The usefulness of preparing a trial balance as a tool for checking the accuracy of general ledger accounts does not entail reliability for checking the overall accuracy of accounting records. This article gives examples of what a trial balance does not tell to ensure the veracity of financial data.

Distinguishing the Types of Errors that a Trial Balance Cannot Tell

What a trial balance tells you after proving the equality between the total of accounts with debit balances and the total of those with credit balances is that all your left column entries create the same effect on your right column entries. What a trial balance does not tell you is the accuracy of the data used in passing those entries.

In a separate article entitled Sample Unadjusted Trial Balance Worksheet , we illustrated examples on how to look for common errors that create imbalances in the total debits and total credits. However, most inaccuracies presented are examples of mechanical errors.

What a trial balance does not tell you are the human or judgmental errors that influenced the creation of improper accounting entries. There is no built-in mechanism in the trial balance system that allows automatic detection of misclassified accounts or of miscalculated amounts.

The following sections provide examples of possible human errors not detected by way of trial balance worksheets. These mistakes can affect the overall accuracy of financial reports, and their impacts are further evaluated if material or immaterial and in some cases unintentional or indicative of fraud.

(1) Omitted Transactions

A single act of omission may result in different types of human errors, as illustrated by the following examples.

Example:

A new customer paid the required customer’s deposit for renting DVDs/ CDs. However, the sales report for the day showed all cash received by the sales clerk as Sales from DVD Rentals, including the amount paid as the customer’s deposit by the new customer.

The bookkeeper merely picked up the totals of the sales report as transactions for the day and made the following entry:

Dr. Cash __________________xyz

Cr. Sales Receipts from DVD Rentals __________________xyz

The bookkeeper’s trial balance showed that all his debit and credit entries were balanced and the cash on hand tallied with the records. The trial balance was unable to tell if the right income recognition procedures and principles were observed. In this case, the customer’s deposit should have been recorded as a prepaid liability and not as revenue.

Implications: At this point, the Sales Receipts from DVD Rentals carries an overstated amount. Overstated income if not detected prior to the filing of tax returns will result in overpayment of taxes. In the long run, the Customers’ Deposits account will result in negative balances once charges against this account are made because not all customers’ deposits were properly recorded as such.

Remedies: Business owners should see to it that sales reports prepared by persons handling the sales transactions as well as all transactions during the day, including inventory movements, are properly reviewed by another staff, if the owner cannot perform them himself.

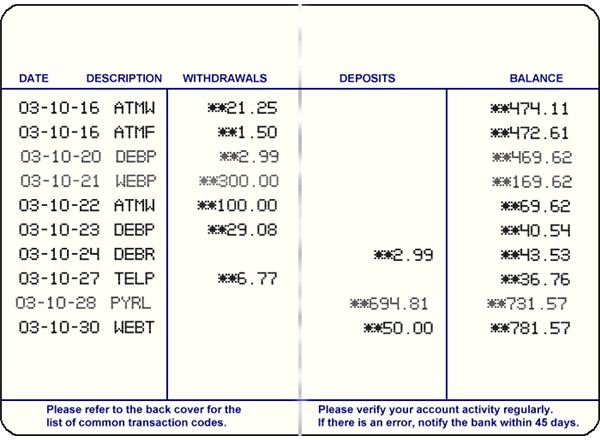

(2) Misposted Transactions or Postings to the Wrong Account

A misposted transaction can create repercussions not only to the detriment of the business but to the customer as well.

Example:

A cash deposit for Savings Account No. 123 was encoded in the teller’s validating machine as a cash deposit for Savings Account No. 132. The teller’s input will automatically reflect on the records of SA No. 132, while none will appear on the records of SA No. 123.

The trial balance for the day’s transaction was balanced since all transactions involving cash deposits and withdrawals were properly recorded. However, what the trial balance does not tell is that Savings Account No. 123 is understated while Savings Account No. 132 is over-credited.

