Don’t you just love it when President Obama promises tax credits for small business owners (think healthcare here), and then journalists everywhere find ways to shoot the program in the foot on why it won’t work. Do you only hire part-timers? Could it be maybe you’re to blame?

What Part-Time Jobs Used to Mean

When we were youngsters in high school and college, a part-time job meant the soda fountain (for us baby boomers), being a summer lifeguard and paper routes. As baby boomers started having babies of their own, the “part-time” job became “job sharing” because it sounded time-trendy and was a venue for working parents to share a job with another co-worker, decreasing the number of hours worked per week in order to spend more quality time at home.

Job sharing actually worked because before healthcare got so out of control: Usually one family member, partner or spouse had a full-time job where benefits covered family healthcare expenses.

These days, part-time jobs mean no benefits. Ask workers from large supermarket chains and big box stores, and they’ll tell you their hours have been cut, essentially making them part-time workers so they don’t qualify for company benefits such as healthcare. Or, there are less and less full-time job offerings so today’s employer can skip offering benefits.

Since the economy debacle and with unemployment rates as high as 10 percent in some areas, many business owners are opting for the part-time venue. Why? It’s cheaper, not just for healthcare, but for other employee expenses such as workman’s compensation and retirement benefits. Literally, a benefit plan, depending upon how it’s set up, can exclude those working on a part-time basis. Business owners who say downsizing is the key really do have a point—they simply can’t afford the cost of hiring full-time employees because those full-time workers want benefits.

Before I get angry comments from those who can’t find a full-time job or have had hours cut so they are now part-timers, let’s look at some business owner costs.

CNN Money journalist Catherine Clifford quotes small business owner Jo Heinz (owner of Staffelbach an architectural firm in Dallas) in her article, Need a job? Forget the Benefits:

“Everyone’s focus right now is controlling cost” and contractors and part-timers “are going to get the nod before the individuals who are looking for the full (benefit) package .” Heinz also offers that depending on salary levels, a benefit package can cost the small business owner between 20 to 25 percent over and above the base salary of a full-time employee—and she’s right. Business owners simply can’t afford to spend more when cash is so tight and sales are down.

Another small entrepreneur, Maxine Turner of Cuisine Unlimited, tells reporter Clifford “a chef making a base salary of $55,000 costs Turner $13,800 a year in benefits, including health insurance, retirement and personal time off.” However, unlike some employers, Turner is happier sticking with her full-timers because of the motivation, production and happy workplace environment she is able to achieve where, out of her 80 employees, 60 are full-time.

Many of my readers know I recently moved from New Mexico to Texas, and the company my husband now works for does offer healthcare benefits but contributes nothing to the monthly premium—even for the employee. What they are able to do is offer a lower cost group rate to their employees and some, depending on age, can get great healthcare for around $200 per month. For the older employees (40 plus) the monthly nut is higher—around $400 per month and to add the spouse and kids, employees (and I’m not kidding) can spend up to $1,200 a month on healthcare. So what’s their take-home pay look like—fifty bucks?

Your employees may hate you, but gone are the days when the small business owner could afford to participate in all elements of a benefits package. Some business owners either opt to drop benefits totally or decrease the percentage portion they contribute. For example, some still offer retirement options but no longer contribute a percentage or match the employees’ contributions.

Employees Don’t Get It

Sadly, most employees don’t understand what it truly costs to employ them, and even the Obamacare tax credits for the small business owners impose some restrictions. To receive the tax credit, you must employ 25 employees or less, have average annual wages of $50,000 or less and must contribute at least 50 percent of the healthcare premium costs. This is not a tax credit folks, this is a fairy tale.

Why do I compare these healthcare tax credits to fairy tales? I have owned and operated many small businesses—all with 25 employees or less. I can see where I would qualify for meeting the 50 percent employer contribution in premiums, (although health care is SO expensive and before my businesses were shut down, I was offering only a 40 percent employer contribution), but I wouldn’t have qualified when it came to the average wages of $50,000 or less—this means your annual payroll divided by the number of employees you have. So it’s a fairy tale to some business owners and I for one did not receive the little IRS post card telling me any of my businesses would qualify for this credit for wages paid in 2010. My average payroll was not $50,000 or less and unless you’re very, very small, most business owners won’t meet this requirement.

