered his subordinates to recognize as “long-term investments” the routine operational “line costs.” That was in order to avoid reflecting heavy losses in the company’s financial statements.

In the case of WorldCom, the company’s internal auditors discovered the anomalous accounting entries in 2002, which spurred the SEC’s full investigations. Initial results of SEC investigations disclosed about $9 billion worth of business transactions misstated as capitalized investment costs instead of routine expenses, in order to avoid declaration of losses. Final accounting of the anomalous accounting entries involved other capitalized expenses and fictitious accounts receivables amounting to $11 billion.They were all certified by Andersen Accounting as all in accordance with GAAP rules.

The revelations of WorldCom’s accounting scandal saw stockholders pulling out their investments. In July of 2002, WorldCom declared bankruptcy while 17,000 lost their jobs in line with the company’s bankruptcy reorganization. The company’s shares of stock plunged to 20 cents per share, which left some investors reeling from considerable amounts of investment losses.

WorldCom’s CEO Bernard Ebbers and CFO Scott Sullivan were incarcerated, as subordinates turned state witnesses to the criminal charges filed by the SEC for securities fraud in 2002.

Overviews about other major accounting scandals continue on the next page.

III. Waste Management – Distorted Accounting Methods for Depreciation and Amortization Expenses

Even before Enron and WorldCom, there was Waste Management (WM) Inc. whose financial statements were considered by the SEC as part of the garbage that the company was managing. As early as 1997, the Andersen Accounting firm was hired by WM to review its financial records, the results of which were presented by AA as “Proposed Adjusting Journal Entries.”

For five years, Andersen Accounting helped the top officials of WM “cook the books.” This was part of the special work that the accounting firm was paid to do for WM, which was outlined as “32 must-do steps.” Through those five years, the books of the company were actually made to conform to targeted projections through manipulated accounting practices.

In addition, a reserve account was maintained as a stand-by account to absorb whatever adjustments cropped-up during internal or external audit examinations. However, the purpose for the reserve account became questionable to investigators later on, and it was eventually proven by other external auditors as a “cookie-jar” reserve account.

The SEC had ordered a restatement of WM’s financial statement in 1998 by $1.7 billion. On the other hand, Andersen Accounting was ordered by the SEC not to sign financial statements in the future, along with a $7 million fine. AA’s promise was embodied in a consent agreement, which AA obviously broke, since it later signed WorldCom’s and Enron’s fraudulent financial reports.

Waste Management’s accounting manipulations are summarized as follows:

-

Depreciation expenses on garbage trucks were distorted by assigning large amounts of residual or salvage values, while useful lives were extended beyond what was prescribed by industry standards.

-

Other fixed assets, which previously had no salvage values, were re-computed by assigning arbitrary salvage values.

-

The value of the landfill sites were assigned with book values that did not conform to their reduced or degraded values as land filled with wastes.

-

Various expenses were capitalized in order to allocate the impact of WM’s wrong accounting practices for a period of 10 years. These were orchestrated and directed by the CEO and chairman of WM’s Board of Directors, Dean Buntrock, President; Phillip Rooney, COO; and James Koenig, EVP and Chief Financial Officer.

-

Based on the inflated revenues, top officials of Waste Management earned for themselves hefty amounts of compensation packages comprising substantial profit share bonuses, basic salaries, enhanced retirement benefits, and stock options, which were all practically derived from money infused by investors.

-

While formal investigations were going on in 2002, top officials of WM started cashing in on their stock options, which started the downward trend of WM’s stock price to more than 33%. In addition,The CFO ordered the destruction of important documents to obstruct investigations.

-

The company’s shareholders reportedly lost over $6 billion after the final accounting of the Waste Management fraud was completed. .

IV. The Baptist Foundation of Arizona – A Case of Proper Fund Accounting Ignored and Manipulated

Another major accounting scandal, and prelude to Andersen Accounting’s participation in Enron’s anomalous deals, was the illegal securities trading committed by the Baptist Foundation of Arizona (BFA).

BFA was the endowment managing arm of the Arizona Southern Baptist Convention (ASBC). It was a movement started in 1948 by a Baptist minister under tumultuous conditions, but it was continued under a renewed leadership by Bill Crotts, the Baptist minister’s son, in 1982.

Instead of relying on solicited endowments, Crotts cooked-up a scheme where the not-for-profit BFA could easily generate the funds it needed in order to build Baptist churches and carry on with philanthropic church’s works for Arizona’s poor sector. Initially, Crotts borrowed substantial funds from the ASBC, and later he convinced an estimated 11,000 elderly church members to invest their life’s savings and retirement funds. BFA’s annual financial statements presented fairly good track records of its past achievements.

