In learning the difference between accrual basis vs. cash basis accounting, it should be clear that choosing one method over another is not about their pros and cons. Determining net Income should be based on accounting principles and the main guiding tenet is “matching income and expenses."

The Accrual Basis: How It Differs from Cash Basis

Accrual basis vs. cash basis accounting methods are quite confusing, particularly for those who have just started a new business. The accrual method can be considered as a less likely choice if a non-accountant will perform the accounting process. The accrual method is quite complicated because it involves correlated actions of recognizing, amortizing or deferring expenses or income without considering if an actual exchange of cash had taken place.

As opposed to cash basis, wherein the income and expense transactions are included for as long as they cause a decrease or increase in the cash balance. Hence, cash basis is often the popular choice because it is easy and simple. But as far as determining your actual gains or losses are concerned, it is effective only if your business runs on a purely cash basis and does not maintain any merchandise inventory.

As trade and commerce advanced with technological developments, so did the accounting process. The accrual method is a system that was established in order to recognize the expenses incurred in relation to the income it generated. Income on the other hand, was included if it was actually earned. Businesses who receive advances or prepayments will consider payments received in advance as unearned income booked as liabilities. They will be actually recognized as income until such time that the services or products have been served.

Conversely, businesses that make prepayments for services or products that are yet to be delivered will book their advance payments in an other asset account. They will be recognized as expenses on the actual dates that they inure to or upon actual application of their prepayment. An example of this is an advanced rent deposit paid as a prerequisite for rental agreements. This is illustrated in the comparative examples on how net income is computed using accrual basis vs. cash basis shown on the next page.

Any mismatch between the expenses deducted against the reported income may result to an understatement or overstatement of net income. The Internal Revenue Service (IRS) often frowns upon an understatement of net income because it will appear that it was deliberately done to reduce the tax obligations for the year. On the other hand, investors will not consider the business as a worthy investment prospect since a losing-entity is hardly a good investment choice.

If your income is overstated as a result of using the inappropriate accounting method to match income and expenses, it will also put you at the losing end. Your tax obligations will be bloated and you might be paying more than what is due. On the part of the investors, once they get to see the true picture of your business and perceive that the income reported is hardly a reflection of your company’s performance.

In a separate article entitled Top Ten Accounting Scandals that Changed the Business World , readers will learn how accounting irregularities led to the downfall of top companies who were charged with fraud, for presenting investors with misleading financial reports about their business conditions.

To illustrate the effects of accrual basis vs. cash basis pertaining to how expenses that were paid in advance or income that was received in advance are treated, please proceed to the second page to view comparative examples.

Accrual Basis vs. Cash Basis Accounting: Comparative Examples of Computing Net Income

There are other types of transactions that may be affected by accrual basis or cash basis accounting. To illustrate, here are some examples of other business expenses and some deviations in the manner by which they were incurred or paid. This is to assume that the business has just started .

Given conditions:

- Merchandise purchased from January to December-$60,000 (Inventory of the unsold stocks as of December 31 showed that the remaining value of the merchandise still on hand was $25,000)

- Salary Expenses from January to December including bonuses- $ 40,000

- Employer’s Share of Health Benefits- $5,000 (Fully remitted up to November while the December premiums of $455 were paid in the month of January of the succeeding year.)

- Rent Expense from March to November - $5,500 (2-Months rent deposits of $1,000 were included in the rent payments for the year; $500 December rent was actually paid in January of the succeeding year.

