Standard and Poor’s–aka S&P–has roamed outside its prescribed jurisdiction in downgrading the United States’ credit rating. Let’s look at this agency. Not only does S&P refuse to admit its accounting errors, it’s also under scrutiny for possibly leaking information about the downgrade.

Who Expected This?

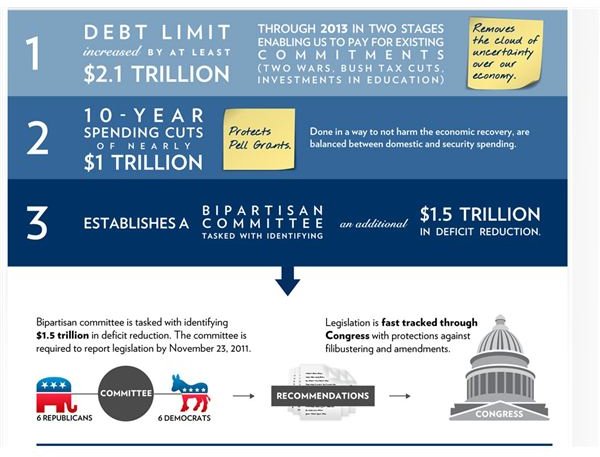

Well, we waited on tenterhooks to learn how our government’s decision makers would resolve our debt ceiling issue. There was no

collective sigh of relief that it was done: We all felt aggravated to one degree or another with our lawmakers because of their squabbling. But we always knew that at the eleventh hour, some kind of agreement would allow us to continue paying our bills.

When newsmakers spouted off about the dire consequences of a possible reduced national credit rating and higher interest rates, we just blew it off as so much rhetoric.

And then Standard and Poor’s, in its so-called infinite wisdom, decided to downgrade the United States’ credit anyway. This was not done immediately after the deal was signed into law, however; the downgrade occurred five days later. We heard the news of the agreement on Monday, August 1, but it was Friday, August 5, when Standard and Poor’s announced its arbitrary decision for the credit downgrade. Why the delay in the announcement?

Who Knew What When?

Kara Scannell, from CNN’s Financial Times , reported on August 12 that the U.S. Securities and Exchange Commission’s Examination Staff has asked Standard and Poor’s to reveal who on the company’s staff knew of the downgrade prior to its tardy announcement. The request was initiated by Senator Maxine Waters (D-California), who speculated in a letter to the SEC that Standard and Poor’s might have “selectively disclosed information about the downgrade…to certain financial institutions…before that information became available to the public.”

If people who knew about the downgrade “traded ahead” of it, and if they advised their associates and acquaintances to trade also, the effect would be a negative valuation of investments and retirement accounts throughout the entire country.

If you think that kind of thing would never happen among honorable people, just remember that Martha Stewart spent five months in the pokey in 2005 for participating in exactly that category of crime. Then remember the blithe ratings given by the ratings agencies to the ill-fated mortgage securities of 2008. And last, take a look at your 401K.

Nobody can dispute the rocky rollercoaster ride taken by our stocks, bonds and other investment instruments since the downgrade. So the question keeps rearing its ugly head. You don’t have to be a forensic accountant to wonder: Exactly what did the people at Standard and Poor’s know, and when did they know it?

Maybe It’s Payback Time

Possibly Standard and Poor’s downgraded the U.S. credit as reprisal for being scrutinized by the Justice Department. CNN reported on August 18 through a Reuters news release that the U.S. Justice Department for some time has been investigating Standard and Poor’s for its indisputable history of faulty ratings. Senator Carl Levin (D-Michigan) told Reuters staff that a report issued in April documented “reckless actions and significant conflicts of interest on the part of the credit rating agencies.”

The investigation clearly began before Standard and Poor’s downgraded our credit. It sounds like S&P has been playing a little tit for tat, if you ask me. Why else would the agency wander outside its jurisdiction to concern itself with our level of congressional function? Actually, just what business is it of theirs, as long as we pay our bills?

The Person Behind the Push

In an additional wrinkle to this story, Ellen Brown of the Sky Valley Media Group on August 20 reported that once President Obama had signed the new agreement into law, the person who “personally led the push for a U.S. downgrade” was Standard and Poor’s CEO, Deven Sharma. She quotes writers from an assortment of news outlets who believe that Sharma for a few years now has been working to bring about a new world economic order, one in which the United States holds no more sway than any other country.

Sharma wields significant influence as a “key contributor” at the elite Bilderberg Conference, an annual summit of world financial leaders who meet for the sole purpose of discussing global financial issues. It was at the 2009 meeting that Sharma advocated “an end to the dollar as the global reserve currency.”