To show you how I wouldn’t qualify, in 2010 for one of my businesses the total wages I paid out were $512,748 and I had 10 employees ($512,784 / 12 employees = $51,275 so my average payroll was over $50,000. Some may say, heck you paid your employees well, but in the auto industry it’s the nature of the beast and those who have worked in and around the industry know flat time hours for mechanics can add up quickly.

On the other hand, say you did pay out annual wages of $250,000 and had 10 employees - this would make you eligible because your average payroll would be: $250,000 / 10 employees or $25,000. Here, I must point the latest poverty wages for a family of four is $22,350 so if a family is depending on a one-income household making $25,000, shame on the employer because that’s only $2,650 above the poverty level. Don’t forget these are gross wages, not net wages after required tax and other deductions.

Then there are the forms from the IRS. Yes fellow entrepreneurs, the IRS wants us to fill out more forms on top of the ones we already have to fill out—which are multiple and lengthy. This new tax credit form (if you even qualify) is Form 8941 (a link to the form can be found in the reference section below).

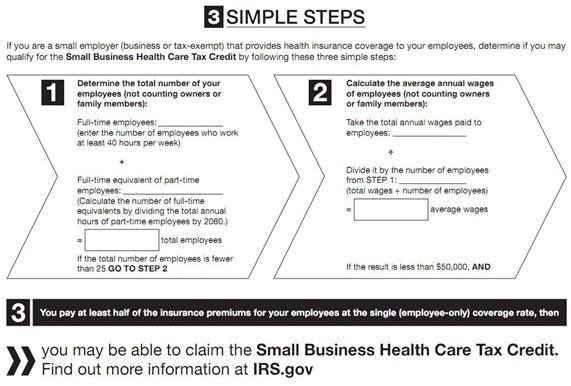

I would be remiss if I didn’t mention how much of a tax credit one could receive in Sleeping Beauty Land. Well, first you must fill out a fact sheet – another IRS form (seen in screenshot below). I should mention that if you do employ some part-time workers, you can add their total hours up as well on the worksheet/fact sheet.

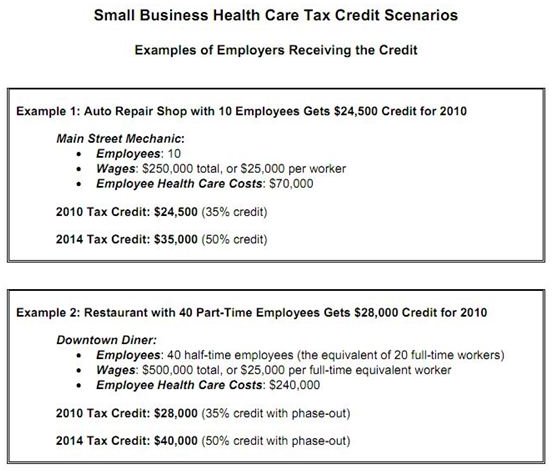

If you do qualify, the screenshot below shows how the credit works:

An employer (if he qualified) was offered a 35 percent tax credit in 2010 and in year 2014,the tax credit will be 50 percent (if Obamacare holds up and isn’t voted out). Note in the screenshot part-timers and those tax credits are “phased out.” Pay attention to the fine print in the screenshots above as well, especially the first one. It does say once you calculate your average payroll you “may be able to claim” the tax credit. “May” does not mean “can” or “will” here folks.

Don’t fret, however, because if you are as confused as most, you can read the IRS publications IR-2011-90 or IR-2010-117 (again links to both provided below). Actually, to take the mystery out of the credit, just call the IRS and ask them to explain it to you and offer the official IRS representative your scenario—because their scenarios are usually not the average business.

Additionally, a tax credit doesn’t put money in a business owner’s bank account so it doesn’t mean they’ll be getting cash to help pay for healthcare or other benefit premiums. A tax credit is filed with the company’s tax return and, sure, it’s a great credit. Most business owners, however, will tell you they don’t have the cash to begin with to pay for benefits and a tax credit does nothing but add a deductible expense on the annual tax return—so the government is not “handing out money” to help pay for Obamacare. Nor should a small business owner expect an official IRS check in the mail to help pay for benefits.