Implications: If the depositor of SA No. 132 withdraws the entire amount reflected as deposited in his account, the withdrawal will still appear as a regular transaction. However, if a check clears against the rightful deposit account, which in this case is SA No. 123, there’s a possibility that the check will be returned for insufficient funds, and the customer’s account will be penalized with overdraft charges.

The owner of SA No. 123 can file a lawsuit against the bank for mishandling his account and make further claims for indemnity for damaging the depositor’s reputation, caused by the inappropriately returned check. On the other hand, the bank can take remedial actions against the holder of SA No.132 for withdrawing funds that were not rightfully his. This has to be settled in court though, because the bank has to show proof that the depositor’s action was not in good faith. Regardless of the outcome, the bank’s reputation is at risk for not exercising due diligence in handling their depositors’ accounts.

Remedies: All automated transactions for the day should be reviewed for possible human errors. Computers are only capable of automating the accounting system based on inputs supplied by humans. A control officer, usually the accountant, should also check the frequency of misposted deposits or withdrawals and determine if there’s any possibility of fraud involved.

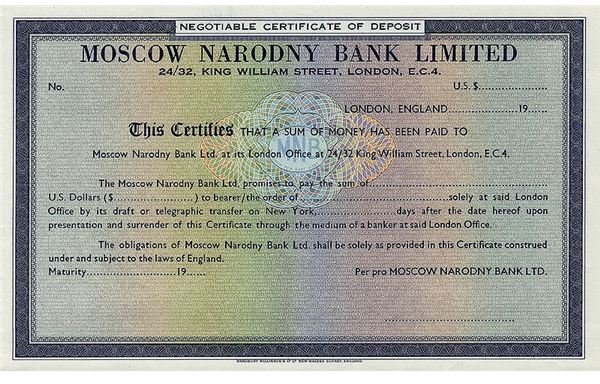

(3) Miscalculated Transactions

Computer-generated amounts used as the bases for accounting entries rely on human input–thus, the matter of “trash-in-trash-out cycle” will take place, which refers to wrong computer output caused by wrong human input.

Example:

The information about a Certificate of Deposit for $50,000 to earn 3% interest p.a. for a one-year term is entered as a 30-day CD. The trial balance for the day will not result in any imbalance inasmuch as debit and credit entries are correct. The trial balance is unable to tell that the computer will be basing its calculations on wrong data. Succeeding entries related to interests will appear as regular transactions, albeit using miscalculated amounts.

Implication: The computer will automatically compute the interest rate at 3% for 30 days only; succeeding rates computed thereafter will be based on the savings account interest rate. Since the customer placed the CD under a one-year term, he will expect interest credits computed at 3% throughout the term. If the customer is not so knowledgeable about interest computations, the error will only result in disappointment and the customer will consider transferring his account to another bank. However, if the CD interest is substantial and vital to the customer’s future cash position or relationship with his own clientele or associate, a knowledgeable customer can have reasonable grounds to file complaints for unfair trade practices.

Remedies: The control officer should see to it that computer-generated item counts for per-term classification should tally with the actual certificates. Any discrepancy should be thoroughly reviewed or checked to preclude the manipulation of interest differentials being funneled to other accounts.

Summary:

These examples of human errors are representations of trial balance limitations. The remedies always involve manual review and checking to allow room for evaluation whether the errors require further investigations. In most cases, errors like these are discovered as they arise from depositors’ complaints or during post-audit examinations. It is still possible for internal auditors to miss these types of errors, especially if audits are conducted by way of random-sampling methods.

What a trial balance does not tell, most of all, is the frequency by which human errors are committed --the number of errors, whether of omission, misposting, or miscalculation, could indicate whether they are being committed due to lack of knowledge or out of carelessness or, at worst, to perpetuate fraud.

Reference Materials and Image Credit Section

Reference Materials:

- Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso. Accounting tools for business decision making , 3rd edition. (John Wiley & Sons, 2009). The trial balance (page 129) - from the Google Books website, also available at Amazon.

Image Credits: