Why does a balance sheet have to balance and what accounts must you reconcile to complete the process? Here, Jean Scheid offers a sample of balance sheet account reconciliation and explains why it’s necessary.

What Is the Balance Sheet?

A balance sheet is often referred to as a snapshot of a company’s financial status at any moment in time. The balance sheet lists assets, liabilities, owner’s equity, and net profit in a summary format. These summary numbers must come from somewhere, however, and they must balance.

You can download and print the balance sheet example we’ve provided in our Media Gallery for the ABC Company dated December 31, 2010 . This will enable you to see the summary numbers for items like cash, accounts receivable, inventory, accounts payable, loans payable, and other summary accounts.

The numbers in these summary accounts are pulled from journals, schedules, and the general journal and then to the trial balance. If the trial balance is not equal in debits and credits and doesn’t balance, the balance sheet will be incorrect.

Analyzing Balance Sheet Reconciliation

Your first comment may be when looking at the ABC Company balance sheet, “Can’t you just plug any old number in there and because it automatically calculates, won’t it still balance?” Well, you could, however, this would show balance sheet limitations and show false or created summary totals. Let’s look at some examples.

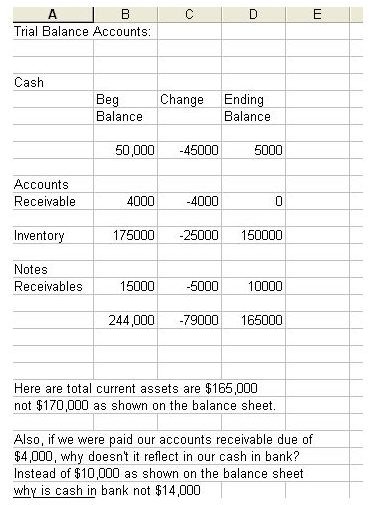

Our cash on the ABC balance sheet is $10,000. That $10,000 comes from the cash in bank ledger and each month the bank account is reconciled to ensure it’s accurate. The same is true for every asset account to determine the total current assets on the trial balance. In our example, the total current assets are $170,000.

Click on the Trial Balance Image to the left to see what happens in the trial balance. Keep in mind that every number pulled to the trial balance comes from the general ledger, schedules, or journals. The trial balance will show a beginning balance, any changes in the form of debits or credits , and the ending balance. In the trial balance example, although our beginning balance and change columns do equal, the ending balances do not equal what is on our ABC balance sheet.

If you don’t reconcile trial balance accounts accurately, what it will do when pulling summary totals to the balance sheet is offer an incorrect net profit. Here, the net profit decreases from $53,000 to $48,000 and that’s incorrect. Try plugging the correct bank balance into the sample ABC balance sheet and see what happens.

Finally, it’s important to note that not all, but some balance sheets contain summary accounts such as “other assets” or “other liabilities.” These accounts are often utilized by accounting software programs to force the balance sheet to balance.

Trial Balance Numbers

The world of financial accounting can be difficult to understand. A balance sheet like the one in our example in a MS Excel format, will balance no matter what numbers you apply but random numbers will result in lower net profits or negative equity. This is where the trial balance comes in and the numbers on the trial balance come from the general ledger or journal, specific journals, and schedules.

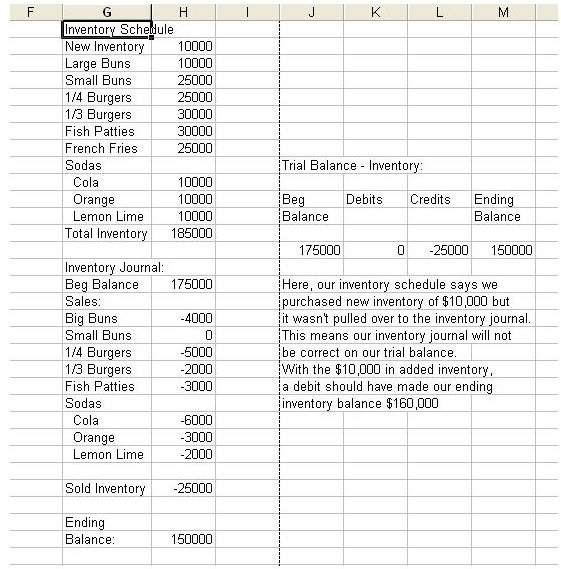

Before you give up on financial accounting, the need to offer the sample balance sheet reconciliation is essentially a huge step in understanding where those summary totals come from. Let’s take inventory for example. Our balance sheet shows a summary total of $150,000 in current inventory. Let’s assume we had a beginning balance of $175,000 with $25,000 inventory out equals our ending balance of $150,000. But how did this end up on the balance sheet and trial balance and what if it wasn’t correctly recorded?

