A cash receipts schedule is not a regular reportorial requirement in the ordinary flow of business transactions–hence not many people are in the know of its uses or who uses one. Financial managers utilize them for budget analysis, while bankruptcy courts require them from Chapter 11 debtors.

Knowing the Users and Sources of Data

Accounting-wise, a schedule is a supplemental listing of certain particulars and their values that supports a principal document. Based on this description, creating a schedule of an entity’s cash receipts would be easy to visualize.

If the accounting system is manually performed, there is the cash receipts book to refer to, which contains a detailed listing and summary of the daily and monthly sales transactions. If on the other hand the business has a computerized system, the “point-of-sale” module can easily provide the same sets of information for all the items scanned as sales transactions.

However, the users need to know not only the cash that was received over the counter but also amounts directly credited in the entity’s bank account. Thus, other information will come from bank records and/or from the credit card company’s confirmations that the selling entity’s account has been credited. The data to include as details of the schedule and how to present them will depend on its user.

-

The financial manager uses it for budget analysis, in order to determine the cash flow trends during the most recent and applicable business cycle.

Advertisement -

A Chapter 11 debtor, or an entity or individual who has formally declared bankruptcy, is required to submit it as a supplementary document to the Monthly Operating Report (MOR). This is submitted to the bankruptcy court that has jurisdiction over the debtor’s financial activities.

Examples of a cash receipts schedule and explanations are provided below to better illustrate how this document is used as supplemental information for a principal purpose.

To Support a Budget Analysis

Estimating the cash inflow of the business requires an analysis of how the business generates its cash increments for a particular period. The most common timeframe used for summarizing cash receipts is on a quarterly basis, that being the most reasonable length of time for a budget’s review. That way, the financial performance of a business is monitored through a timely analysis of the variances.

The financial manager’s objective is to immediately determine latent issues that were not considered during budget preparations. In other cases, there is a need to determine how the volatility of current market conditions could be affecting the cash inflows, in ways that call for remedial actions. Click on the corresponding images to get an enlarged view for a better illustration of the explanations regarding its uses

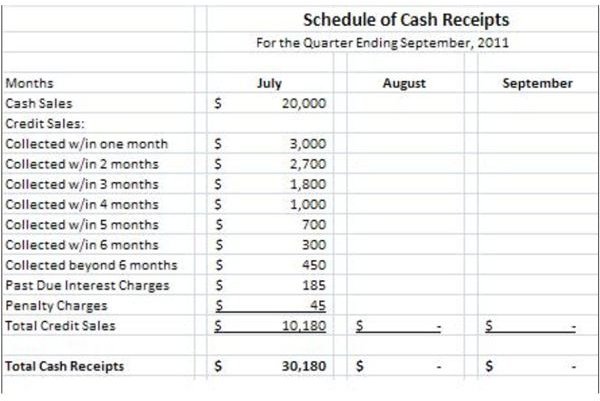

Example 1:

In this example, the cash inflows of the business are derived from cash and credit sales. The collections from credit sales are presented in such a way that the financial manager can readily perceive how much of their cash inflows are derived from over-the-counter operations and from those that were received from back-office collections. The schedule further shows the collection trends by providing details of the monies received, within the same month or extended beyond one month.

These figures will be compared to the corresponding projected cash inflows to establish and analyze the variances that are too far off from the projected baseline. Once the columns for the succeeding months have been filled, further comparisons and analysis will be performed to study the trends on how much cash is coming in and from which types of sales transactions they are derived.

