The IRS debacle about changing depreciation methods, came from court litigations filed by the agency against several businesses that claimed substantial tax refunds. The cases resulted in court decisions which refuted the IRS tax rules for changes in accounting methods related to depreciation.

The Conflicting Issues about Modifying Depreciation Methods

Taxpayers should increase their awareness about the Internal Revenue Service’s regulations about changing depreciation methods . The IRS maintains that modifications in accounting methods include replacements of recovery periods or useful life as a basis for calculating depreciation expenses.

Numerous tax litigation cases were filed by the IRS against several businesses, as the latter were assessed for unauthorized claims of tax refunds. The claims were based on depreciation cost adjustments computed by using a shorter recovery period, different from what they used in previous years.

However, conflicting court decisions had muddled the issues associated with changing depreciation methods by using a different recovery period. There were court decisions that disqualified changes in recovery period or useful life of the asset as analogous to a change in accounting. Still, despite the IRS’s defeat, the tax agency still maintains the same position regarding altering the estimated life or recovery period in calculating depreciation.

Nevertheless, there were certain qualifications that resulted in court decisions in favor of the tax agency’s contention that the change in recovery period involved a change in accounting method. The following sections examine the underlying circumstances regarding this particular tax regulation.

The IRS Rules for Changing Accounting Methods

IRS Revenue Procedures 97-37 under Section 446-Income Tax Regulations provide that a change in method of accounting includes a change in the overall plan of accounting for gross income or deductions or change in the treatment of any material item.

Section 446-e states that except as otherwise provided, a taxpayer must secure the consent of the IRS Commissioner before changing a method of accounting for income tax purposes.

Another clarification to this tax regulation is the Internal Revenue Service’s position that this includes changing the methods of calculating depreciation costs based on “Cost Segregation Studies.” It was noted that most of the issues about changing depreciation methods stemmed from the taxpayers’ initiatives based on said perspectives.

What Do “Cost Segregation Studies” Entail?

The engineering department of the IRS recommended that, for tax purposes, the proper way of determining the depreciation expenses of lump-sum building construction costs is to make a careful study of the depreciable items included in the building. Accountants should classify and segregate the property costs into those falling under Section 1245 from those that qualify under Section 1250. The IRS referred to this as Cost Segregation Studies.

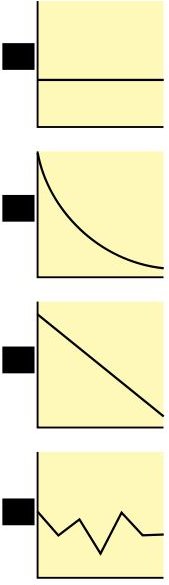

Section 1245 refers to equipment, furniture, and fixtures built as part of building constructions costs and are categorized as personal tangible assets . The latter includes building occupancy items such as wall coverings, doors, lighting fixtures, cabinetry, and the like The cost recovery periods for these occupancy items is 5 to 7 years and items are eligible for accelerated depreciation or using the double-declining balance method.

Section 1250 refers to buildings considered as 39-year property for which the straight-line method of computing depreciation is being used.

The Issues about Changing Depreciation Methods Based on Cost Segregation Studies

-

The IRS maintains that the matter of cost segregation studies were only recommendations coming from the tax agency’s engineering department and should not have been recognized as an official IRS publication.

-

Based on these recommendations, however, some accountants came up with computations that presented previous years’ income adjustment by way of depreciation expense increments. In recognizing increments in operating costs, they presented tax returns adjustments and claimed tax refunds.

Advertisement -

Recall that for 1250 building costs, depreciation is computed on a straight-line basis for 39 years: Any changes in depreciation costs that pertain to reclassification or reallocation of building costs into a 1245 tangible property entail a change in accounting method. Computations of depreciation costs under the 1245 section are based on the accelerated recovery or double-declining method for 5 to 7 years.

-

Although the act of claiming for tax refunds may have been legitimate based on the cost segregation studies, the IRS considered them as unauthorized, because there were no applications submitted for approval regarding the change in accounting methods via IRS form 3115.

Advertisement

In view of the pending movement to adopt IFRS accounting standards , the IRS’s advice to business owners is first to seek proper consultation with the tax agency’s Change in Accounting Method Technical Advisors. This should be done before pursuing tax refunds resulting from changes in depreciation method. That way, there is proper guidance in its implementation and before putting into effect any claims for tax adjustments and refunds. This procedure, of course, involves the submission of application for change in accounting methods.

Reference Materials and Image Credit Section:

References:

- Rev. Proc. 97–37 –https://www.unclefed.com/Tax-Bulls/1997/Rp97-37.pdf

- Cost Segregation ATG - Chapter 6.2 Change in Accounting Method –https://www.irs.gov/businesses/article/0,,id=134669,00.html

Image Credits:

- 4 Depreciation methods

- Queen Victoria Building interior.jpg

- [Hotel interior (Thimphu)](https://commons.wikimedia.org/wiki/File:Hotel_interior_(Thimphu)_-Blend_of_Traditional_a nd_Modern.jpg)