No one can escape the numbers. The finished goods inventory formula is used to calculate the value of finished goods available for sale in inventory. This amount is then recorded on the company’s balance sheet as an asset.

What Are Finished Goods?

“Finished Goods” is a term most associated with manufacturing companies . Manufacturers transform raw materials into new products. They then sell those products directly to consumers or to wholesale and retail customers. Most of the time we think of larger companies as manufacturers. The truth is, any small craftsman is, in theory, a manufacturer of goods. For example, a person who makes necklaces has an inventory of raw materials and performs direct labor in order to create those necklaces. That brings us to the nitty gritty. Before diving in and learning how to calculate ending finished goods inventory, it’s important to understand a few terms:

- Raw Materials - Finished products are not created from thin air. It takes materials like nails, fabric, paint, wood, silicon, and so on. These are raw materials that are used to create products.

- Work-In-Progress - Have you ever started a project that you were unable to complete by the end of the day? Well, that is exactly what the work-in-progress category represents. It exists to depict, in dollars, the number of units that have begun to move through the production line but are not yet complete.

- Finished Goods - The finished product. For example, a finished product is a computer, a desk, a keyboard, a pie. You get the picture. Finished goods represent the amount of finished product sitting in inventory that is now available for sale to customers.

The Finished Goods Inventory Formula

The simple formula for calculating finished goods inventory is:

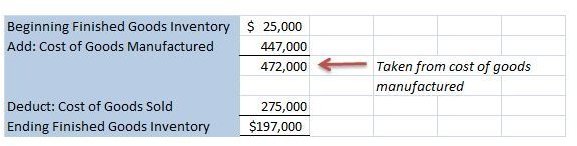

Beginning Finished Goods Inventory + Cost of Goods Manufactured - Cost of Goods Sold = The Ending

Finished Goods Inventory Amount.

But what do the numbers in the formula mean?

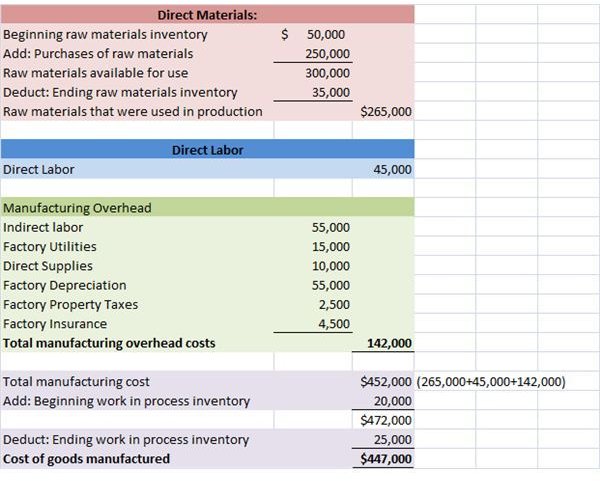

The beginning finished goods inventory is found on the balance sheet. It is the prior period’s ending finished goods amount. Add to that amount the cost of goods manufactured to come up with the total goods available for sale. Deduct the cost of goods sold and there you have it: the ending finished goods inventory. Sounds simple right? Well there is only one hitch in our get-along. You guessed it: how do we calculate cost of goods manufactured? The numbers used in the following example are fictional. There only purpose is to illustrate the cost of goods manufactured calculation:

Manufacturing companies must understand the amount of finished goods they have available for sale. It is an import factor in determining profitability and knowing what the inventory levels are. Tracking inventory is also an important step in deterring possible theft within the company by implementing control systems. These types of control systems are required by the Sarbanes-Oxley Act , a topic for another day. As you can see in the examples shown above, several concepts play into learning how to calculate ending finished goods inventory, such as the cost of goods sold formula.

Credits:

Photo courtesy of TheTruthAbout

Cost of Goods Manufactured Schedule courtesy of Alice Rovney

Finished Goods Inventory Calculation photo courtesy of Alice Rovney