Are you confident that your cash is adequately protected? You may think that insurance coverage is enough to cover your losses against theft or embezzlement; yet, even insurance companies take into account the effectiveness of internal controls instituted to protect their own interests.

Guiding Principles for Setting Up Policies and Procedures

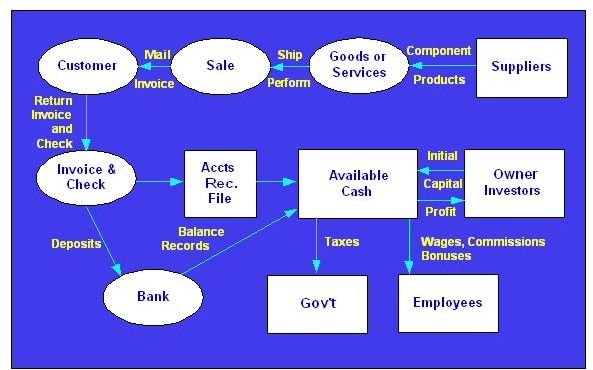

Understand that a reference to cash covers more than currency that physically exists and is actually on hand. As a matter fact, one of the initiatives for keeping money secured is to make sure that only a minimum amount is physically available on the business premises. This denotes that the monies subject to internal controls include those that are kept intact as deposit accounts, from where funds are withdrawn as a means to meet the company’s financial requirements.

Best practices recommend depositing most of the cash received during the day to a reliable local depository bank. In some instances, a depository bank’s armored vehicle is requested to pick-up the deposit to ensure security of transport.

The most important aspect of cash management is to institute efficient and effective security measures for cash handling. Internal control policies and procedures are therefore implemented to safeguard funds and monies against theft, waste and embezzlement.

There are twelve operational principles observed and used as guidelines for setting-up policies and procedures for managing cash and its movement. These are:

(1) Recording and documentation of transactions

(2) Segregation of duties and responsibilities

(3) Authorization of transactions

(4) Timeliness of payment

(5) Review and verification of documents

(6) Security of physical conditions

(7) Supervision, monitoring and traceability of fund movements

(8) Planning and budgeting controls

(9) Establishment of accountability

(10) Limitations over accessibility and availability

(11) Summarization and reports

(12) Element of surprise in relation to periodic audits and related initiatives.

Policies and procedures are formulated by integrating these principles as built-in preventive and corrective measures in managing the following aspects of business operations:

- Receipt or collection of payments

- To defray costs and purchases

- To pay for obligations

- The maintenance of unused or available funds.

Securing the Monies Collected from Business Operations and Other Sources

Receipts and collections are the most vulnerable and fraud-sensitive transactions related to cash handling. Internal control requires that balancing and reconciliation procedures are performed daily to ensure that all monies received are handled and recorded accurately. That way, origins of overages and shortages can be easily established, while the corresponding accounts affected are brought to the correct balances at the end of the day. Starting from a clean slate at the beginning of each new round makes the job of keeping the books balanced a lot easier.

Keep it in mind that cash receipts include customers’ checks and credit card payments as well as electronic fund transfers, inasmuch as they also translate to increments in fund deposits. The acceptance of other modes of payment other than by way of over-the counter transactions provides a more secure method of receiving payment.

On the other hand, certain cash transactions are classified as “cash equivalents ," which represent surplus funds invested in high-yielding accounts in order to optimize earning capacity while awaiting better investment strategies. Their control measures relate to investment practices, since their account balances are likely to stay fixed for a specific period of time.

The control procedures discussed below are related to the receipt of cash at point of sales (POS) and transfers of credit payment collections.

Use and Control of Automation

-

For businesses that deal heavily with cash receipts, a computerized cash register incorporates other control features by simultaneously transmitting the cash transaction to other program modules. This system guarantees the consistency of amounts used to record related transactions. Actual cash balances at the end of the day are compared to the end-of-day balance generated by the machine.

Advertisement -

A control officer affixes his or her initials at the beginning of each cash register tape to signify that all accounts are cleared and shall start with zero balances.

-

Transfers of cash collection to the depository bank are properly noted by a control officer on the register tape before securing the money and other cash items in a locked bag. Moreover, the accuracy of the machine’s cash balance should be ascertained before any transfers are made.

Advertisement -

Transfers may include assumption of shift-schedules between cashiers, but should not hamper the business operations. The objective is to determine at which point cash overages or shortages occurred and under whose responsibility. In which case, any discrepancies noted are temporarily logged as cash overage or shortage but with the intention of fleshing-out the discrepancy at the end of the day.

-

All transfers are documented by way of a transmittal form, on which the breakdown of actual cash transferred is indicated.

-

The monies received by the company’s credit collection unit are transferred to a cashier before the machines are closed for the day. Transfers are supported by a credit collection report along with the transmittal letter. The reports are likewise machine-validated or supported by a register tape.

-

A daily cash report is prepared by each cash register operator, and summarized by the supervisor-in-charge. Copies of the reports and transmittal letters are forwarded to the accounting department to facilitate or validate all back-office accounting entries.