Unknown to those investors, BFA’s fraudulent scheme involved bogus for-profit companies created by Crotts and his cohorts. These fake companies received the investments and used the funds in assuming the roles of buyers in BFA’s real estate buying and selling deals.The shady deals made possible the transfer of the church members’ investments into the coffers of BFA as legitimate cash inflow.

In truth, BFA was heavily indebted up to $100 million by the year 1999, and its actual losses reached $585 million because there were no actual profitable real estate deals–only fake transactions. In addition, BFA’s real purpose, which was building churches and helping poor members of church congregations, was forsaken for self-serving purposes.

Please proceed to the next page for the continuation of the BFA accounting fraud overview.

Continuation: BFA’s Fraudulent Fund Accounting Overview:

The Arizona Attorney General’s Office (AAGO) got wind of BFA’s illegal fund sources because the foundation was a non-profit organization and had no authority to seek investments. It took the AAG Office eight years, from 2001 to 2008, before the real estate properties held as assets by the BFA were liquidated in order to return the money invested by the elderly church members.

The AAGO was able to collect an additional $217 million from Andersen Accounting as settlement for its participation in certifying the non-profit organization’s fraudulent financial reports, which were mostly made up of fake fund accounting transactions.

Even Croft’s parents and sister were held on probation and were made to pay certain amounts in order to pay back the debts and the investors’ money. However, during the eight years of liquidation, most of the elderly investors either lived in poverty or spent their remaining lives in poor health while some reportedly died in the aftermath of the fraud’s discovery in 1999.

During the trials in the year 2000, some of Crotts’ cohorts turned state witnesses, which eventually led to Crotts’ imprisonment.

V. Global Crossing – Bankruptcy at the Heels of Enron’s Accounting Fraud Scandals

Global Crossing (GC) was another telecommunications network giant, which was established at the height of high tech communications development. GC’s case was similar to WorldCom’s failed business projections, overexpansions, and heavy borrowings, which were covered-up in similar ways to WorldCom’s manipulated accounting transactions. This should not come as a surprise, because Andersen Accounting was its financial consultant and external auditor. That was during the same period that the accounting firm was also acting as consultant to Enron and WorldCom.

Massachusetts Congressman Michael Capuano, who was part of the investigating panel of the Global Crossing’s fraud scandal, summarized the company’s activities, from its establishment in 1997 through its declaration of bankruptcy in January of 2002, in a single sentence — “You bought something you didn’t need, with money you didn’t have, and sold it to somebody who didn’t need it and didn’t have any money, and you hid the bookings.”

-

Global Crossing insisted on calling its deals with other telecommunication companies as “swap exchanges” and not the same “round trip trades” committed by Enron. However, it was all basically the same, because investors and creditors were made to believe they were quite active in closing successful trade deals.

-

Borrowed funds were made to appear as money coming from successful trade negotiations.

-

The maturing $12.5 billion debts were already being called on by the creditors, which thus forced Global Crossings to declare bankruptcy in 2002.

-

Among GC’s major future projections were deals that involved Enron, which turned out to be bankrupt as well, and was facing charges for the same practices that GC emulated through the help of Andersen Accounting.

-

GC investors started to divest as they became wary of the accounting anomalies committed by Enron and other energy and telecommunications giants. Still, other Global Crossings investors lost $54 billion, while more than 14,000 employees lost their 401k retirement funds.

However, GC made a difference in comparison to Enron and WorldCom because it was able to emerge from bankruptcy in 2005. Singapore’s state-owned investment company, Temasek Holdings Ltd., became its major owner when the latter paid off the majority of GC’s 12.5 billion debt.

VI. Peregrine Systems, Inc. – Inflated Revenues Through Fake Reselling Trades

Peregrine Systems, Inc. (PSI), an enterprise solutions software developer, initially found success during its early years of operations in 1981. However, the advent of the Internet and open source systems offered downloadable software that users could test; hence resellers of software products found it more lucrative to sell the more advanced systems.

Nevertheless, the software company was able to present financial reports that showed profitable results of business operations for 17 consecutive quarters, through Andersen Accounting’s consultancy and external audit services.

As part of the accounting manipulations, PSI’s resellers were convinced to receive the software goods delivered to them as consignment deals. Although this meant no actual money received, the objective was to move the company’s software stock inventory out of its offices and off its books.

That way, the consignment deals were recognized in PSI’s books as actual sales in the form of accounts receivables, albeit uncollected.

