Surveys indicate that most business owners aren’t aware of the tax deductible benefits available to them, including tax deductions for business casualty losses. Some entrepreneurs even misconstrue that the methods used for determining the deductibles for personal and business losses are the same.

The Basic Requirements for Calculating Losses on Damaged Business Properties

Knowing the methods used to calculate deductible business casualty loss is important especially for home-based entrepreneurs that make use of personal property for business purposes.

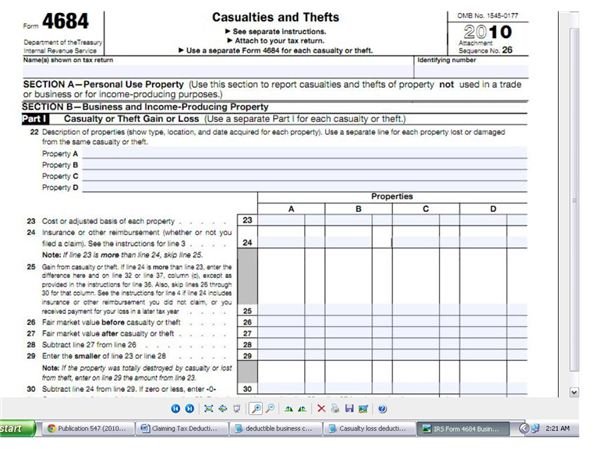

Business loss on damaged property takes into account the value of each asset that was destroyed or lost during a calamitous event. IRS Form 4684-Section B is used to report the casualty losses. As a matter of procedure, the information will be used by the IRS to evaluate the values used as operating expenses or losses to reduce the gross profit realized by the business entity during the tax year.

Readers can take a closer look at the IRS form by clicking on the image at the left. Notice that when calculating claims for business purposes, losses from damaged properties are summarized. The aim is to provide a breakdown of the losses already considered and incorporated as accounting transactions, as a means to come up with a fair presentation of financial statement reports. This stands in contrast to the method used for personal casualty loss in which tax deductibles are claimed by way of Form 1040 Schedule A, as itemized tax deductions.

Nonetheless, the components used to determine the loss suffered from a damaged business asset and for the calculation of personal loss are the same. They are:

-

The adjusted basis of the property – which is the acquisition or original cost plus the cost of improvements and less the cost of depreciation, erosion, amortization or depletion.

-

The fair market value (FMV) before and after the untoward event that led to the destruction of the property or asset. The loss recognized is the difference or the decline in value.

Advertisement -

The amount of reimbursement received to compensate for the loss, the most common source being the proceeds of insurance policy coverage.

At this point, emphasis is given to the $100 personal deduction limit and the 10 percent rule which does not apply when calculating the deductible business loss. These components are discussed in a personal finance article entitled “Calculating Tax Deductions for Casualty Loss”.

Inasmuch as losses resulting from unexpected adverse events are individually calculated, the succeeding explanations and examples are presented accordingly.

Calculating the Loss from Income-Earning Assets or Properties

In claiming the value of losses involving a home used for business purposes, the amount of loss claimed as deductible may be limited. The said home is subject to “Passive Activity Loss” (PAL) limitations.

A PAL emanates from a trade or business for which the owner has no active tax participation, or from rental activities, regardless of tax participation. The basic rule observed is that losses suffered by passive activities cannot be used or applied as a reduction to the income generated by non-passive activities.

Nevertheless, some are allowed but are based on certain exceptions and subject to limitations. The guidelines for determining eligibility as a tax deductible loss are set forth in Form 8582.

For income producing properties, such as those used for rental activities, determining the amount of loss does not take into account the decrease in Fair Market Value (FVM) but instead makes use of any salvage value to determine the amount of loss on a damaged property. Taxpayers operating home-based businesses should reference IRS Publication “Instructions for Form 8582” for proper guidance. (See link in the Reference section of this article).

