Every business that sells goods should have a method for valuing inventory in place. Two forms of business inventory valuation are the periodic inventory system and the perpetual inventory system. A decent understanding of both is critical to choosing the right one.

An Overview of Periodic and Perpetual Inventory Systems

Inventory is typically the largest current asset on the balance sheet of the merchandising (retail) and manufacturing businesses. It stands to reason that managing that inventory is vital to success. There are two basic yet very important reasons for understanding inventory valuation: control and accurate record keeping.

When a business is exercising control over its inventory, that means it knows when to restock, has an understanding of what sells and what doesn’t, and gains greater command over reducing theft. Accurate record keeping involves reflecting, to the best degree, the physical on-hand inventory, the costs involved to sell that inventory, and actual sales. Periodic and perpetual inventory systems are the methods that management and accountants use in order to meet these objectives. However, only one system is ever in place at a time, unless a gradual shift from one to the other is occurring.

Periodic Inventory System

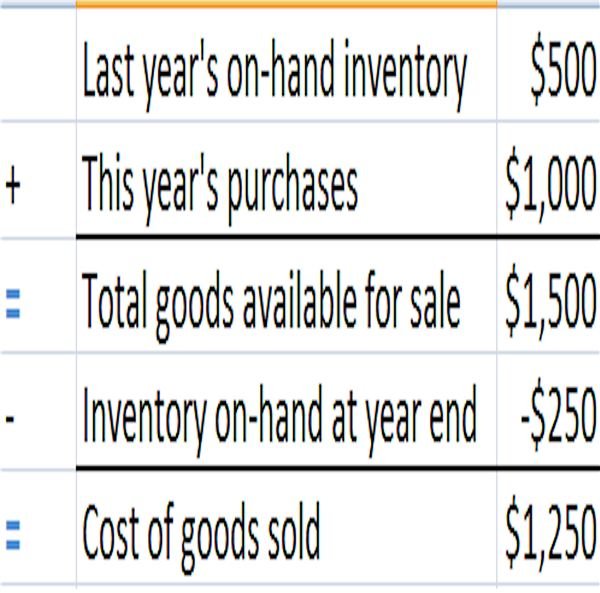

A periodic inventory system was most popular before the introduction of technology to the accounting process. Just as the name implies, physical inventory counts and updates to the accounting records are done periodically. Most companies use an annual basis. For example, at year end managers will begin the process of physically counting the inventory on hand. Purchases that took place throughout the year are added to last year’s ending inventory on the balance sheet to give the total amount of goods available for sale. The amount of on-hand inventory recorded from the physical count is then deducted from that total. The result is the cost of goods sold .

PROS

- The periodic system is easy to implement.

- It’s cheaper to implement the periodic inventory system.

CONS

- The accounting records are modified at the end of the year to reflect the physical inventory count, which leads to greater inaccuracy.

- Taking physical counts of inventory is labor intensive and usually must occur during off hours.

- Exercising control over inventory is more difficult. In other words, it is harder to gauge the level of theft.

Example of Periodic Inventory Calculation

Perpetual Inventory System

The perpetual inventory system is most prevalent today. This process, as the name suggests, keeps an ongoing account of purchases, sales, and losses. Inventory is scanned when it arrives using a scanner that reads a bar code affixed to the item. The dollar value of the inventory is added directly to the inventory account in the software. Likewise, when a sale is made, the item is scanned at the cash register. The value of that item is deducted from the inventory account and added to the cost of goods sold account in the software. Accounting records are continually kept up to date.

PROS

- Inventory values recorded on the balance sheet are more accurate.

- Cost of Goods Sold values recorded on the balance sheet are more accurate.

- Managers have a greater understanding of when to order new stock, including what items sell and what items don’t sell.

CONS

- Implementing a perpetual inventory system costs more money. Purchases such as point-of-sale systems, bar-code scanners, labels, and label printers are necessary.

- Time to train staff on equipment usage and report features is a factor.

- Technology is always changing and this creates a need to update the system periodically.

Image Credit: sxc.hu, Candy Racks, by K Man .