People go into business because they have an interest in producing a specific product or service. The last thing they want to do is wade their way through all kinds of financial ratios. The liquidity analysis is an important ratio for an owner to know about, and this guide will take you through it.

The Fluidity of Liquidity

Some people feel a great deal of confusion by the complex and confusing glossary of the financial business world, and understanding liquidity analysis is a perfect example. The term actually means just what it sounds like: The liquidity of your finances, meaning your ability to utilize money in a timely fashion to meet financial situations that arise.

Liquidity is different from solvency. A business is considered liquid if its assets are sufficient and are sufficiently convertible to cover liabilities. Liquidity implies that the owner’s fluid ability to convert assets will convince investors or bankers to loan money to the business.

Liquidity problems occur when, for example, the business owner cannot convert assets into cash quickly enough to cover liabilities as needed. However, the fact that he has assets might convince lenders to help him out in given situations. The business’s combination or ratio of assets to liabilities keeps it liquid.

What Information Do Liquidity Ratios Provide?

If it wants to succeed, a business must be able to meet its regular demands as well as any unexpected expenses that come up. Liquidity is determined by dividing current assets by current liabilities. If someone has assets in the amount of $300,000 and liabilities of $100,000, the liquidity ratio will be 3. A ratio of 1.5 or higher is positive.

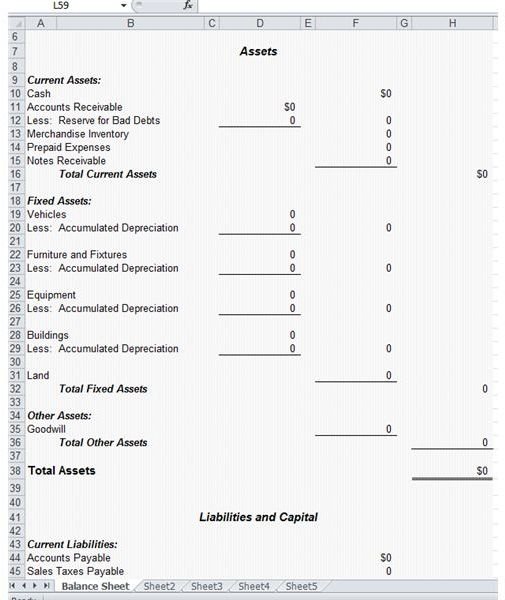

An Example of a Basic Balance Sheet

Where does the business owner get these figures—the total assets and liabilities? They are figures, along with others, found on the balance sheet. Of course, the ratio is a little more complicated than assets divided by liabilities. You’ve got to take your assets and subtract current inventory. Your liabilities should include your equity. This article links you to a free downloadable template for a balance sheet.

Ratio Analysis of Financial Statements

You keep hearing about ratios, but a company’s trustworthiness or value must be crunched into a number so that investors and lenders can make decisions about the company. Those numbers help the owner make decisions about cash on hand, accounts receivables, and much more. Learn here how the business owner can reach a liquidity ratio and give it the proper weight. Likewise, he must look at profitability ratios to see if, over a longer term, profitability remains dependable. Take a look, also, at efficiency ratios and long-term solvency ratios.

Exactly What Is Solvency?

Solvency problems, on the other hand, arise when the business simply does not have the money or the assets to cover its debts. The most common example occurs when a company does not have the assets to back up its request to borrow money or its needs to raise money quickly for specific situations. When a business owner gets into trouble and he has no financial options to save his business, he is insolvent.

Overview of Solvency Ratio Analysis

Reviewing your solvency helps you determine if you’ve gotten too far deeply into debt to remain viable if disaster strikes. Learn about the debt ratio, which is the reverse of the liquidity ratio—liabilities divided by assets. You will be able to see if too much of the money on your books comes from creditors rather than investors, which is not a good sign. Your ratio should be no greater than 0.5, although the acceptable number can vary according to industry.

Why Is Liquidity Such a Primary Factor?

It doesn’t do any good to be solvent if you’re not liquid. What should a company do if it has a large cash reserve? Your immediate

recommendation might be investment in more capital equipment. After all, if a factory has a bigger assembly line, it can turn out more gadgets, which means more sales.

But what if the market for gadgets drops? People just don’t want them anymore. The business owner who sank all his money into producing more of them will be in sorry shape.

Suppose the business owner decides to split the extra cash. Some of it, yes, he invests into capital equipment and expansion. But much of it will go into short-term investments. If the owner suddenly finds a need for cash—what if a tornado strikes the factory and blows away all his equipment?—he can convert his investment back into cash and remain solvent. He has maintained his liquidity.

How Liquidity Affects Market Value and Book Value of an Investment

The company’s financial statements demonstrate its liquidity—current as of the date the statements were prepared. In other words, a company’s financial state is constantly changing with day-to-day market conditions. If a company has a high liquidity ratio, investors are more likely to feel comfortable putting their own money into that company.

