While some individuals believe the meaning of reconciling an account involves fiddling with numbers and forcing two accounts to add up properly, this is not the case. In fact, it is important that companies and accountants work carefully to properly reconcile accounts for maximum effectiveness.

Account reconciliation involves looking at an account statement and determining whether the balance shown in your records matches the balance shown by the bank’s records. For some, this leads to a headache, especially if accurate records have not been kept. However, this accounting activity is essential for knowing:

- Whether the bank has made an error in computation

- Whether transactions were not completed

- Whether a client’s or customer’s payment was not received

- Whether a check you received bounced

- Your correct current financial situation

- Whether payments you made cleared or not

What Accounts Need Attention?

When running a business, reconciliation is not as simple as simply ensuring your business’s checking account is accurate. Other accounts that must be reconciled on a regular basis include:

- Accounts Receivable

- Accounts Payable

- Investment Accounts

- Other assets including land, buildings, and equipment - you need to take depreciation into account

- Payroll that has accrued

- Vacation and benefits that have accrued

- Taxes

- Loans and other credit/bank notes payable

How to Complete

To begin reconciling an account, you need to be sure you know what’s supposed to be included in the ledger for that account. Once you know what’s supposed to be in the ledger, you need to acquire all of the documents that go with that account. For example, if you are reconciling an accounts receivable ledger, you will want to find all your invoices and contracts. If you are reconciling a business checking account, gather up your receipts and statements.

Once you have your materials, if you haven’t entered the amounts into the appropriate ledgers , you should do so at this time. Be sure to double check each number, as wrong transcription is a common error when it comes time to reconcile your accounts. Enter the numbers from the actual invoices, receipts, or time sheets. You should never rely upon information from your bank account statement when entering information. Why is this the case? If you rely upon this data, you may miss errors that occur as part of human error or billing errors.

Next, you will add up the invoices, receipts, time sheets, etc. separately. Add them twice. Why do this? You should have the same amount both times you add up the amounts. If you don’t, you know you either missed something or keyed something in wrong and you will repeat the procedure a third time to confirm the amount.

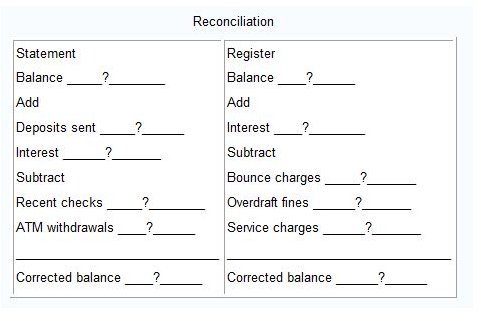

Once you have confirmed the amount, then check your statement against your personal register. Do the two amounts match? Good! You’re lucky. Even if the two amounts match, go through your items one-by-one and check each off as having been reconciled.

What Happens When the Statement Does Not Match the Register?

Every so often, your statement and register will not mesh. This can be for a variety of reasons - one of the most common reasons for this error is that you forgot to record a receipt or deposit. When you go through your items one-by-one, you should find this error. A second common error is a typo - make sure when reconciling that the amounts for each debit and credit match up. A third reason your amounts may differ from one another is that the bank made an error. If you have double-checked your records and you are still coming up with different figures, it is time to call your bank.

Do not adjust any amounts just to match the statement to the register. Even though it is a pain, and can be quite time consuming, take the time to hunt down every last penny, even if it’s only a five-cent difference. It will save you time (and heartache) in the future, and by being in the habit of double-checking everything until it’s reconciled, when there’s a big difference, you’ll know the procedure for tracking down where the error is, and you can be on top of debts, billing errors, and bank errors.

References:

“Account Reconciliation” https://www.fso.arizona.edu/fso/deptman/16/1630reco.html

Reconcilition chart image courtesy of Wikimedia Commons