-

The cash register is utilized purely for sales transactions and should not be used for in-house check encashment. Sales returns, refunds or discounts are the only transactions that would create a reduction to the total cash collections for the day.

Physical Handling of Collections

- All monies received over-the counter are counted and verified in front of the paying customer before processing the official receipt that acknowledges receipt of payment.

(a) Official receipts are pre-numbered regardless if it is manually or electronically prepared or generated.

(b) The person receiving the cash payment should not perform dual functions related to accounting or recording of business transactions.

(c) Payments received in the form of checks are all payable to the business entity.

(d) Post-dated checks are not treated as payments but only as “items-held-for-safekeeping,” for which a register is maintained for purposes of monitoring the dates they will be processed as payments.

(e) All documents are filed chronologically to facilitate future audit reviews.

(f) Both the internal and external audit teams shall conduct surprise cash counts at the onset of their audit engagements. The resident control officer periodically performs unannounced cash counts aside from the daily balancing routine. Balances of accounts receivables are directly verified with the customers by sending out confirmation letters.

Controlling the Funds Used for Defraying Business Costs and Purchases

As a rule, all cash outlays related to procurement of goods, assets and services are controlled through the development of a properly planned budget. A budgeting system organizes the use of monies as payment for expenditures and purchases and ensures that fund usages have justifiable purposes in relation to the company’s annual financial projections.

1. Only those expenses included in the budget plan shall be processed for payment. In line with this, all requests for payment for major purchases and expenses, including salaries and wages, shall bear the budget officer’s approval to denote propriety and fund availability.

2. The organization shall institute a purchasing system and a department that handles the processing of purchase requests, actual receipt of the purchases and subsequent requests for payments.

- 2. a -The purchasing system addresses the methods used and procedures performed in connection with the procurement of goods and services , i.e. bidding, submission of quotations, purchase orders, receiving and verification of goods delivered, warehousing or storage as well as maintenance of stock inventory.

- 2. b - Expenses deemed as minor, minimal, ordinary and frequently recurring within a four-week period are paid from the petty cash fund maintained by each department or organizational unit. These expenses do not require a request for payment and budgetary approval but should all be disbursed in accordance with the imprest system’s procedures for cash handling. Internal control policies and procedures for this purpose are distinct but are part of the company’s business procurement processes.

3. Processing of requests for payments covering substantial business expenses that recur on a monthly basis, i.e. utilities, payroll, benefits, fall under the responsibility of the accounting department‘s administrative unit.

4. All requests for payments are approved by two authorized officers. One officer is responsible for review of supporting documents to determine the validity, accuracy and timeliness of each request. The other approving officer assumes responsibility for overall propriety of the transaction.

5. In larger organizational structures, approving authorities are assigned for different value ranges or brackets as this system determines scope of authority and responsibility .

- 5. a - In extraordinary cases, for which supporting documentations are not yet unavailable or not possible, “one-over-one-approval’ of the payment request will be required. This means, a higher or the highest signing authority (the board of directors) decides on the reasonableness of the transaction. Moreover, overall command responsibility for the transaction shall be assumed by the most senior approving officer/s.

- 5. b - In other cases, certain expenses are supported by justifications, documentation and budgetary approval but ongoing negotiation or recent developments necessitate further review by a specialist (e.g. attorney, accountant, analyst, etc.). These types of transactions require “subject matter approval” before a “one-over-one approval “can be secured.

Please proceed to page 2.

Controlling the Funds Used for Defraying Business Costs and Purchases (continued from page 1)

6. The accounting department handles the processing of all approved payment requests by issuing checks that are payable to the individual or entity named in the supporting documents.

7. It is important that the payee of the check issue an official receipt to acknowledge that payment has been received. Otherwise, the check payment is not physically conferred until such time that a valid official or provisional receipt can be issued.

8. The purchasing department prepares a summary of all purchases made during the month and submits it to the accounting and budget departments. These departments, on the other hand, will reconcile the report with their own set of records to ensure that funding requirements have been observed and that the transactions are properly recorded, whether manually or electronically.

9. The internal control auditor(s) conducts an annual audit by reviewing the accounting records and supporting documentation. An unannounced physical inventory of the company’s assets and stock inventory shall be conducted periodically.

10. Annual review and examination by external auditors to evaluate compliance with the Sarbanes-Oxley Act is also performed.

Control Procedures for Payment of Obligations

A reference to obligations refers to trade payables that require timely settlement as a means to avoid additional costs in the form of interest and penalty charges. Otherwise, the additional expense creates an unplanned burden on the company’s cash position. There is also the matter of determining the validity of debt or trade agreements and the absence of stakeholder conflicts of interes t.

Trade Credits:

-

The purchase or expense to which a payable is related has a corresponding purchase order that bears the approval of the budget department. Although actual payment was initially deferred, it is understood that the purchase of goods or services is part of the financial projections for the year and presents a benefit to the company.

-

Each obligation or payable has a separate subsidiary ledger that is manually or electronically maintained for purposes of monitoring individual balances and due dates. The aggregate amount of all subsidiary ledgers is reconciled against the general ledger accounts payable balance on a monthly basis.

