How do the financial analysts look at a company when trying to find good investments? Find out how horizontal and vertical analyses fit into financial statement analysis to help a reader understand a company’s past, present, and possible future performance.

When it comes to comparing horizontal analysis versus vertical analysis, one must keep in mind that they are contrasting approaches in financial statement analysis but together they help bring clarity and more impact to some items and relationships that might have been overlooked.

Vertical Analysis

Vertical analysis shows each account on financial statement in dollars and as a percentage of another item. The vertical analysis of a balance sheet shows the amount of each item as a percentage of the total assets. Each item on an income statement is shown as a percentage of sales. For example, the cash account on a balance sheet is $8,000 and the total assets are $100,000. The cash account would show 8.0% in the percentage column of the statement. Similarly, the interest expense on an income statement is $50,000 and the sales revenue is $1,000,000; the interest expense would show 5.0% in the percentage column.

A financial statement in the vertical analysis format is known as a common size statement. Common size statements are useful for showing annual changes in a company and when comparing the data from two companies or to industry averages. Two companies in the same industry can be dramatically different in size but the percentages of their common size statements allows them to be compared to each other and also to the industry average.

For example, ZYX company has sales revenue of $500,000 and XYZ company has sales revenue of $5,000,000,000. The interest expense of ZYX is $25,000 and this equals 5% of their sales revenue. The same expense for XYZ is 300,000,000 and this equals 6% of XYZs sales revenue. Though they are of vastly different sizes, the interest expense for both of them is similar and compares favorably to the industry average of 5.5%.

Horizontal Analysis

Horizontal analysis is basically a year over year comparison of ratios or line items financial statements. Each item of the statement is compared to the same item in the previous year and can be expressed as a dollar or percentage increase or reduction on a comparative financial statement. For example, the accounts receivable account in the current assets section of a balance sheet for the year 2009 has an ending balance of $5,000,000. At the end of 2010 the same account had an ending balance of 7,500,000. When the two accounts are compared the increase in accounts receivable is $2,500,000. This would be a percentage increase of 50%. Comparative statements are created that line up the two years together for a comparison. They can just show the two statements next to each other or the dollar or percentage difference in each account displayed in a conveniently placed column, usually to the right of the column or page.

Seeing the most current year’s financial statements next to the previous year’s, or comparing interim statements, gives the analyst and the company a better perspective on how the company is performing. Small changes in an account wouldn’t draw much attention but large ones can be a red flag for further analysis. The example above shows a large increase of 50% in the accounts receivable account that would raise some eyebrows. The cause could be a 50% increase in company sales. This isn’t really a problem and some company execs might be breaking open bottles of champagne over it. But if the increase in sales is only 10% there could be a sudden bill payment problem that developed for some reason and could lead to a shortage of cash for the company’s operations. This could cause an increase in short or long-term debt to raise the cash that is needed.

Exploring Horizontal Analysis Further

Horizontal analysis can be taken further to encompass a number of years instead of just the previous one and expressing the increases and decreases as percentages in terms of a base year. This allows the analyst to determine if any of the company accounts are displaying meaningful trends. The name given to this is trend analysis and the percentages are known as trend percentages.

This kind of analysis is important because it gives the reader a better perspective on the progress of a company than just looking at the data as dollar amounts.

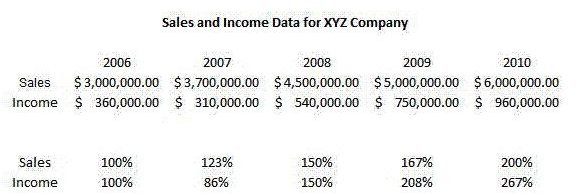

This statement is compared to the same item in previous years and can be expressed as a dollar or percentage increase or reduction on the comparative financial statement of XYZ company. For example, the Sales Revenue account on the income statement for the year 2006 has an ending balance of $3,000,000, 2007 an ending balance of $3,700,000, in 2008 an ending balance of $4,500,000, in 2009 an ending balance of $5,000,000, and in 2010 an ending balance of $6,000,000. The year of 2006 is used as the base year for comparing the other year-end balances. The ending balance of 2007 is 123% more than 2006, 2008 shows to be 150% more than 2006, the ending balance for 2009 is 167% more than that of 2006 and the ending balance for 2010 is 200% more than in 2006. Click on the following data image to view this:

Summary

Horizontal analysis and vertical analysis are important parts of financial statement analysis. It’s important for investors, managers, and others to have an idea of how a company can be expected to perform in the future. These analyses arrange data on the current and past statements in a way that show important relationships regarding this.

- Vertical analysis shows financial data on the current year’s financial statements that is more company specific and in the current timeframe. Each item is expressed as a percentage of the total for the accounts in its category and can be easily compared to other company’s statements.

- Horizontal analysis compares current year financial statement items to the previous year’s items and increases or decreases are expressed as percentages. This makes comparisons to other companies or industry averages easier.

- Trend analysis takes horizontal analysis further using several time periods and trend percentages in a way that can show developing trends.

As far as horizontal analysis versus vertical analysis can be thought of, the contrast is distinct but together these forms of analysis help analysts and investors make intelligent projections concerning a company’s future performance.

References

-

Undisclosed, “Comparative Statement,” http://www.investopedia.com/terms/c/comparative-statement.asp

AdvertisementWayman, Rick. “Operating Cash Flow: Better Than Net Income?”, http://www.investopedia.com/articles/analyst/03/122203.asp#13063441777462&close

Averkamp, Harold (CPA), “What is the difference between verticla analysis and horizontal analysis?”, http://blog.accountingcoach.com/vertical-analysis-horizontal-analysis/

AdvertisementUndisclosed. “Vertical Analysis and Common Size Statements:”, http://www.accountingformanagement.com/vertical _analysis_full.htm

Undisclosed, Veritcal Analysis and trend Percentages", http://www.accountingformanagement.com/horizontal _analysis_or_trend_analysis.htm

AdvertisementUndisclosed. “Vertical Analysis and Trend Percentages”, http://www.accountingformanagement.com/trend _percentages.htm

Image Credit:

AdvertisementDollar Sign/Wikimedia Commons/ScottSteiner

$50 Dollar Bill/Wikimedia Commons/Akjz

Advertisement