A review of activity based costing, its advantages and disadvantages, suggests that while this accounting system has contributed to the transformation of many organizations, it is not widely used today.

What Is Activity Based Costing?

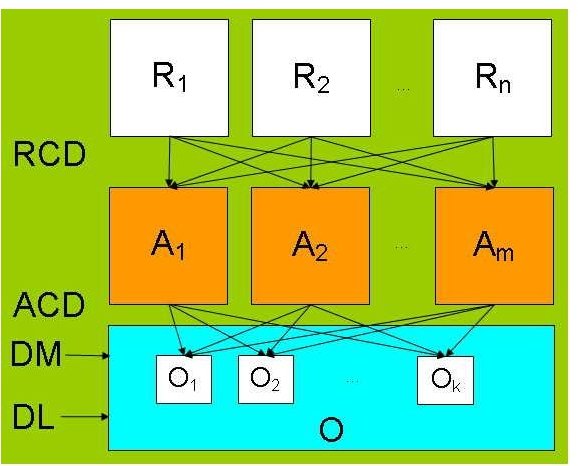

Activity based costing (ABC) is a managerial accounting system that estimates the cost of products and services by assigning overhead costs to direct costs. This costing method assigns the cost of each activity in an organization to all products and services according to the actual consumption of the activity resource by the product or service. This is a marked departure from the practice of sharing overheads costs equally or overheads becoming part of the overall profit-loss estimate instead of component product pricing.

The process of ABC entails the following steps:

- Analysis of activities

- Cost data gathering

- Tracing of costs to activities

- Establishment of output metrics

- Cost analysis.

Image Credit: Wikimedia Commons

Advantages

The major advantage of activity based costing is the ability to estimate the cost of individual products and services precisely. By transferring overhead costs to individual units of products or services, ABC helps identify inefficient or non-profitable products or activities that eat into the profitability of efficient processes or highly profitable products.

The advantages of ABC extend to:

- Making possible equitable and scientific pricing by reducing prices of products that use less activity resources and increase prices of products that consume more of the firm’s activity resources.

- Helping organizations provide value added services or “top-ups” to existing products on actual cost incurred basis.

- Eliminating unprofitable items from the product line, thereby increasing profitability without increasing prices, a valuable option in recessionary times.

- Eliminating the cost of maintaining or running non-remunerative activities, increasing overall profitability.

- Allowing allocation of resources to profitable items or items that use less resources.

- Ensuring compatibility with performance management scorecards by revealing per person contribution to the product cost, and hence, profits.

- Exposing waste and inefficiency that contributes to boosting productivity.

- Identifying and eliminating non-value adding activities, or activities that do not contribute to the final value of the product or process. Examples of non-value adding activities include needless inspections and duplicate processes.

- Providing quantifiable figures for planning and estimates.

ABC mirrors the functioning of an organization and contributes to strategic decision-making processes. It identifies the relation of the product within the business activity and the resources it requires.

- ABC identifies activities that consume too much of the organization’s time or resources, or that contribute little to profitability. This helps in deciding on whether to outsource such processes or whether to implement processes improvement methodologies.

- ABC highlights non-remunerative distribution channels allowing the management to adopt alternative marketing strategies or close down the channel for a more profitable one.

- ABC exposes wastes in the process and integrates well with overall quality management initiatives such as Six Sigma, Total Quality Management , and Kaizen.

Disadvantages and Limitations

The major disadvantage of activity based costing is that although activity based costing is a scientific approach, the method of implementation is complex, time consuming, and costly. The process of data collection and data entry requires substantial resources, and remains costly to maintain.

ABC reports do not conform to generally accepted accounting principles (GAAP) , and as such, firms following ABC need to maintain two cost systems and accounting books, one for internal use and another for external reports, filings, and statutory compliance. This is a cumbersome duplication of efforts.

A primary disadvantage of ABC is that it is not possible to divide some overhead costs such as the chief executive’s salary on a per-product usage basis. Similarly, employees rarely devote 100% of their working hours to productive activities, and not all productive activities add value to the product or process of the firm. For instance, the ABC method fails to account for the time employee takes part in a first aid awareness campaign, leading to substantial ‘cost leaks.’ There is no meaningful way to assign such ‘business sustaining’ costs to products on a proportionate basis, and products and services share such costs equally.

Finally, too much attention to detail and control might obscure the bigger picture or make the firm lose sight of strategic objectives in a quest for small savings, making the firm “penny wise and pound foolish.” For instance, ABC might identify one distribution channel as non-remunerative, or an inspection as non-value adding. Such channeling or processes might be non-profitable, but placed in the first place to achieve some other strategic objectives.

Image Credit: Wikimedia Commons

Summary

A review of activity based costing advantages and disadvantages suggests that although ABC has many uses and has helped transform many firms, the development of lean accounting methods such as Balanced Scorecards and Economic Value Added (EVA) and the like, that focus on eliminating cost allocations and allow thorough accounting, control, and measurement systems without the complex and costly methods of ABC, has made activity based costing obsolete.

ABC however, still has many backers, most notably the US Marine Corps and some business-intelligence software applications.Robert S Kaplan who first promulgated activity based costing in the 1980s has recently promulgated a time-driven ABC that overcomes much of the drawbacks of traditional ABC.

Reference

Kaplan, Robert, S, & Anderson, Steven, R. Rethinking Activity Based Costing. Harvard Business School. Retrieved from https://hbswk.hbs.edu/item/4587.html