What do you do if the Total Debit and Total Credit columns on your trial balance don’t equal? Learn some tips on how to detect posting errors before proceeding with the post-closing procedures of the accounting process.

The Importance of Monitoring the Equality of Debit and Credit Balances

After every completion of posting the monthly accounting transactions, it’s important to prepare an unadjusted trial balance for the general ledger accounts. Their respective ending balances should be in accordance with their normal balances under the debit or credit columns. Any resulting difference between the total debits and total credits can be easily traced by simply reviewing the latest transactions posted. This is a way of maintaining a balanced general ledger before posting the next batch of accounting transactions.

Verifying the equality of debits and credits is quite important, especially when we reach the final month of an entire accounting cycle. At that point in time, the figures carried as general ledger balances will be the basis for the preparation of standard financial statement reports.

Still, certain adjusting and closing entries are required as parts of the closing procedures, to arrive at the true figures that the account balances should have. Thus, the initial step is to prepare a worksheet, to test if the GL’s debit and credit balances are equal before the post-adjusting and post closing entries are made.

Performing the Initial Steps for the Post Closing Entries at Year-End

View our sample post-closing worksheet below, which shows that the total of the Debit column is equal to the total of the Credit column but still unadjusted as far as post-closing entries are concerned. We can therefore proceed with the standard adjusting entries and closing entries, in order to come up with account balances considered as usable for financial statement reporting. For a downloadable copy of this sample, you can check out Bright Hub’s Media Gallery for Sample Unadjusted Trial Balance Worksheet.

However there is always the likely possibility that a difference may arise between the Total Debit and Total Credit columns. It is important therefore, that the errors causing the imbalance should be detected before proceeding to the final steps of the accounting cycle for the year.

How to Detect Errors if the Total Debits and Total Credits are Not Equal?

You will have to review the latest transactions you posted after you have double checked the total for each column; this is still advisable even if you are using an Excel worksheet and its auto sum function . Here are some tips to consider when in the process of tracing back your current month’s transactions:

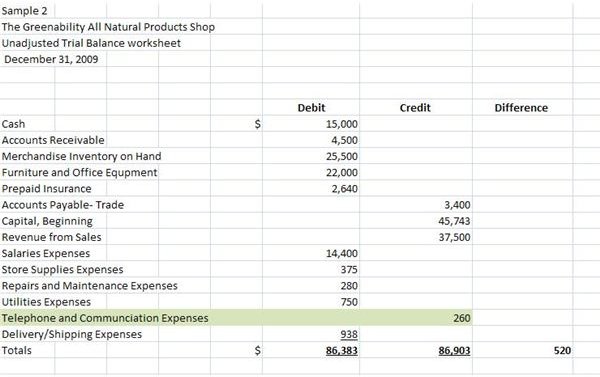

If the difference between the debit and the credit totals is divisible by 2, check for an account balance equal to the halved amount of the difference. To illustrate, please click on the image on your right in order to have a larger view of a sample imbalanced post-closing worksheet. In viewing, please note the following:

-

We can easily recognize that $520 difference as an amount divisible by 2 and its resulting half is $260.

Advertisement -

Look for the figure $260 in the column that has a greater total, which in this case is the Total Credits.

-

Note that the $260 balance for the Telephone and Communication Expenses was placed under the credit column instead of the debit column, which is the normal balance of the account. Hence, in placing the $260 under the appropriate column, the worksheet will now have the same debit and credit totals.

Advertisement

A mere physical transfer of the figure to its proper location will suffice and will not require any adjusting entires.

Continue to the next page for more examples of detecting errors that cause an imbalance between debit and credit totals.

More Examples on How to Detect Errors that Cause Imbalances

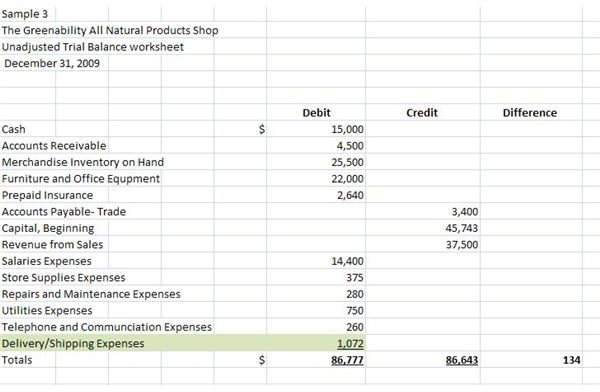

The same technique holds true if you are trying to locate any inaccurately posted transactions for the month. A transaction may have been credited instead of debited and vice versa. Kindly click on another sample of a trial balance that has to be adjusted before proceeding with the post-closing and post-adjusting entries . The sample worksheet reflects a difference of $134 between the Total Debits as against the Total Credits.

