In a competitive financial market, decisions of one party provide clear signals to others. Paying attention to the behavior of others can speak volumes on the expected profitability of a security. Learn all about the types of signals financial markets.

Types of Financial Signals

The Principle of Signaling is a simple yet powerful concept in financial markets. The adage “actions speak louder than words” sums up this principle well. In financial market, decisions to buy and sell securities are public information. A large corporation or investment firm can not sell or buy large quantities of securities without arousing the interest of other investors and the financial news media. In addition, entering new lines of business, abandoning a line of products, announcing dividends and stock splits, etc. all indicate important information to the market.

Actions

Suppose the CEO of a publicly-traded corporation makes an announcement that she is optimistic about the future of the firm and expects a large return on investments in the near future. This news would normally result in an increase of the firm’s stock price. However, imagine if soon after this announcement, the CEO herself sells off the majority of her holdings in the company. How confident would investors feel about paying for shares of the firm’s stock at the new, higher price? The CEO’s action has spoken louder than her words making investors suspicious about the optimistic announcement.

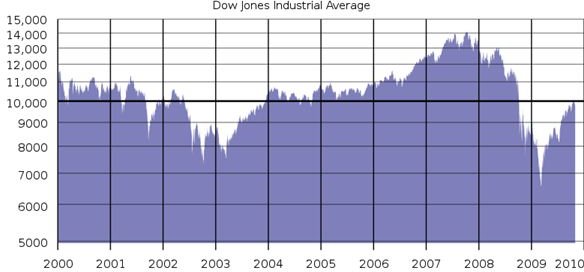

Prices

The automobile tire market suffers from a major marketing problem. Most people who own cars do not know much about what makes a quality tire. Customers must rely on experts to tell them which tires are good quality and which should be avoided. Sometimes the only expert available is the manufacturer itself. One way to convey quality is with price. People generally believe that higher prices correlate with higher quality tires. Smaller competitors in the tire industry have a difficult time establishing themselves as low-price providers because lower prices are perceived to be synonymous with inferior quality. Here, price is a signal that directs behavior in the market.

**

Adverse Selection

One principle indelibly linked to signaling is adverse selection, which occurs when offering something for sale triggers a negative signal. One of the difficulties of selling a used car is the signal that is generated when the car is put up for sale. Questions come up that ask why someone would sell a car that runs well and why the seller is willing to part with a perfectly good car. Simply putting the car up for sale is a negative signal that can dilute a buyer’s willingness to pay the asking price. The buyer wants a lower price partly to mitigate any negative outcomes that may arise after the purchase of the used car.

Following the Crowd

Signaling has its disadvantages. Consider this metaphor: A group of deer are drinking water from a lake in the early hours of the morning. A branch falls from a tree and one deer, perceiving it may be a predator, bolts into the forest. The other deer, seeing this behavior, run into the forest for fear that they may have missed something and want to be safe. This illustrates the bandwagon effect where the simplest and most innocent of events causes a chain reaction of behavior. In investing, signaling is a powerful tool but it can be dangerous to rely on others who have relied on others, etc. for the best actions to take.

Image Credit

Wikimedia Commons: https://commons.wikimedia.org/wiki/File:DJIA _2000s_graph_%28log%29.svg

This post is part of the series: The Competitive Financial Environment

The competitive financial environment is governed by four distinct principles. These principles encompass the idea that attaining value is a matter of competition resulting in winners and losers. The principles outlined here are an overview of this competitive environment.