As an owner of more than one business, I often find myself creating a contra account between payables and receivables. The reason? My dealership often utilizes the services of my body shop and vice versa but no real money changes hands. Here’s how a contra account such as this works.

What Is a Contra Account?

Basically, contra accounts in financial accounting can be any two accounts that offset one another. While these accounts work against one another, and often show up in balance sheet accounts, they don’t follow the same rules as double entry bookkeeping entries , and in effect, are utilized to balance books.

For example, an asset may also be a liability, especially if the business owner and customer are one and the same.

Contra Accounts for A/R and A/P

As I mentioned previously, because I am the owner of more than one business, I often utilize the services of one business that should be paid by the other business. For example, at my Ford dealership, if a new or used car is damaged, I send the damaged vehicle to my independent body shop that repairs the vehicle and returns it to the dealership.

Because I own both businesses, I find creating a contra account between payables and receivables often works best.

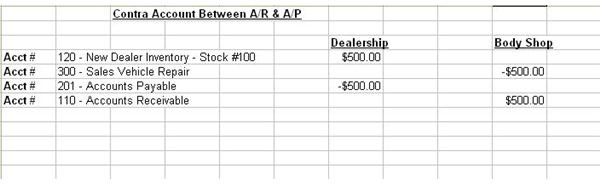

Here is an example of how I would record an entry in the scenario above (click on screenshot to enlarge):

In this situation, the 4 accounts are affected:

- New Dealer Inventory – I must debit $500 to increase the cost of stock #100.

- Sales Vehicle Repair – In this body shop account, I must credit the sale for the repair (remember in financial accounting that sales are always a credit and cost of sales are a debit to determine gross profits).

- Accounts Payable – The dealership now has a payable to the body shop of $500.

- Accounts Receivable – The body shop now has a receivable due from the dealership of $500.

At the end of any given accounting period, say at month end, by offsetting these accounts, even though no money traded hands, the accounts are still offset. But what if it were a little more involved and the body shop and dealership both utilized each other’s services?

Two Company Contra Accounts

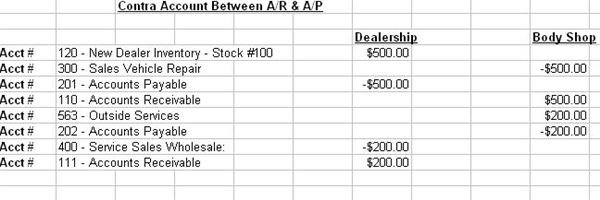

In the below screenshot, now we have journal entries for the dealership performing services for the body shop:

- Outside Services – The body shop needs to have the dealership repair an engine for $200.

- Accounts Payable – The body shop now owes the dealership $200 for an engine repair.

- Service Sales Wholesale – The dealership has a sales revenue of $200 for the engine repair.

- Accounts Receivable – The dealership has an accounts receivable of $200 from the body shop for the engine repair.

Creating contra accounts for both of my companies is often frowned upon by my accountant, but it’s not illegal and helps to keep my books balanced by offsetting the appropriate contra accounts. If I were to seek out an investor in my business or a bank loan for one or both companies, the question of why there are outstanding receivables and payables may be a concern, but are usually accepted.

Pros and Cons of A/R & A/P Contra Accounts

In the accounting scenarios above, by creating a contra account between payables and receivables, both of my businesses show an existing asset and a liability. While my bookkeepers at both businesses may send out Accounts Payable statements each month to one another, it’s really up to me whether I want to actually exchange cash or allow the debits and credits to offset themselves. Because both of my companies have equal amounts due and owed, there really is no benefit as far as cash received. What is not included in the equation is the cost of the sale, which turns into an expense for each company that will never be recovered unless cash exchanges hands.

On the positive side, you can also create a contra account for payables and receivables in a bartering situation.

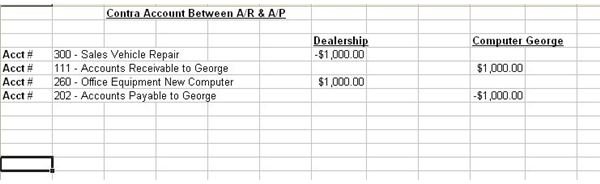

For example, say my IT guy George wants to have his truck’s transmission repaired but he doesn’t have the cash of $1,000 needed to pay for the repair. On my side, I need a new computer, but I also don’t want to spend needed capital on a purchase:

In the above screenshot, while I’m fixing George’s vehicle and he’s giving me a new computer, I have both a receivable and a payable that offset one another, even if no cash was exchanged. In this very simple example, at accounting month or year end, my books will still balance. Creating a contra account for payables and receivables in a bartering situation is advantageous to both parties who have something to offer, but no real cash. These transactions, however, must appear on the books because I now own a piece of equipment that is an asset and will depreciate . By crediting the accounts payable and debiting the accounts receivable for Computer George, they offset each other and will not make my books out of balance. Again, this simple example does not allow for cost of sales for educational purposes.

Using contra accounts for payables and receivables can be a good thing in a bartering situation or a hindrance if you own more than one company that both utilize one another’s services but receive no real cash because both your accounts payable and receivables continue to grow and in some situations may have to be explained to a lender.

Screenshots: Created by and courtesy of author.