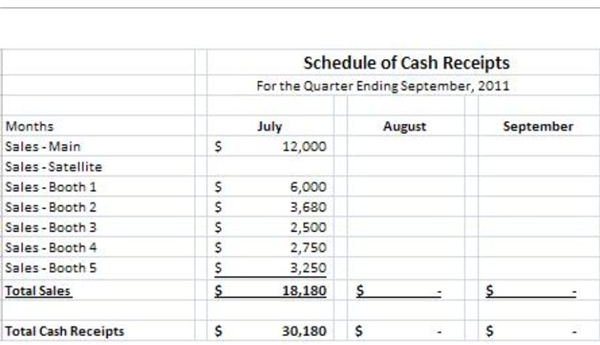

Example 2

The second example furnishes a different set of information, in which the inflows are distinguished according to the outlets that bring in the cash. In this example, it readily shows that the main bulk of the sales transactions are generated by the main outlet.

However, the financial manager will likewise use this information to assess the efficiency of the main sales outlet in granting credits, inasmuch as the satellite outlets sell only on a COD basis. In comparing this set of information against those presented in Cash Receipts Schedule 1, it can be gleaned that of the $20,000 COD sales realized for the month of July, $18,180 were generated by the satellite booth and only $1,820 COD sales were generated by the main office.

A question to ponder would be: “If the satellite outlets can generate as much as $6,000 COD sales and $2,500 at the least, what’s stopping the main outlet from selling as much in COD sales?” Although the selling prices of credit sales are higher, there was no edge created for the amounts generated by the main outlet over those sold on a COD basis. Thus this issue is a matter to analyze and further investigate as far as the financial manager is concerned.

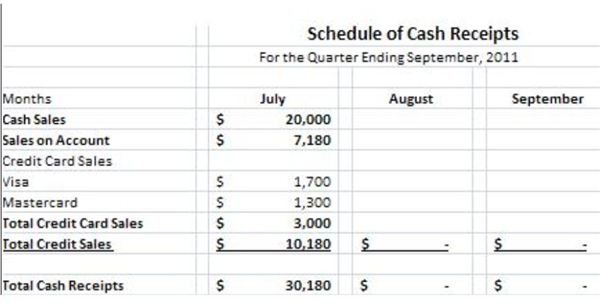

Example 3

The third example of the schedule presents the type of credit sales being extended to customers. The information provided shows how much of the purchases were sold on credit by way of credit agreement terms and how much were sold via credit card payments. Inasmuch as credit purchases via credit cards are as good as COD sales, getting information about the sales extended to customers on account as a form of marketing strategy can be determined.

In our example, the information reveals that out of the $10,180 cash receipts classified as credit-based, only $3,000 were sold via credit card payments. The rest, amounting to $7,180 were sold on account from previous months’ transactions. It can be surmised, therefore, that the $3,000 in cash receipts collected within the same month, provided as information in the first schedule, were sourced from credit card sales.

The rest of the monthly collections exceeding one month are from the credit sales handled by the main outlet. This denotes that the efficiency of the main outlet is the least favorable, since the bulk of its sales take more than a month before they create an incremental effect on the company’s cash position. Some are even considered past due, by basing on the past due interests and penalties received. Obviously, the financial manager has gathered enough information on which to base specific remedial actions, before the entity’s credit sales pose greater problems to its current cash position.

As Supplementary Documentation to the MOR Required by Bankruptcy Courts

The U.S. Department of Justice requires individuals or individuals with sole-proprietorships that formally filed bankruptcy status under Chapter 11 of the Bankruptcy Laws, to submit reports of their monthly operating expenses. Said reports should be submitted on or before the 20th of the following month to the bankruptcy court that monitors their financial activities.

It is important that the information contained therein are based on the balances appearing on the debtor’s actual records and not based on information appearing in bank statements.

