Chase Bank takes the top position as the country’s number one SBA lender according to their June 2011 press release. The release offers up some interesting statistics on where the money’s going and how new clients can qualify for SBA loans. Is this all true or is Chase Bank promising the impossible?

The SBA Doesn’t Lend Money

I must say here first off that many folks out there think the Small Business Administration (SBA) lends money—it does not. The SBA only guarantees a portion of the loan depending on the type. To obtain an SBA loan, (no matter what type) you must go to an SBA lender, much like Chase Bank.

Before you even consider an SBA loan, with Chase Bank or otherwise, you need to know that not everyone will qualify. What does that mean? If you don’t have sufficient collateral or assets the lender can lien, or if you credit is in the toilet, most likely you’ll have trouble. No matter how wonderful you feel your business idea is, a bad credit score (under 650) means you won’t qualify. Finally, you will be required to sign a personal guarantee so forget hiding behind your business structure if you find you can’t repay the loan. This goes for every SBA loan, even if the Chase Bank press release makes it sound like anyone will qualify.

Now that I’ve burst that bubble about getting an SBA loan, why all of the sudden does Chase Bank state they are “IT” if you want one?

What Chase Bank Claims

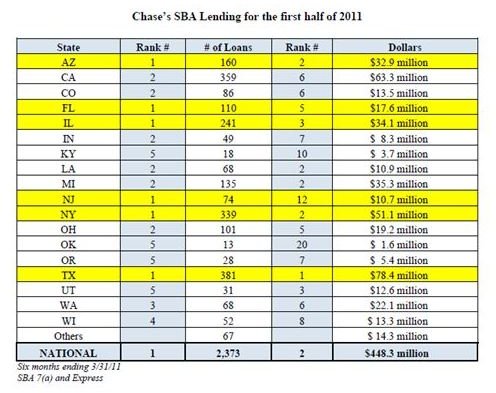

If you take a look at the screenshot to the right

(click to enlarge) from the press release offered by Chase, you will see a pattern. Notice how all the states receiving the most funding are states hit hardest during the housing recession, are states recovering from natural disasters such as floods and hurricanes, or they are states possessing a large minority population. Around $448.3 million has been divvied out via loans according to Chase, but the chart reveals this figure only reflects 7a and Express Loans. The SBA offers all types of business loans including the 7a, ARC loans, 504 loans, and the Express and Patriot Express loans—you can find out more about each type of loan here on Bright Hub .

This great news can be found en mass on the Web including MarketWatch, the Wall Street Journal and smaller offerings such as The Street—all providing an exact copy of the release, which is what news venues do when such releases are faxed or emailed to their news desks.

Attempting to sort out the validity of whether Chase will indeed keep lending remains a mystery to this writer, especially since in reality, it’s really hard to get an SBA Loan whether it’s a 7a, Express or Patriot Express Loan.

The Truth About SBA Loans

Chase Bank’s CEO of Business Banking, Michael Cleary is quoted in the press release: “SBA loans provide the lifeblood for so many business owners who reinvest in our neighborhoods by hiring employees, improving their property and buying supplies and services.” And, “The SBA guarantee allows us to extend credit to a wider range of businesses that need capital to survive and grow.”

There is that old saying, don’t believe everything you hear (or read) because although Chase wants the small business owner to feel comforted that they too will be able to get an SBA loan, chances are, most won’t—not even the ARC Loan that is only $35,000 to aid in paying past due vendor bills.

Whose Fault Is It?

Because all SBA loans have the SBA stamp of approval on them, people tend to blame the stupid business administration—err I mean, the Small Business Association when they can’t obtain a loan. Not fair I say, blame the banks—yes even Chase. I don’t care what their press release states. But the SBA must take a little bit of blame here, too.

Americans were disillusioned from top government officials when all these recovery business loans were all the buzz. Sadly, the SBA (a division of the U.S. Government) had no choice but to advertise and announce these loans, and anyone can read all about the loans by visiting their website. And, beyond the regular loans, they wanted to help military families too by offering the Patriot Express Loan to aid current and retired military families in opening a new business. All of these loans seemed great, wonderful, fantastic and attainable so the American public bought into the announcements of all this Federal aid.

The SBA pays all sorts of staff members and because I indeed did achieve an SBA Patriot Express loan, I can tell you those smiling SBA heads with MBAs will and do seem positive, want you to know they are there to help and some will even offer up the best banks to choose from to ensure you get that loan. What they don’t do is plead your case for the loan, help you write a business plan or really dig into your SBA loan packet and tell you what you left out or what areas need some improvement before you offer up the loan packet to a bank. So, as I said, let’s blame the SBA a little too because we, as taxpayers, are paying their salaries to do nothing really. They do have to submit annual reports to the top office on how many SBA loans were approved in their area, but how long can that possibly take with so many loans being denied?

Meanie Banks

It is nice to see a press release from Chase blasted all over the Internet, but the chart above does say these distributed millions only consist of 7a and Express loans—what about all the other loans the SBA offers?

Express loans (those under $35 thousand) are not worth the paperwork the small business owner has to complete only to be denied. The point behind these express loans was to skip the mess of paperwork and get the cash fast—not true folks, simply not true. On the average, an Express loan or a Patriot Express loan can take up to a year to be approved so where’s the speedy process?

The 7a loans offered by the SBA are probably easier to get—if you have a large company with revenues in the tens of millions. Or, a business can get a 7a loan if their ideas are innovative and fall within one of the groups of businesses the SBA likes—technology, science, farming or healthcare. If your business doesn’t fall in one of these four categories AND produce in the tens of million, you won’t get approved, no matter what you do, how good the credit history of the owners is or how great those cash flow forecasts look.

The SBA also sets rules, but the banks get by those rules. One rule on most SBA loans is the bank is allowed to charge prime plus a percentage—sometimes up to 4 percent. So, if prime was 3.75 percent, and you do get approved, the interest rate could be 7.75 percent. But again, the lender can get around this via loan fees, processing fees, higher interest rates due to risk and no collateral, and all sorts of things they make up. You, as the recipient of the loan may need to pay high processing fees. Sure, the SBA may say it doesn’t allow it, but if you really want the loan, it’s all you can do. If you want to report the fees to the SBA, go ahead, they don’t mind. But, you’ll have to start the process all over again. You’re screwed either way.

No Money?

I do feel for the banks here, if just a little. They really don’t make any money from SBA loans and beyond the paperwork a business owner must submit—triple that for the SBA lender. Only the ARC loan is guaranteed by the SBA at 100 percent, meaning if the business defaults, the SBA will reimburse the bank—but wait, what about the interest due on that loan? Yep, you guessed it. The lender will want payment in full for the interest they can’t recover from the SBA. So, guarantees have some loopholes and that’s really sad for the small business owner.

If you want an SBA loan, even from Chase Bank, don’t expect to get one—they’ll find a way you won’t qualify. The stats they offer up don’t include the SBA loans most small businesses want such as the ARC or Patriot Express loan so Chase isn’t really saying they’re the best of the best. What the press release really means is Chase Bank is offering up millions in 7a loans to qualified businesses that fall in the categories I mentioned above, and they snuck a few Express loans in the stats here and there to make them look good.

Need Another Option?

I remember an old Law and Order show where a small construction company was seeking out investors. To make a long story short, one investor told the detectives (no plot necessary here) they decided that when a company needs money to stay open and survive, that’s not a good investment. If a company needs money to expand or grow, that is a great investment.

As a small business owner, that’s what you must realize here. If you need money to pay vendors, you won’t be able to get an SBA loan—it’s that simple. If, however, you can prove to the SBA lender you are expanding, developing, creating jobs and do have a good credit score, you may just get one. But be patient folks, express does not mean express. It means a very, very long time and it could take up to a year to even see any money from any lender, Chase Bank or otherwise.

Instead of buying into the promises of SBA lenders like Chase, start with the bank where you have your business accounts —you’re likely to get a loan faster (if your credit is good and your business is not in trouble) and with a competitive interest rate.

Finally, for those of you out there thinking anyone can get an SBA loan even with bad credit, it’s not a possibility and SBA lenders won’t even consider a credit score under 700. So it’s often better to look to local banks.

References

Chase Bank Press Release June 15, 2011 - https://investor.shareholder.com/jpmorganchase/releasedetail.cfm?ReleaseID=585177

MarketWatch – Chase Press Release June 15, 2011, “Chase Doubles SBA Lending in First Half of 2011” - https://www.marketwatch.com/story/chase-doubles-sba-lending-in-first-half-of-2011-2011-06-15

The Street – Chase Press Release June 15, 2011 “Chase Bank Double SBA Lending in First Half of 2011” - https://www.thestreet.com/story/11153839/1/chase-doubles-sba-lending-in-first-half-of-2011.html

Image Credits:

SBA Logo - Wikimedia Commons/US Government

Screenshot of Chase Loans Stats via https://www.chase.com

Wrong - Sxc.hu/Cieleke

Fried Baloney - Wikimedia Commons/Public Domain

Empty Pocket - Sxc.hu/playboy

Puppet - Sxc.hu/porah