PSI’s books also recognized the famous “cookie-jar reserve account" as an additional buffer for the unreal sales. The software company’s revenues were overstated by $100 million dollars from 1999 to May 2002.

Find the continuation of PSI’s fraud overviews on the next page.

Continuation: Peregrine Systems’ Inflated Revenues Through Fake Reselling Trades

The substantial amounts of uncollected receivables and unjustified reserve account caught the attention of the SEC, and restatements of its financial reports were ordered.

As a result of the restatements, Peregrine Systems, Inc., was forced to declare bankruptcy in 2002 and blamed Andersen Accounting. Accordingly, the latter allegedly failed to advise PSI management that the company was using the wrong accounting practices in recognizing revenues, nor did it advise about proper treatment of uncollected bad debts .

Nevertheless, investigators saw through PSI’s fraudulent schemes because the company benefited from the accounting manipulations, as the prices of its shares of stock rose from $2.25 to $79.50 in 2002.

PSI’s CEO Stephen Gardner and EVP for Worldwide Sales Stephen Powanda sold their shares and gained profits in the amounts of $11 million and $24 million respectively. This was shortly before the SEC launched a full blast investigation into PSI’s financial records.

The company’s shareholders lost $4 billion in the software company, and in 2004 eight executive officers of PSI, including Gardner and Powanda, were indicted for grand larceny.

VII. AOL Time Warner – Recognition of Revenues from Barter Deals

American Online, which was more popularly known as AOL, acquired majority ownership of the underperforming Time Warner (TW). However, TW protected its corporate values in view of its role as the publisher of Time Magazine, a publication revered for its journalistic integrity.

Clashes between TW’s and AOL’s business practices led to the unraveling of the accounting scandals. Overviews of the underlying factors that lead to AOL’s financial and accounting troubles are highlighted below:

-

AOL dominated the Internet scene for four years, between the mid-1990s to1999, by entering into aggressive advertising contracts instead of charging subscription fees.

-

Internet advertising became a hit, and AOL’s stock prices rose astronomically. Due to this tremendous response from investors, enhancing revenues in order to keep the stock prices favorable for AOL TW’s stockholders became the core objective of the AOL management and its employees.

-

However, the year 2000’s slump in stock market trading due to numerous accounting scandals affected most of the companies that were into Internet advertising contracts with AOL TW. This also meant loss of advertising revenues for the latter.

-

To sustain the strength of AOL TW’s stock prices, AOL’s management resorted to accounting manipulations by recognizing off-book revenues, like:

(a) Recording of pre-booked advertising contracts were made twice, notwithstanding that they were already recognized as pre-booked revenues;

(b) Assigning overvalued amounts to advertising contracts as ways to inflate revenues; and,

(c) Dollar values of advertising deals entered into as barter trades with other companies were recognized as legitimate sales.

-

The barter trades were actually entered into for the purpose of making AOL’s advertising offers look lucrative by faking trade deals. Customers were given free advertisements just to make it appear that they closed advertising contract deals with AOL Time Warner. The dollar values of the barter deals amounted to as much as $30 million. This of course reflected large revenues and boosted stock prices.

-

The SEC finally got wind of these shady advertising revenues and accounting manipulations, and the ensuing fraud investigations subsequently caused AOL Time Warner’s stock prices to drop to $8.70 per share or as much as 85% in reduction of its value on the trading floors.

In 2003, the Board of Directors and major investors booted out the AOL CEOs and handed over the management to Time Warner’s top executives. To regain its tarnished reputation, the AOL trade name was dropped and AOL trading was reduced into becoming a division of the Time Warner company.

VIII. HealthSouth – Accounting Manipulations in the Healthcare Industry

In 2003, the SEC filed civil charges against HealthSouth for misleading public investors by presenting overstated and fraudulent financial statements. In relation to the SEC’s formal inquiriess, a forensic investigation was conducted by PricewaterhouseCoopers to determine the extent and value of the accounting misdemeanors that took place from 1997 through July 2002.

During the years reviewed, the CEO and key finance officers of HealthSouth boosted the company’s revenues by way of the following manipulations:.

- Deferred revenues from prepaid health coverages were recognized in full instead of adhering to the matching of cost and revenue principles.

- Other revenues from healthcare coverages were overvalued.

- Routine operational expenses were capitalized or deferred as expenses in order to understate the year’s annual expenses and to further inflate revenues.

- The infamous “cookie jar reserves” were also used to absorb income deficits.

PricewaterhouseCoopers uncovered a total of $1.4 billion in systematically overstated income, which began from 1999. This was in addition to the $1.1 billion identified by the US Justice Department from HealthSouth officials’ admissions of overstated earnings.

