Calculating EBIT is as simple as calculating for net profits before the corresponding income tax provision is applied. This article explains not only the formula for EBIT but also the significance of its concept and how it is used by financial analysts in evaluating a borrower’s credit worthiness.

Understanding the Formula for EBIT

Calculating EBIT is as simple as determining the business profit by deducting all expenses directly incurred in generating the gross income earned during the year. Anyone who knows how to read the Income Statement report of the company can easily learn how to calculate EBIT, since the format of said report follows the same formula observed in calculating EBIT, i.e.:

Gross Income - Cost of Goods Sold - Operating Expenses = Net Profit before Income Tax or Earnings Before Income Tax

Since EBIT is merely an acronym for Earnings Before Income Tax, which is basically the same as Net Profit before Income Tax, what could be the significance or the rationale behind the use of the term EBIT?

The Significance of EBIT

As a rule, business loans are granted for expansions or investment purposes, and approvals are usually based on the premise that the intended expansion or venture will be self-liquidating. This means that the money borrowed to finance a certain business undertaking can be repaid from the funds generated by its operations.

EBIT is a term used by creditors for their credit risk analysis of a proposed loan. Credit processors, financial analysts, and the loan approving committee have to be clear as to which income to evaluate. It is important that in the performance of their functions, they have a uniform basis in determining the actual earning capacity of the business. Said capacity should be more than enough to pay-off the loan being applied for by the applicant-borrower.

The rationale in establishing EBIT is to make sure that any future loan payments that the company makes will have no effect against the company’s operational funds. The conclusion drawn from this analysis is that once the creditor grants the loan, the business will continue to operate as a profitable “going concern .”

The Uses of EBIT

The following are the main uses of the EBIT concept:

-

EBIT is a measurement of credit risk before a loan is granted and not so much as a tool for determining the profitability of the company as an investment outlet.

Advertisement -

EBIT is the basis used by financial analysts of financing companies in determining the margin of safety before recommending the loan for approval.

-

Once the credit risk or margin of safety is determined, the financial analyst or credit processor of a bank or a financing institution will have a basis for whether or not to recommend additional collateral. This is to ensure that the lending company’s credit exposure is adequately covered.

Advertisement

However, financial analysts are also wary of income statements that reflect substantial amounts of Earnings Before Income Tax, due to previous cases of accounting manipulations. Hence the best indicator to support the reliability of a high EBIT figure is still the borrower’s high credit score.

Example of Calculating EBIT and Analyzing the Borrower’s Credit Worthiness

To illustrate how creditors evaluate credit risks by calculating the EBIT, the following givens are provided in order to present an example of its use in credit analysis:

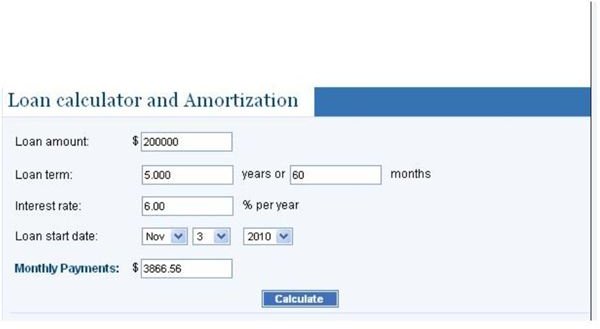

(1) The Greenability Co. is currently applying for a $200,000 loan payable in five years at the rate of 6% p.a.

(2) Monthly loan amortizations were computed at $3,866.56

(3) The income statement submitted by the company reflects the following highlights pertaining to the results of the company’s operation for the year:

Gross Sales - $285,000

Cost of Goods - $57,000

Gross Profit - $228,000

Operating Expenses - $148,000

Net Income or EBIT - $80,000

Income Tax Payable - $4,800

Net Income for the Year- $75,200

EBIT Analysis of the Company’s Loan Application

-

If the bank approves the said company’s application for a $200,000 loan, the company is bound to incur total additional expenses of $47,839.72. This will be derived from the income it will generate for the next five years of operations from the date the loan will be granted.

-

The said amount represents total loan payments every year computed by multiplying $3,986.66 x 12 months.

Advertisement -

Based on this, it is important that the applicant-borrower has the capability to generate annual income of more than $47,839.72 for the next five years.

-

The Greenability Co. reflects an EBIT of $80,000 in its last income statement, denoting income earning capacity that could adequately cover the expected total annual loan payments.

-

There is also a comfortable margin of allowance by which the company could sustain minimal increases in its operating expenses.

-

However, since it is expected that the loan will be used for business expansion, the credit analyst can reasonably expect that there will be growth in EBITs to be reported by the company within the next five years.

-

Otherwise, a decreasing trend should be closely watched by the creditor, since this will diminish the company’s capacity to pay the outstanding loan.

As an added note, financial analysts for investors, who will use EBIT as gauge for the profitability of the company, should take into consideration the annual loan payments. Analysis should include calculating the annual EBIT less the expected annual loan payments in order to determine the true profitability of the company.

Reference Materials and Image Credit Section

References:

- Investowords.com-EBIT https://www.investorwords.com/1631/EBIT.html

- Bankrate.com Loan Calculator and Amortization https://www.bankrate.com/calculators/mortgages/loan-calculator.aspx

Image Credit: