Extraordinary items require certain rules to be followed in financial accounting. It is first necessary to understand the reason why extraordinary items may be needed in various accounts. Here, we’ll take look at how to perform this accounting function.

How to Define Extraordinary Items

In order to understand closing entries in accounting for extraordinary items, it is first necessary to understand why income or expenses should be categorized as extraordinary items. Extraordinary items are income and expenses that arise from events that are distinct from the ordinary activities of the enterprise and are not likely to recur frequently in future accounting periods.

Traditionally it was necessary to show such items separately from other items in the accounts. The logic behind this treatment of extraordinary items is in the interests of consistency of presentation in the accounts from one period to another to show the users of the accounts certain income or expenses were a once-time occurrence and are unlikely to occur in the future. Users of financial statements should be aware they should pay less attention to these items when considering the ongoing financial situation of the enterprise and its likely future prospects.

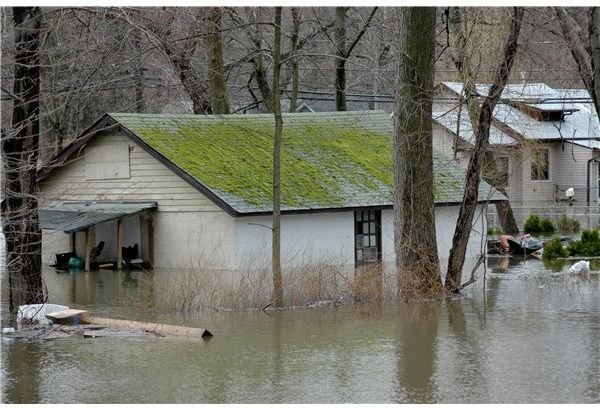

Examples of extraordinary items might include a natural disaster, a factory fire or expropriation of the assets of a branch of the company by a foreign government. There could also be extraordinary items relating to unusually high income, such as a large receipt from an insurance policy. Extraordinary items could also involve unusually high expenses resulting from irregular lawsuits or industrial action by employees. The unusual nature and the infrequent occurrence are the main distinguishing features of an extraordinary item.

The treatment of extraordinary items has been the subject of considerable discussion because problems arise in identification of extraordinary items and because many people consider there is no need for such items in basic accounts. Many accounting standards now prohibit or recommend against the inclusion of income or expenses as extraordinary items because they often confuse the position for the users of financial statements.

In any discussion of accounting, it is necessary to go back to basics and consider why items are categorized in a particular way. The presentation of items in financial statements is for the benefit of the users of the figures who wish to see the financial information presented in the most useful and accurate way. The users of the accounts include potential investors in the enterprise, employees, current shareholders, trade creditors and loan creditors. These stakeholders in the enterprise want to receive accounting information in a form that helps them draw accurate conclusions about the financial state of the business without being misled about past or future financial events. They want the information to be presented to them in a way that helps them to compare the past and present financial results and draw conclusions about the future by discerning trends from the accounting information. This objective should be considered when determining extraordinary items and the correct journal entries.

International Financial Reporting Standards

International financial reporting standards no longer require the presentation of certain information as extraordinary items in the accounts. Indeed, they state that no items should be presented as being outside the usual activities of the enterprise. The presentation of an item in the accounts should be determined by the nature of the activity rather than by its frequency of occurrence. The main problem with the presentation of some income or expenses as extraordinary items is there has to be an arbitrary selection of which items relate to the extraordinary events and which items are a part of the normal activities of the enterprise.

For example, in the event of a natural disaster such as a hurricane, which affects the activities of the enterprise for part of the accounting period and necessitates extra expense, it is not possible to accurately distinguish between those expenses that only relate to the extraordinary event and those that relate to normal activities.

The exercise of judgment in this matter is likely to be arbitrary in nature. It is better to present the expenses in their normal categories and to make the users of the accounts aware through a note in the relevant part of the financial statements that a natural disaster has affected the activities of the enterprise during the accounting period. The disaster may occur in a period when there is a normal cyclical downturn in the industry which would have had an effect on figures in the financial statements, blurring the distinction between normal and extraordinary expenses.

Classification of expenses as extraordinary items could even be used by an enterprise to improve the image of the business presented in the financial statements by classifying loss-making activities as extraordinary items while retaining profitable activities in the main body of the accounts. Far from making the picture clearer for users of the financial statements, this could give a misleading impression of the current and future financial position of the enterprise. These were the types of concerns that led to extraordinary items being forbidden by international accounting standards, though they continued to be permitted under US GAAP within certain defined limits.

Deciding on Closing Entries

It is clear the closing entries in accounting for extraordinary items are a matter of judgment and may even be regarded by some as arbitrary. A decision has to be made as to which entries in the expense accounts relate to the extraordinary event such as a natural disaster and should be shown separately under the extraordinary items heading. Adjustments for extraordinary events may be made in the year end worksheets . In the case of expenses, the accounting journal entry will be to credit the relevant expense accounts with the amounts relating to the extraordinary item, and to debit the total of these credits to an extraordinary items account. Where there is income relating to an extraordinary event, the journal entry will involve a debit to the relevant income account and a credit to extraordinary items.

The extraordinary item account will now contain the income and expenses relating to the extraordinary event, and where that event has had adverse consequences on the business, the extraordinary item will be a net expense. The closing entry then credits this extraordinary expense account and debits the income statement (profit and loss account) for the period. If the adverse event has occurred entirely in one accounting period, a nil balance on extraordinary items will be carried forward to the next accounting period. Where the adverse events affect more than one accounting period there may be prepaid expenses or accruals that are not transferred to the income account but are included as a balance on extraordinary items to carry forward to the next accounting period. These important details must be considered carefully when planning the closing entries in accounting for extraordinary items.

References

IAS Plus (Deloitte) - https://www.iasplus.com/index.htm

“Closing entries” NetMBA - https://www.netmba.com/accounting/fin/process/closing/

Image credits:

DSCF5161(2).jpg by ronnieb on morguefile

111256698931.jpg by kconnors by on morguefile