-

All trade payables are supported by documents required by the purchasing system, e.g. purchase order, sales invoice, delivery receipt, credit sales agreement, billing statement, etc. All of these documents are presented to the reviewing and approving officers to provide the basis for payment approvals.

-

The control officer should investigate returned items that were noted during delivery of the purchased goods. This is done to determine if the supplier’s billing statement was properly adjusted in order to avoid overpayments.

-

Availability of trade discounts and failure to take advantage of said payment reductions should also be given attention.

-

Evaluation of credit incentives or the lack of trade discounts coupled with comparison of prices against industry standards should likewise be conducted. Consider the possibilities for conflicts of interest and their prevention.

-

The person in charge of administrating the business obligations is not involved in the preparation of checks, nor in the review, endorsement and approval of payment requests.

-

All checks issued as payment for credit obligations are payable to the business name of the corresponding creditor indicated on all supporting documents.

Loans and Other Forms of External Financing

-

Financing or loan obligations require board approval before they are contracted. Moreover, in-depth review and analyses must be performed to justify the necessity of securing financial assistance from external sources. The objective is to determine the business organization’s ability to pay the obligation and potential to recover the cost of money.

-

All loans and other forms of financing obligations are supported by original documents duly executed by the company and the financing institution. Such documents are kept under lock and key by the accountant or any control officer but should always be available for verification. Only photocopies are attached to the related requests for payment. Moreover, payment dates, interest calculations or additional charges are calculated based on the terms and conditions indicated on the related documents.

Other Forms of Liabilities

-

Obligations also refer to federal and statutory liabilities like periodic tax remittances, business permits, licenses, registration fees and the like. They are paid accurately and in a timely manner to avoid unnecessary costs in the form of surcharges and penalties.

-

Other forms of obligations include customer deposits for which proper accounting and agreement with book balances is a must. There should be a periodic review that the deposit requirements are properly maintained. Another matter to look into is the propriety of those instances when such deposits are applied as payment by the customer.

-

All unusual or extraordinary requests for payment of obligations should be thoroughly reviewed before they are endorsed for approval.

-

Internal auditors send out confirmation letters to all creditors for any type of obligation to verify the validity of the payables and their outstanding balances. This shall form part of their annual audit engagement and determine compliance with all internal control requirements. Any breakdown or weakness should be properly reported and along with relevant recommendations for corrective actions.

-

The external auditors shall likewise review and evaluate the transactions related to the company’s obligations and the internal controls for cash handling. Compliance or non-compliance to the requirements of the Sarbanes-Oxley Act should be properly evaluated before a certification is issued to support the fairness and accuracy of financial statement reports.

General Preventive Control Measures

(a) Cash boxes and registers that are unattended are always kept under lock and key. A cash vault or safe serves as a repository for petty cash funds and cash boxes containing collections not yet deposited, during non-working hours and days.

(b) Cashiers, credit collectors and officers who have access to the cash vault or safe, are covered by surety bonds.

(c) The security of the vault or safe shall be the joint responsibility of two key officers; hence, the vault or safe door should have two sets of control combinations. This means one officer cannot gain access to the steel repository’s content without the other’s knowledge.

(d) The monthly bank statement is reconciled against the general ledger’s cash in bank balance by a staff member who is not involved in handling cash transactions or issuance of check disbursements. The exercise will disclose if there are bank transactions not yet recorded on the books or if there are errors or irregularities in the management of cash deposits and check issuances. All canceled checks shall be filed intact and in numerical order, including those that have been voided or nullified.

(e) Accountable forms like checkbooks, official receipts, purchase orders, sales invoices, delivery receipts, debit /credit advices and the like are kept under lock and key and under the custody of a control officer.

(g) All accountability forms related to cash receipts and other trading or purchasing activities used as supporting documents for the filing of income tax returns are duly registered with the Internal Revenue Services and shall bear the agency’s registration marks or control numbers.

(f) Preventive measures are also instituted at point of hiring by carefully evaluating the results of background checking , especially if the person being hired will be tasked to manage or handle cash.

Incidents of robbery, stealing and malversation are reported to the company’s security department who will in turn take charge of reporting the matter to the local crime authorities. The internal audit department or a forensic accounting team will be assigned to investigate the circumstances, procedures, methods, documents and devices used, for purposes of determining the impropriety of cash handling. Weaknesses or breakdowns of internal control will likewise be identified in order to institute corrective and additional preventive measures.

Reference Materials and Image Credit Section:

Reference:

- Retrieved from the author’s personal files used in her private practice as a Certified Public Accountant.

Image Credits:

- By Georgeobancroft / Wikimedia Commons

- By Marcin Wichary / Wikimedia Commons

- Produced by Agência Brasil, Creative Commons License Attribution 2.5 Brazil / Wikimedia Commons

- By Paranoid / Wikimedia Commons

- Released by the United States Navy with the ID 101116-N-3666S-079 / Wikimedia Commons

- By Ctk56 / Wikimedia Commons

- By Membeth / Wikimedia Commons

- By Sheila C. Bair, Chairman / Wikimedia Commons