HealthSouth joined the list of publicly traded companies that manipulated their accounting records as the means of deceiving stock investors.

IX. Adelphia Communications - A Case of a Publicly Owned Company Used as Family Piggy-Bank

Adelphia was a cable TV company that ranked as No. 6 in America’s cable TV industries. A financial analyst discovered $1 billion worth of off-the-book dealings linking Adelphia funds to entities owned by the Rigas family. This spurred a spate of federal investigations in 2002, which led to the arrest of John Rigas, the founder-CEO of Adelphia.

The arrest likewise prompted the cable company’s investors to withdraw their financial support and the creditors to call in their loans, in which charges included the following:

-

The Rigas family used Adelphia as collateral for private loans in 1996, which was, of course, kept hidden from its investors.

-

The family instructed its accountant to inflate cable TV subscriptions to mislead investors that the company was experiencing tremendous growth rates.

-

Subscriptions from customers coming from non-Adelphia transactions were counted as part of Adelphia’s cable TV revenues, including those who placed orders for home security systems.

-

The family splurged on various expenses, including ventures into film making, which was estimated to have reached $3 billion dollars. These expenses were disguised as legitimate company expenses, albeit overly bloated and obviously self-serving.

-

Adelphia’s funds were used to pay for timber rights allegedly worth $25 million, which the cable TV company later sold to the Rigas family for only $500,000. In addition, cable TV funds were also used to build a golf course for the Rigas family.

In 2007, John Rigas and his sons were indicted for looting Adelphia’s coffers by using the company’s funds for self-serving purposes. However, due to the elder Rigas’s failing health, his sentence was reduced to 15 years.

X. IMClone Systems - A Case of Insider Trading

The CEO of IMClone Systems Sam Waksal was indicted for insider trading and implicated his friend, Martha Stewart, the respected icon in the housekeeping and home designing industry.

Waksal, who received a tip in December of 2001 that the US FDA was going to reject his application for a colon cancer drug, sold 80,000 of his company’s shares one day before the FDA handed down its rejection of the drug. He also instructed his daughter, his father, his friend Martha Stewart, and other IMClone shareholders to sell their shares. As a result, the prices of IMClone’s stocks dropped from $60 to $6.68 per share.

Waksal was guilty of the illegal type of insider trading since he violated his fiduciary duty to the stockholders by placing his own interests and those of his family’s and his associates’ ahead of the shareholders’ interests, who would buy and sell IMClone stocks based only on public information about the company.

In June of 2003, Sam Waksal was sentenced to seven years in prison and paid fines totaling $4 million dollars for being found guilty of the insider trading charges. Stewart, likewise, served time in jail for five months.

How the Sarbanes Oxley Act Changed the Business World

The Sarbanes Oxley (SOX) Act was based on a careful study of all the malfeasance and manipulations committed in the spate of accounting scandals that rocked America in the early years of the 21st century’s first decade. The laws implemented by the SOX Act brought about changes that deal heavily with offenders and do not excuse anyone from ignorance of the GAAP accounting rules and policies.

Readers may refer to a separate article entitled An Overview of the Sarbanes Oxley Act to get more insights into how these ten major accounting scandals changed the business world.

Reference Materials and Image Credit Section:

References:

- Forbes.com :The Corporate Scandal Sheet https://www.forbes.com/2002/07/25/accountingtracker.html

- Public.Kenan-Glagler.UNC.Edu: Corporate Earnings: Facts and Fiction:– https://public.kenan-flagler.unc.edu/courses/mba/mba733/Lev,%20Corporate%20earnings%20facts%20fiction,%20Dec%202002.pdf

- What went wrong? Accounting fraud and lessons from the recent scandals—https://goliath.ecnext.com/coms2/gi _0199-10239964/What-went-wrong-Accounting-fraud.html

- Accounting: Concepts and Applications: By W. Steve Albrecht, James D. Stice, Earl K. Stice, Monte R –https://books.google.com.ph/books?id=sYlWqWB0sz4C&pg=PA17&lpg=PA17&dq=10+Major+Accounting+Scandals+That+Changed+the+Business+World&source=bl&ots=mUikdDar1k&sig=hEhVgCrfKYeWpKq9TBnyhpwSpxs&hl=en&ei=wYMQTdnQFYG8caix6coK&sa=X&oi=book _result&ct=result&resnum=5&ved=0CDkQ6AEwBA#v=onepage&q&f=false

Image Credits from Wikimedia Commons:

- Innansicht Festplatte 512 MB von Quantum, SPBer

- Andersen’s revenue (artist unidentified)