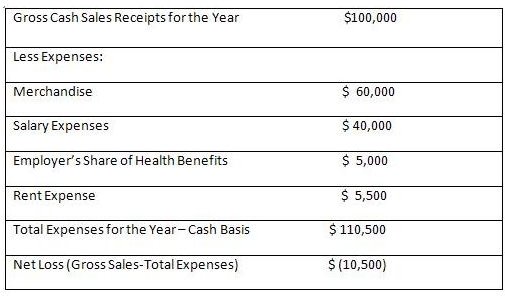

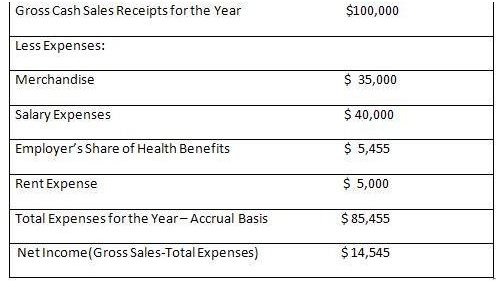

- Gross Cash Sales Receipts for the Year - $100,000

Please click on the image to have a larger view of the illustration.

Net Income Computed on Cash Basis

In using the cash basis to determine net income, all expenses or cash outlays for the year were used as a deduction to the gross sales receipts. This resulted in a net loss of ($ 10,500). If you are to use this computation in your income tax return, the IRS Agent who verifies your tax return will likely serve you with an assessment for unpaid taxes.

Now, let’s find out why and learn the difference if the Net Income was computed on accrual basis.

Net Income if Computed on Accrual Basis

Now you can see that under the accrual method, a net income of $ 14,545 will be reported to the IRS for the year’s income tax return. You may have the impression that the other expenses were valid; hence, should have been recognized as a deduction. Actually, recognition will only be deferred for the next accounting period when the expenses will be used as deduction to the next round of income generated.

There are cases during year-end operations when some expenses are paid in January of the succeeding year. In cash basis, these expenses are often overlooked because they were disbursed and recorded in the new year’s transactions. This is why under the accrual method, they are already recognized as expenses by setting up a liability account to complete the dual accounting entry.

Please proceed to the next page for further explanations about the accrual basis vs. cash basis accounting valuations..

Explanations on Valuations Used in Accrual Basis

Below are further explanations on how the given expenses were treated to determine the net income using accrual basis. Click on the accrual image to the right to enlarge it for our example.

Merchandise - This item is not treated as an outright expense since not all of the merchandise purchased was sold. A year end inventory of the stocks showed that $25,000 worth of stocks were still on hand. Hence, this portion did not generate any income but only created an asset account, which is the merchandise inventory on hand. The cash disbursement was recognized in the books in the following manner:

- Merchandise as Cost of Goods Sold - $35,000. This part will be taken up as expense and summarized in the profit and loss statement. It was used to arrive at the net income account.

- Merchandise as Inventory on Hand - $25,000. This will be taken up as an asset account-merchandise inventory-on hand and will be carried over as the beginning balance of the balance sheet statement . For the next year end, they will be recognized as part of the expenses by following the FIFO (First-In, First-Out) method of assigning costs for stock inventory.

- Cash used to pay for the entire purchases - ($60,000). The entire amount will still be treated as a reduction of cash balance for the year.

Employer’s Share of Health Benefits - $455. Although this year-end expense was paid on the first month of the succeeding year, this is still included as expense for the year that recently ended. Take note that the salaries it inured to were incurred for the previous year, thus it should be matched against the income for that year.

Rent Expense - The same is true with the $ 500 December rent payment, even if it was actually disbursed on the following month**.** The rent was for the inclusive period of the reported income hence, the actual date when the cash was decreased by the said payment will not be the basis. In addition, recognition of the $1,000 advance deposit as an expense will also be deferred until the time that they will actually be applied as rent for the business operation. In the meantime, the advance deposit will be treated as an asset account named as an other asset account-prepaid rent or advances and deposits.

The illustrations above show that there are no pros and cons as far as accrual basis vs. cash basis is concerned. It is a matter of applying the appropriate method based on the principles of “matching revenue and expenses" applied on a consistent basis."

Reference and Image Credits:

- Case study and explanations were created by the author.

- Screen-shots of sample financial statements were created by the author

- WM Expenses Pie 2006 by Tlogmer at Wikimedia Commons https://commons.wikimedia.org/wiki/File:WM-expenses-pie-2006.png