A Cranky Workforce

People looking for jobs are cranky and they should be. Business owners can’t afford full-time workers when hiring two people to do one job is cheaper. Of course you could be the Scrooge of the small business world and cut all benefits before you’re forced to offer them by Obamacare, cut your full-time workers hours so they aren’t eligible for benefits or simply hire only part-timers, but are you really benefiting from any of these decisions?

As an entrepreneur, I must say, no—you really aren’t. All you are doing is making your existing staff angry, and job seekers don’t want to work for you either. Further, if you have a happy and content workforce, one sure way to turn it into a sour grapes workforce is to cut benefits and hours and introduce your happy staff to the new part-timers Jane and John you just hired to pick up the slack.

It’s really a Catch-22 situation. Business owners need employees and employees need business owners to hire them. However, employers can’t afford benefits and employees can’t afford working only part-time or in jobs offering no benefits. No one wins really—no one at all.

Is This Fixable?

Because our two main political parties seem to hate each other of late and are more interested in “I won’t vote for what you want simply because you’re a Democrat” or “I won’t vote for what you want because you’re Republican” has gotten so silly these days, I’m sure nations around the world are laughing at us. And, these are not just chuckles but outright belly-holding, can’t-catch-our-breath laughs. Aren’t you a little embarrassed, Washington? I would be.

As far as whether this mess of hiring only part-time workers in order for your business to survive is the only foreseeable future, I say yep, for sure and hire away but expect much dissension.

While it may not be fair to job seekers everywhere, if you can’t afford full-time employees with benefits and you try to maintain the unaffordable, you’ll quickly find your business defaulting on what most small businesses default on first–IRS employee taxes–and then before you know it, you’ll owe so much on back taxes and penalties, you may be forced to close your doors. You’ll still have to set up a payment plan with the IRS because they never forgive 941 employee taxes—for any size business (don’t believe the ads you see on television—instead, call the IRS and ask if you don’t believe me).

So, I’d say to job seekers out there—you better be at the top of your game and if not, find a way to get there fast even if that means agreeing to less hours and lower or no benefits and never, ever complain. If you’re on the average scale, don’t be surprised if you’re passed over; and business owners everywhere—if you’re forced to hire only a few or part-timers only, be picky about who you hire.

There is really no great solution here, but it’s true that more small business owners are cutting benefits in order to lower overhead costs, and one way to do that is employing part-time workers.

If you’re a small business owner, what do you think of the healthcare tax credit? Did you qualify for the credit in 2010 and did you apply for it? Are you hiring only part-timers or cutting hours to avoid paying benefits or have you had to cut and trim your benefit package ?

Maybe if business owners everywhere start a real discussion on this topic, our brilliant minds may be able to figure out how to fix this. What are your thoughts—better yet, drop me a comment and let’s start this discussion right now!

References

-

Clifford, Catherine - CNN Money – “Need a Job? Forget he Benefits ” August 11 2011.

-

IRS Form 8941 – Credit for Small Employer Health Insurance Premiums

-

Image Credits:

Barack Obama in NH / Wikimedia Commons / Marc Nozell / C.C. 2.0 License

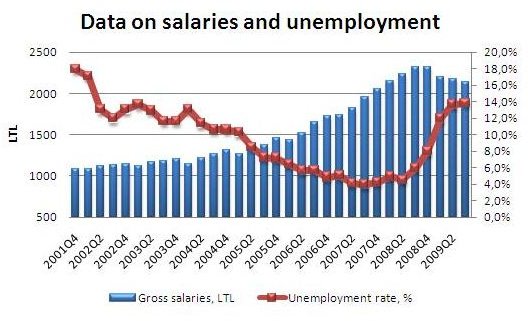

Salaries and Unemployment / Wikimedia Commons C.C. 3.0 License

Screenshot of IRS Fact Sheet by author from the IRS

Screenshot of IRS Health Care Tax Credit Scenarios by author from the IRS

-

Download IRS Publications IR-2011-90 and IR-2010-117