In financial accounting every journal entry made in the general ledger flows to the trial balance. What is a trial balance sheet and why is it so important? Jean Scheid offers an in-depth look into why this financial accounting statement is so important and key to every financial statement prepared.

What is a Trial Balance?

Journal entries, debits and credits, profit and loss statements, balance sheets—where does it all end? To be honest, everything either flows into or comes out of the trial balance sheet.

Think of the components of the trial balance sheet as the heart of your accounting system. Without this heart, your accounting system would be no accounting system at all. Sure you can get a quick snapshot of your business from your balance sheet and a look at your income and expense statement will tell you if you made a profit, but in order to be sure those summary numbers on these reports are accurate, the trial balance must be accurate first.

Taking a Closer Look

When I started in business years ago, I never realized how important the trial balance was. Not only does it show everything that occurs financially in your business, if you don’t keep a close eye on it, especially during month or year-end times, your accounting will be inaccurate and hard to fix.

At the end of my first year in business when my accountant asked for my trial balance, I think I sat there staring at her thinking, “What’s that?” If your business is not an all-cash business and you utilize an accounting software system, however, creating a trial balance is easier than you think.

First, read the article a Guide to Preparing a Trial Balance and in the article you’ll find a link to a trial balance template. Now let’s talk about its primary components.

Components

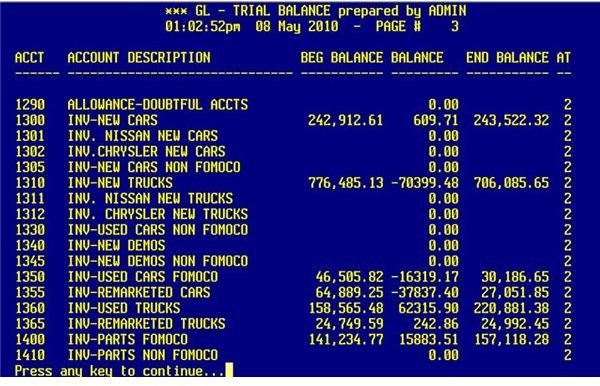

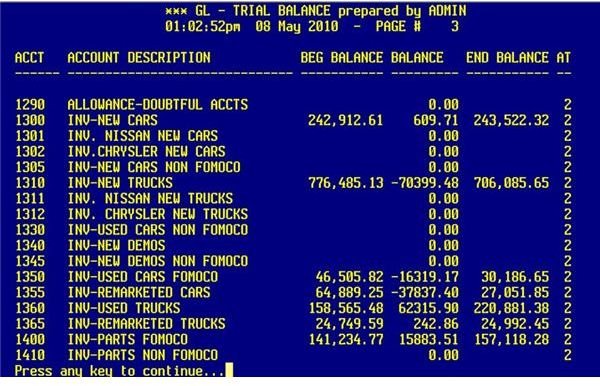

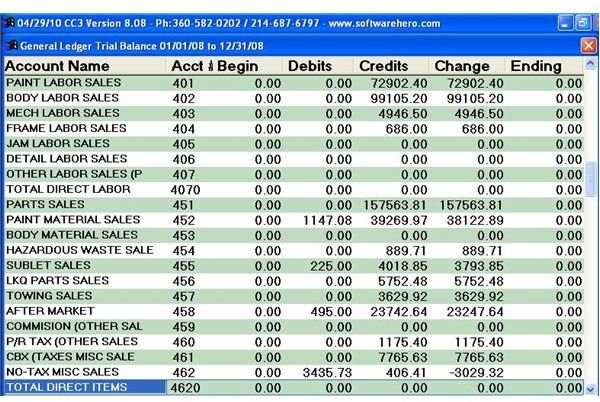

The trial balance contains every transaction made into general ledgers as journal entries in every account that relates to your business. In the example to the right (click to enlarge), you will see a portion of a trial balance for an auto dealership.

Every time a journal entry is made to an asset account, liabilities, sales, cost of sales, or expenses, that journal entry is pulled to the trial balance. In the example to the right, look at account #1310 (Inventory-New Trucks). Here we see the following numbers on the trial balance:

Beginning Balance / Balance / Ending Balance

$776,485.13 / $-70,399.48 / $706,085.65

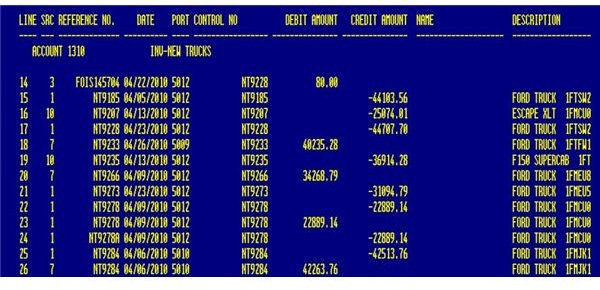

But how did those numbers get there? In the next image to the right, is the account detail for New Truck Inventory that pulls to the trial balance from the

general ledger journal entries. In this account for New Truck Inventory, you see the detail including the date the journal entry was made, debits and credits, and a description.