Those curious about what happens at Bilderberg can read the words of one of its founders in a series for London’s The Guardian written by Jon Ronson. In 2001, this key person explained, “To state that we were striving for a one-world government is exaggerated, but not wholly unfair…We felt that a single community throughout the whole world would be a good thing.”

Are you kidding me_?_ The flower children of the ’60s tried the same type of thing. A weirdo named Charles Manson went a different route, also to attain a specific world order. Neither of those ventures worked out very well, thank goodness. Maybe Sharma sees our nation’s downfall as a way to launch his own personal global financial agenda or maybe he just doesn’t like this country.

There’s also the matter of the $2 trillion error committed by Standard and Poor’s when it was going over the United States’ numbers in preparation for the downgrade. When the error was brought to S&P’s attention, the company refused to budge. “Oh, that little error,” S&P more or less said , “Well, we just don’t like how your congressmen get along, so we’re going to downgrade the USA anyway.” What’s up with that?

The Plot Thickens

In May, about two months before the S&P downgrade, the SEC released a proposal for the ratings agencies to (among other things) correct errors, create a greater transparency of ratings agencies’ methods, apply uniform methods across all ratings agencies, and curtail conflicts of interest. The proposal allows for a specific process to correct errors.

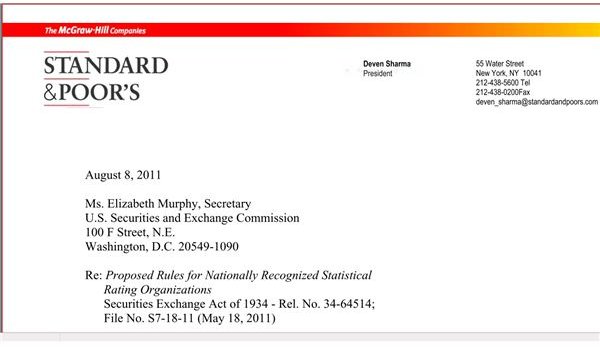

Sharma—a native of India, who moved to this country to take advantage of education and employment opportunities—fired back in a letter dated August 8 that the SEC cannot expect a “one size fits all” approach from ratings agencies. Sharma also protests that the SEC cannot tell S&P that something is an error—because the SEC would be forcing its opinion upon S&P that something is in fact an error. I’m here to tell Dr. Sharma that $2 trillion is a significant accounting error. He must have missed class the day they taught that in school.

Sharma also says that the SEC proposal to open up the ratings business to greater competition will actually end up costing more money, thus restricting competition. My kids give me strange excuses like that when I want them to eat their broccoli.

For the record, of the two other top-rated ratings agencies, Moody’s has only limited objections to the SEC’s proposals relating to the number of modifications required by the new rules, while Fitch Ratings generally supports the spirit of the new rules.

You Can Write to Deven Sharma!

So what have been the effects of the downgrade? As I mentioned, I just can’t look at my retirement account right now. Financial advisers say if you’re in the market for the long term, just stay put. Of course there are other effects, such as the massive diversion of funds from the stock market to Treasury notes and bonds, with its added effect of driving down their interest rates. Local, regional, or state agencies that rely on T-bills for interest income are sure to take a hit this year.

Write to your legislators to keep the pressure on Standard and Poor’s. Maybe the IRS could audit S&P; that would personally make me happy. In the meantime, we’ll have to turn our attention to the twelve legislators—the Dirty Dozen—chosen by the arbiters of our debt ceiling agreement to reach a compromise involving spending cuts and revenue increases. Don’t forget to email them. Heck, you can even send Dr. Sharma an email—just click on the image of his letterhead on this page for his contact information. Just be sure no matter who else you write to, let me know your thoughts in the comments section below.

References

-

Ronson, Jon. The Guardian: Who Pulls the Strings? (part 3), published March 2001, at http://www.guardian.co.uk/books/2001/mar/10/extract1

-

Images

AdvertisementBipartisan Compromise Infographic at WhiteHouse.gov. See the full graphic at [http://www.whitehouse.gov/infographics/the-bipartisan-compromise](/themes/brighthub/tools/Bipartisan Compromise Infographic at WhiteHouse.gov. See the full graphic at http:/www.whitehouse.gov/infographics/the-bipartisan-compromise)

sxc.hu, by tulp , terms of service .

Deven Sharma from S&P’s website

-

Deven Sharma’s letter of August 8, 2011, to the SEC, retrieved at http://sec.gov/comments/s7-18-11/s71811-32.pdf -