Click on the Sample Inventory Schedule to the left. It shows our beginning balance of inventory at $175,000 and inventory out of $25,000 so our balance sheet summary total is $150,000. But wait! Somewhere, the new inventory coming in of $10,000 was not recorded in the inventory schedule or journal . If it wasn’t recorded, it doesn’t pull to the trial balance meaning even though the company bought new inventory of $10,000, the current inventory summary total of $150,00 is off by $10,000; it should be $160,000.

On the balance sheet, because the inventory account was not reconciled correctly, instead of a $63,000 profit, we have only a $53,000 profit.

Please click on Page 2 to find out why not all balance sheets are equal and why investigation is key in balance sheet reconciliation.

Not All Balance Sheets Are Equal

Just to throw another element in the pot, it’s important to note that not all balance sheets are equal. Even with our sample of balance sheet account reconciliation in this article, your balance sheet could be totally different. Balance sheet summary accounts vary depending upon the type of business you have, the size of the business, and if the business is a franchised business.

For example, in smaller companies, the accounts receivable summary account is not looked at as a strong asset because it’s money waiting to be obtained. If a company has sales revenues of $150,000 annually and their accounts receivable shows $10,000 due, it’s likely that some of those receivables are non-collectible. Upon inspection, a analyst may find that of that $10,000 due, much of the total would be comprised of accounts receivables that are over 120 days past due.

On the other hand, big businesses that have millions in inventory sales and high accounts receivable numbers can be looked at as a good thing. Most likely these larger businesses do indeed have contracts with suppliers they sell to and if these accounts go unpaid the legal contract helps to ensure payment in the future, hence real cash.

The franchised business is a tricky business, especially when it comes to rules of the franchisor on how summary accounts are reported. Unlike a smaller company where the accounts receivables may be looked at as a negative until obtained, franchisors look at this account as an absolute asset. Why? In franchised businesses, upon franchisor audits, all assets are determined, less the liabilities to determine working capital. Often, franchisors set limits on how high or low working capital must be for the fran

Inspection & Knowledge Are Key

Understanding the importance of balance sheet account reconciliation is prudent in any size company. No company should allow those summary account totals to be comprised of erroneous or out-of-date information. If you do, a simple review of your general ledger, journals, schedules and the trial balance would show any reviewer that your balance sheet summary totals are over or understated.

I’ll go further and give you an example. When I purchased an auto dealership franchise, the seller listed $25,000 in an “other receivables” account. To me, I as thrilled to inherit this amount, however, upon closer inspection, these were dollars that didn’t actually exist. How did they get there? The owner of the dealership received $500 for every vehicle sold from the manufacturer. Not only did this dealer record the $500 as cash in bank (debit) and as a (credit) to his floor plan liability, he also used it to decrease (credit his inventory account and increase (debit) his “other receivables” account. So in fact, the second erroneous journal entry meant the dealer had already received and most likely spent the $25,000 in the increments once received by the manufacturer.

For buyers of an existing business , investigation and financial accounting knowledge is key. A simple balance sheet for a smaller company may be easy to analyze through one general journal or ledger. Larger and more complex balance sheet account reconciliation are compiled from sales and cost journals, inventory schedules that are controlled accounts that must balance, and general journals where miscellaneous journal entries are made. Finally, all of these accounting tools pull to the trial balance which indeed is often the best place to start your investigation when analyzing balance sheet account reconciliation.

The Importance of Balance Sheet Reconciliation

As you can see in our sample balance sheet, if a business does not reconcile every account that pulls to the balance sheet, any sample of balance sheet account reconciliation will be incorrect. Un-reconciled accounts can mean incorrect numbers, over or understated profits. This is true for every summary account on the balance sheet.

To ensure your balance sheet is reconciled correctly, you must understand the importance of not only where those summary totals come from but also how incorrect journal entries can affect that balance sheet snapshot.

This post is part of the series: Understanding Balance Sheets

Learn tips and details related to understanding, creating and reconciling balance sheets. Also, find several examples and free templates you can download for your own personal or business use.