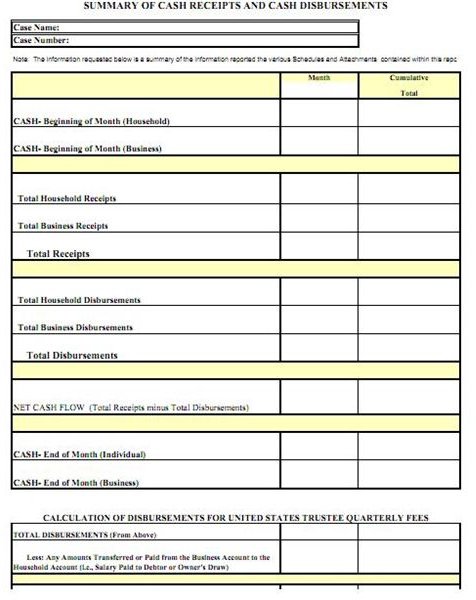

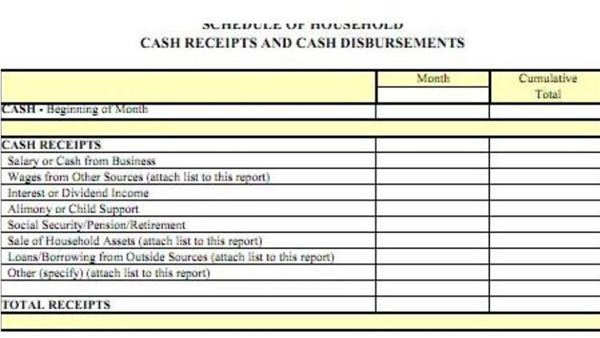

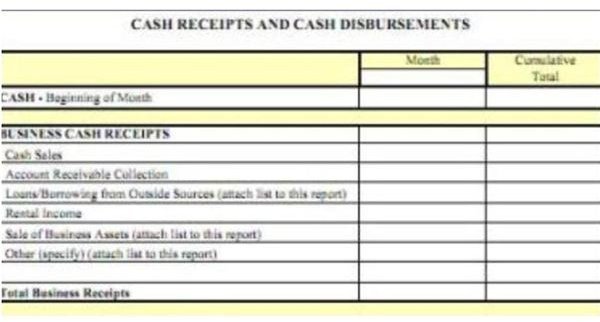

The Chapter 11-debtor who does not operate any business is required to submit a Summary of Cash Receipts and Disbursements and a Schedule of Household Cash Receipts and Cash Disbursement, for the court’s evaluation purposes.

However, if the Chapter 11-debtor is operating a business, the said individual has to submit the additional schedule of cash receipts from the single-proprietorship business. (Images of examples are from the U.S. Department of Justice - find the link in the Reference section below).

Under the Chapter 11 ruling, a debtor may to seek protection from the bankruptcy courts to remain in possession of his assets, as he tries to reorganize his or her finances or business. If approved, the debtor is classified as a “debtor-in-possession”, which stands in contrast to a debtor who does not qualify. As a consequence, the latter loses ownership of his or her assets since the court will issue an order for the assets’ disposal or sale, as a means to satisfy the obligations owed by the debtor to his creditors.

As a “debtor-in-possession”, the individual will submit the prescribed forms of MOR as supported by the schedules of cash receipts and disbursements.

Understand the above uses, since today’s current computerization technology has an abundance of capabilities in terms of report generation covering the different accounting data . Based on the examples and explanations above, a business owner can easily make his or her own analysis by creating schedules and summaries of how different business transactions are being handled.

References

- Image by TJRC Findings of Fact, Conclusions of Law, and Order Approving Sales of Debtor’s Assets / Wikimedia Public Domain –

- Images of Cash Receipts Schedule 1, 2, and 3 were created for this article by the author.

- U.S. Department of Justice. Instructions for Preparation of Debtor’s Chapter 11 Monthly Operating ReportIndividual and Indidvidual with a Sole-Proprietorship – http://www.justice.gov/ust/r21/docs/general/chapter11/mor_individual.pdf

- Image by Olybrius - Toulouse Cash Register / Wikimedia Public Domain —

- U.S. Courts. Reorganization Under the Bankruptcy Code — http://www.uscourts.gov/FederalCourts/Bankruptcy/BankruptcyBasics/Chapter11.aspx