Providing a Sample Calculation and the Accounting Entries:

Example:

A rental car involved in a vehicular accident left the vehicle in a state of total wreck. The vehicle’s acquisition cost is $60,000, and the accumulated depreciation prior to the incident was $35,000. The insurance company reimbursed the business owner the amount of $20,000. The amount of casualty loss is determined using the following calculations and accounting entries:

- Acquisition cost - $60,000

- Less accumulated depreciation – ($35,000)

- Loss from damaged asset - $25,000

- Less insurance reimbursement – ($20,000)

- Amount of Casualty Loss - $5,000

Accounting entries:

(1) To record the write-off of the wrecked car

Dr. Accumulated Depreciation - $35,000

Dr. Insurance Claims Receivable - $20,000

Dr. Casualty Loss- Car Accident - $5,000

Cr. Car-for-Hire Inventory $60,000

(2) To record the receipt of the insurance reimbursement

Dr. Cash - $20,000

Cr. Insurance Claims Receivable - $ 20,000

(3) Explaining the effects of these entries on the general ledger books

- The accumulated depreciation balance of $35,000 was zeroed-out.

- The car-for-hire inventory total was reduced by the acquisition cost of the wrecked car, valued at $60,000.

- The only remaining value recognized in the general ledger book for the written-off vehicle is the Casualty Loss of $5,000, as part of the business’ operating costs for the year.

Recognizing Loss from Damaged Inventory

The IRS allows recognition of loss on damaged inventory as long as the cause was due to a sudden event that was swift and unexpected. It is an occurrence that is not a day-today event that it took some time for the business entity to contain or mitigate the negative event. The tax agency further recommends two ways for the loss to be reflected in the books of the company. The loss may be recognized as a reduction of total purchases or a reduction of the merchandise inventory on hand.

Example:

An unexpected flash flood hit a community, which adversely affected a garment manufacturing firm’s raw materials inventory amounting to $28,000. Although the raw materials were covered by an insurance policy, there was a deductible of $5,000. In addition, the entity was able to sell the damaged raw materials to a scrap dealer for $3,000.

The calculation for the amount of loss is as follows:

- Purchase Cost - $28,000

- Less: Reimbursement from Insurance – ($ 23,000)

- Loss on Damaged Inventory - $ 5,000

- Less: Sale from Disposal of Asset – ($3,000)

- Amount of Casualty Loss - $ 2,000

Accounting Entries:

(a) To record the loss from damaged raw materials inventory.

Dr. Casualty Loss from Inventory due to Flash Flood - $5,000

Dr. Insurance Claims Receivable - $23,000

Cr. Purchases or Merchandise Inventory - $ 28,000

(b) To record the insurance reimbursement received

Dr. Cash $ 23,000

Cr. Insurance Claims Receivable - $ 23,000

(c) To record sale of damaged raw materials to scrap dealer

Dr. Cash - $ 3,000

Cr. Casualty Loss from Inventory due to Flash Flood - $3,000

(d) To explain the effects of the entry in the general ledger book:

- The value of the raw materials damaged reduced the amount of purchase costs for the year.

- Technically, the reimbursement received from the insurance company ($23,000) plus the money received from the sale ($3,000) of the damaged raw materials, can be used to buy the replacement for the damaged goods.

- The insurance claim receivable was zeroed-out.

- The casualty loss which initially represented the $5,000 insurance deductible was reduced to $2,000, since a salvage value of $3,000 was realized by the Sale from Disposal of Asset.

Determining the Loss from a Damaged Leased Property and Other Assets

If an entity is merely renting the place of business and the entity is liable for the damages, the cost of repairs shouldered, less any reimbursements received or salvage value realized, will be the amount of loss to be recognized.

Basically, minor losses can be merely recognized as ordinary business loss or expenses by an entity as far as the general ledger books are concerned.

What is important though is to report the type and nature of the loss in IRS Form 4684-Section B, and retain documentation to support the circumstances and the amounts of the deductible business casualty loss claimed for the tax year.

Reference Materials and Image Credit Section:

References:

- Cost Segregation - Tax Deductions (Cost segregation increases tax deductions) – https://www.upublish.info/Article/Cost-Segregation—Tax-Deductions–Cost-segregation-increases-tax-deductions-/547185

- Publication 547 - Main Content Casualty and Theft Loss – https://www.irs.gov/publications/p547/ar02.html#en_US_2010_publink1000225406

- IRS Instructions for Form 8582 –https://www.irs.gov/instructions/i8582/index.html

Image Credits:

- IRS Form 4681 - Casualties and Theft /IRS.gov.

- By Mcumpston / Wikimedia Commons

- By Harry Rose / Wikimedia Commons

- By Casey Deshong / Wikimedia Commons