A debit to this account means that New Truck Inventory was coming in and a credit means New Truck Inventory was sold or going out. Now look at the next image to the right to view the closing balance detail for account 1310, New Truck Inventory.

What you see here are debits of $447,620.67 and credits of ($518,020.15). These numbers represent all the journal entries made to the New Truck Inventory account for the month.

So, remember those trial balance numbers above?

Beginning Balance / Balance / Ending Balance

$776,485.13 / $-70,399.48 / $706,085.65

These numbers that pulled to the trial balance are based off journal entry detail in the New Truck Inventory account:

- Beginning Balance - $776,485.13

- Debits - $447,620.67

- Credits – ($518,020.15)

- Debits Minus Credits – ($70,399.48)

- Ending Balance - $706,085.65

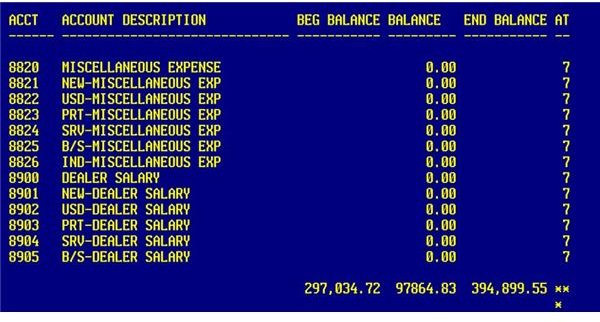

Only the summary numbers (not the debits and credits) show in the trial balance. At the end of the month, as seen in the final image to the right, the debits and credit must equal each other from the journal entries made in the general ledger. In this final image, we can see that we have:

- Beginning Balance - $297,034.72

- Balance - $97,864.83 (This number represents the total of all the debits and credit for the month).

- Ending Balance - $394.899.55

If, for example, the balance number of $97,864.83 wasn’t correct because the debits and credits from the accounting month journal entries did not equal, our ending balance in the trial balance would be incorrect. From there, investigation into each journal entry detail would need to be reviewed to analyze where the mistake lies.

A trial balance would immediately show this through a final account called, the balance offset account. The number in the balance offset account shows the amount the trial balance is out of balance; it can appear as a positive or negative number.

Repairing the Trial Balance Offset Account

If we did have an outstanding number in a balance offset account, that number would have to be investigated. Often, the error can be easy to identify by reviewing journal entries made for the month, however, sometimes the balance offset can contain more than one incorrect or missed journal entry.

In order to correct the trial balance, a bookkeeper or accounting person must find the balance offset error, make journal entry adjustments, re-run the trial balance which would now be an adjusted trial balance, prior to running the final desired reports: the income and expense (profit or loss) statement, and the balance sheet .

When considering the important components of the trial balance sheet, think of them this way, especially as it relates to the accounting flow cycle:

- Journal Entries in General Ledger – This is where every transaction is recorded

- Journal Entry Detail – This shows the detail of what was recorded in each account

- Trial Balance Summary Totals – These summary totals represent the debits and credits made via journal entries and then pulled to the trial balance.

- Balance Offset Account – If the debits and credits in all the trial balance summary totals do not equal, a number will appear here. If it is zero, you are fine.

- Find Balance Offset Errors – Research any numbers that appear in this account and make the appropriate adjusted journal entries.

- Print Adjusted Trial Balance – Re-run your adjusted trial balance to ensure the debits and credits equal and your balance offset account is zero.

- Print Income & Expense Statement – You can now print an accurate income and expense or profit and loss statement , which contain summary numbers pulled from the trial balance.

- Print Balance Sheet – The summary numbers in your balance sheet accounts will be accurate because the trial balance is equal.

If your business utilizes accounting software such as Quickbooks, Quicken or some other accounting software dedicated to your field of business, through the journal entries you make into the general ledger for the month, the trial balance can be created.

Only when journal entries are made inaccurately or missed will it affect the trial balance, or in other words, make the trial balance incorrect. Thus, when debits and credits do not equal for the month, the trial balance will reveal that offsetting number for you to begin your research, correct the trial balance, and print out accurate financial reports for the accounting period.

For some new business owners, even if you have a bookkeeper, it’s a good idea to enroll in some general accounting classes either online or onsite to gain a better knowledge of what the trial balance sheet is and does and how it connects to your other financial statements.

References

The author is a business owner and has experience in preparing and utilizing a trial balance.

All screenshots courtesy of author.

This post is part of the series: Understanding Balance Sheets

Learn tips and details related to understanding, creating and reconciling balance sheets. Also, find several examples and free templates you can download for your own personal or business use.