-

The difference of $ 134 is divisible by 2 since the figure ends with an even number; hence, the halved amount would be $ 67.

-

Examine the figures included under the column with the larger total; in this case it would be the Debit column. However, this column does not have any account balance that matches the halved amount of $67.

Advertisement -

You will now have to review your transaction postings for the month by examining your journal vouchers or the source documents you used for posting the general ledger entries. Keep in mind that you will be on the look out for a journal entry voucher for $67 and not the $134 difference.

-

In the course of your checking, you noted a refund of $67 for a delivery cost, which should have reduced the amount of your Delivery/ Shipment expenses. However, it was erroneously posted as a debit to this account. The journal voucher indicated that a credit entry to Delivery/Shipment Expenses should have been made, yet you automatically posted the amount as a debit perhaps, thinking that it is a normal expense.

Advertisement -

This kind of error will not require an adjusting entry since the journal voucher contained a correct entry. By merely posting the amount to the credit side and drawing a line over the incorrect post on the debit side will suffice. It follows that you should also re-calculate and indicate the correct account balance.

- The image on your right is a snapshot example of the general ledger page for this particular entry. As a rule, posting errors in general ledger entries are usually corrected by drawing a line over the figures to be replaced. This is to provide transparency for any error corrections made on the general ledger pages.

How to Detect Transposition Errors

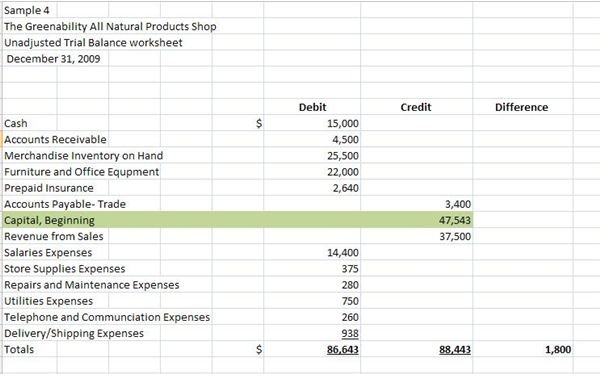

Differences may also arise from mistakes known as transposition errors. A transposition error is one wherein two adjacent numbers of a certain amount were erroneously transposed upon posting. A transposition error can be determined if the resulting difference is divisible by 9. Please click on the image on your right to have a larger view of our fourth sample of post-closing worksheet and you will note that the difference of $ 1,800 is divisible by the number 9.

-

Your review of the balances appearing on the worksheet, revealed that you erroneously indicated the amount of $ 47,543 instead of $ 45,743 for the Capital account. By simply correcting the figure reflected on the worksheet, you will arrive at the correct debit and credit totals.

-

Nonetheless, If the $ 1,800 difference remains undetected, the procedure will again require retracing the postings made on the general ledger book and comparing them to the source document. Again, the error can be corrected by simply posting the right amount under the appropriate column, and by drawing a line over the erroneous post.

Advertisement

Not all errors however can be detected by proving the equality of the GL’s debit and credit totals. Some errors will be revealed at a later date, usually by the internal auditor , who randomly scrutinizes the accounting entries you made. These types of errors often involve misclassification of accounts or errors in analyzing the transaction. These are the errors that require appropriate accounting entries based on the recommendations of the examining auditor.

Nevertheless, once you have proven that the debit and credit totals of your unadjusted trial balance are equal, you can now proceed with your adjusting and closing entries as part of your year end procedure. Ensuring a balanced general ledger gives assurance that the figures reflected in the financial statement reports, are fair representations of the business entity’s financial records. .

Reference:

Explanations and sample post-closing worksheets were created by the author.

This post is part of the series: Understanding Balance Sheets

Learn tips and details related to understanding, creating and reconciling balance sheets. Also, find several examples and free templates you can download for your own personal or business use.