An enterprise may offer rebates as part of a sales promotion campaign. To judge the effectiveness of the sales promotion the management must have accurate accounting information with respect to sales rebates. For this reason the accounting entries for rebates must be made correctly.

Types of Rebates

A rebate is a part of the purchase price that is returned to the customer. The rebate will often be related to the purchase of a particular quantity or value of the particular goods within a specified period of time. This type of rebate will often be given after the full amount of the purchase has been invoiced to the customer and paid. It is, therefore, different to a discount given before the goods are paid for, or a discount given as an incentive for prompt payment.

The accounting treatment of rebates aims to show information about rebates in the most useful way for users of accounting. The most useful presentation may differ according to the type of rebate given. Where rebates are given in relation to a measure of customer loyalty such as the quantity or value of goods sold to a particular customer, it is useful to show these rebates separately in the accounting records. Accounting staff should be familiar with the subject of journal entries and rebates.

It is also important to show the rebates as a separate accounting item so the enterprise may keep a record of the amount of rebates given. This information is very useful to management in assessing the effectiveness of rebates as a sales promotion tool. They may be able to measure the extent to which the rebates are increasing sales and measure the effect on earnings. To offer generous rebates may be counter-productive because they may increase the sales but if the rebates are too high, this may not increase total earnings. This important management information must be available and the rebates must be accounted for separately and highlighted in financial information available to management.

The use of rebate accounts is also useful in respect of tracking rebates given to each customer and ensuring that the correct amount of rebate is given. Owing to the different circumstances in which rebates may be given it is essential to include a check as to which rebates have been allocated to and used by each customer. Keeping accurate rebate accounts may help to ensure that the enterprise is aware of rebates that have not yet been taken up by customers. The enterprise may be in a position to remind customers of rebates to which they may have access. This can be an important tool in improving customer relationships and keeping control of those relationships.

Journal Entries for Sales Rebates

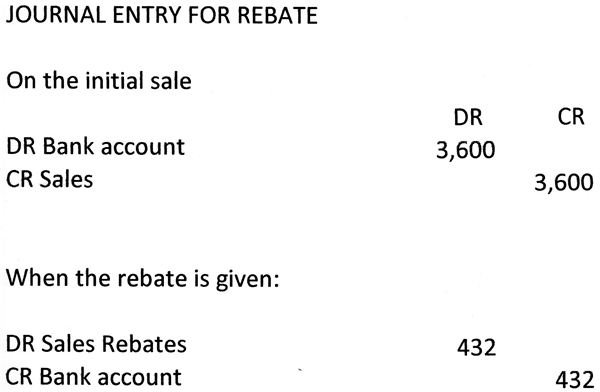

In a situation where cash sales are made, the accounting treatment of the rebate is straightforward. The journal entries reflect the movement of funds in and out of the Bank Account. Where for example a customer has bought equipment for $3,600, the initial entry in respect of the sale would be to debit the Bank Account and credit the Sales Account with $3,600, respectively.

Beyond the purchase price, it then becomes clear the customer is entitled to a 12% rebate amounting to $432. This rebate is then paid to the customer and the accounting journal entry is a debit to Sales Rebates and a credit to the Bank account of $432.

In the case of a credit sale, the entries are slightly different. Taking the example of an item of equipment sold for $1,800, the journal entry for this sale would be to debit the Debtors’ account in the sales ledger for that particular debtor with an $1,800 credit the same amount to Sales. If it is then determined that the customer is eligible for a 15% rebate amounting to $270, this is communicated to the customer and the accounting journal entry is to debit the Sales Rebates for $270 and to credit the same amount to the Debtors’ account for that customer.

The Importance of Accounting for Rebates

Keeping an accounting record of sales rebates is of help in tracking the effectiveness of a sales promotion campaign but also in identifying any problems arising with the offered rebates. For example, some types of rebates require some effort on the part of the customer in registering purchases and applying for the rebate. This can yield useful information to an enterprise about the types of customer making purchases of certain types of product. This may lead to conclusions about consumer purchase decisions and can be used to design future sales campaigns.

Problems may arise if the amount of form filling the customer has to perform to obtain the rebate is too much. If only a small proportion of customers are actually claiming the rebates to which they are entitled, this may be a sign the sales promotion campaign must be redesigned. If the customer considers the rebates are difficult to obtain, this may remove any incentive the sales promotion is intending to create. An adjustment to the method of claiming the rebate may then be required. This type of information can be available to management if the rebates are correctly accounted for and accurate accounting information is reaching the appropriate decision makers within the enterprise. For this reason familiarity with journal entries and rebates and the ability to make the correct entries in the accounting records is an important function in any enterprise.

References

“Accounting treatment of cash rebates” on https://www.icai.org/resource _file/11288p458-460.pdf

“Rebate madness” onhttps://www.consumeraffairs.com/consumerism/rebate_madness01.html

Image credits:

alvimann on morguefile

ronnieb on morguefile

Journal entry screenshot by author