Learning Guide: Interpret and Use Ratios

Here you will come to understand why a business manager should deal in ratios rather than just the figures. The owner can plan strategies to increase production or pull back till inventory is sold. The banker will decide that if the company is sufficiently liquid to cover any needs that arise, the company will be a worthwhile investment.

Acid Test Ratio: Examples and Calculation

For purposes of calculating liquidity, the acid test ratio excludes inventory as an asset. After all, investors consider that even if the company doesn’t sell another gadget, they still want to recover their investment or loan. For this purpose the assets will include only cash, short-term investments, and accounts receivables.

Interpreting the Liquidity Ratio

Once you’ve got the ratios done, what do they mean? What should the owner be looking at, and what do investors check? You’ll find useful examples here such as a company that holds high amounts of cash on hand. Why is that not a good thing? That means the owner is not putting the cash to work for the business, neither investing in capital equipment nor in short-term high-yield investments. When accounts receivables are too high, that means the owner needs to coax his debtors into paying up or else slow down on the credit he extends.

Analysis of Common Size Financial Statements

A common size financial statement dispenses with the exact amounts of assets and liabilities. Instead, the owner chooses a year to use as a base or benchmark for the business and its ratios are represented at a value of 100%. Numbers for subsequent years are also converted to percentages. The person who is reviewing the financial statement will be able to see if the business’s profitability is increasing or decreasing and, in some cases, if a pattern is evident.

Common Statement Analysis: A Method for Analyzing Financial Statements

Investors ask companies to provide uniformity in their statements so that they can see how a company does compared with other similar companies. Choose a set time for analysis of liquidity is difficult because of the changing value of money as time passes. common size analysis and common base year analysis are two ways of looking at financial statements that guarantee uniformity across the board.

Analyzing Your Liquidity

As a new business owner, you have no real indicators of future business liquidity. You can only estimate your current situation based on the start-up money you used. Suppose your business is called JoJo’s Soaps—you have a huge interest in aromatherapy and nice soaps, but you know very little about financial statements. What do you do next?

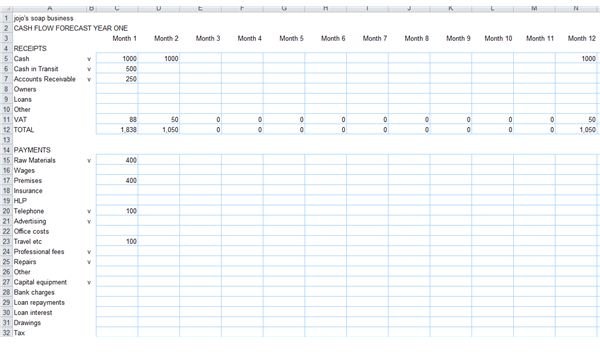

The first thing you should do is download and fill out a Cash Flow Proforma. This is a form that allows you to enter all anticipated

revenues and expenditures on a monthly basis. The first article below links to an Excel Cash Flow Proforma that you can put to good use. As the months pass, you will begin to see a pattern—either you end each month with an operating profit, or you are in the red.

Suppose at any given time your business has $1,000 in cash on hand, $5,000 in soap-making supplies, and accounts receivables of $1,000. Your current liabilities—rent and business loan payment plus monthly expenses—amount to $3,800. Your available cash appears low because you have taken care to insure your business, but your liquidity ratio is 1.84–respectable.

Sam’s Slippery Soap across town has $1,500 in cash on hand, $5,000 in supplies, and receivables of $1,000. Sam has more cash on hand because he has not bought catastrophic insurance. Otherwise his expenses are the same as yours, about $3,800. When a tornado strikes, your insurance company replaces your lost supplies, but Sam is out of luck. His supplies are gone. He cannot replace them with his cash on hand. His liquidity ratio drops to 0.53 (the cash plus the receivables divided by expenses). He does not have the money to replace the supplies and he cannot convince anyone to loan him the money with that ratio. He is insolvent.

How often should you perform a liquidity analysis? The answer to this is that measurement of liquidity—and managing the risks that go with it—is an ongoing process. As each year passes, hopefully you will see a consistency or similarity in positive ratios. That consistency will indicate reliability, something that is a key factor for anyone looking at your business with an eye to invest in it.

Why You Need Cash Flow Proformas

Use the free downloadable template linked to this article so that you can enter your cash in bank, cash equivalents, accounts receivables, and other assets. You will also be able to enter the amounts of all business expenses. The image above is linked to this article.

How to Do a Comparative Financial Statement

At the end of your first year of business, you will end up with a liquidity ratio—for one year’s time. As you move into your second year, you will eventually become able to prepare a comparative financial statement. You are required by financial accounting standards to maintain these records for the previous accounting period.

Using Accounting Ratios to Measure Your Company’s Financial Health

You got into the business of soap making because you love fine soaps and aromatherapy. You were smart enough to figure that out, and so you can certainly understand all the accounting formulas and ratios that a successful business owner will track.

References

- Images

- sxc.hu, SRBichara , royalty-free license

- sxc.hu, guitargoa , royalty-free license

- Image of Balance Sheet and Cash Proforma provided by Jean Scheid