This article features a compilation of definitions for common financial analysis terms about valuations, investments & financial strategies. Financial analysis terms relate to formulas for proportions, yields & turnovers; hence understanding their meanings is necessary in interpreting the numbers.

The Importance of Understanding Financial Analysis Terms

Financial analysis terms are mostly about formulas for measuring yields, costs, and performance. However, one needs to understand the objectives and definitions of financial analysis terms in order to interpret the resulting figures, ratios, and numbers. Certain terminologies are also related to accounting for equity, income, and costing analysis. In case you can’t find something here, please refer to our other publciations about accounting word meanings in the following separate articles:

- Glossary of Basic Accounting Terms

- Accounting Definitions for Income and Expense Terminologies

- Glossary of Cost Accounting Terminologies

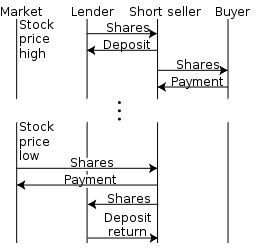

Image Courtesy of Wikimedia Commons: Short selling

Financial Analysis Terms: Beginning with A-D-F

Accounts Receivable Turnover – A method used by businesses for determining the efficiency by which their credit sales or accounts receivables are collected and converted into actual cash needed to support its operational activities.

Acid Test Ratio – It is the measurement of an entity’s liquidity by determining the proportion of its quick assets against maturing debts. The quick assets refer to the cash, marketable securities, accounts receivables and notes receivable, or those that can easily be converted into cash without taking a considerable amount time to be realized as such. This I also call the quick assets ratio.

Acid Test Ratio Formula – The formula is: Total Current Assets – Inventories / Current Liabilities

Days-to-Sell Inventory – This refers to the number of days it takes to dispose or sell goods based on inventory releases.

Debt-to-Networth Ratio – The proportion of all outstanding obligations of the company against the net assets (assets-liabilities) of the company. It’s an indication if the company has sufficient resources to pay off both creditors and stockholders in the event that a company is constrained to liquidate all its resources. An unfavorable proportion denotes a precarious financial condition for stockholders, since they are the last in the order of hierarchy during liquidation proceedings.

Debt-to-Equity Ratio – Since the basic accounting equation is Assets = Liabilities - Capital, financial analysis likewise measures the company’s stability by calculating the proportion of the company’s total indebtedness to its total capital structure. The resulting ratio derived will indicate if the company is operating mostly on borrowed funds instead of capital.

Differential Analysis – This is an analysis of the variables between two financial figures wherein the objective is to find alternative courses of action to counter any negative inferences derived from such variables.

Differential Cost – This is used in some financial analyses, as bases for determining the effects of export pricing costs or to present the viability of different markups when deciding on the selling price of a new product.

Discounted Payback Period – This analysis determines the length of time it takes to recover one’s investment at its present value. See Discounted Present Value.

Discounted Present Value – This refers to the present worth of future money that will be received in the form of several installments during a given period.

Financial Accounting – A specialization in the field of accounting which deals with the process of measuring business performance based on the financial data reported as financial statements.

Financial Analysis – A process of measuring or determining the viability of a business as a worthy investment vehicle by analyzing the numerical data presented in the financial statement reports. The objective is to determine the subject company’s profitability, liquidity, and stability.

Financial Budget – A financial plan presented in terms of financial statements, i.e. Income Statement and Balance Sheet, as a means to show how the approved budget for income and expenses will impact the net worth of the business in terms of potential growth. See Pro Forma Statement.

Financial Forecast – Financial statements that present projected income and expenses based on percent of sales and analysis of regression using financial models. Management will use them as bases for the succeeding year’s budget allocations and estimations for business borrowings, if they become necessary .

Find more financial analysis term & definitions continuing with F and also G, on the next page.

Financial Analysis Terms: F, Continued

Financial Leverage – This is the measure of a company’s ability to operate continuously as a going concern even if it resorts to borrowing long-term funds. The measure is determined by dividing the company’s total liabilities over the value of its stockholders’ equity. This denotes that borrowings are used for self-liquidating business ventures and do not affect the company’s capital growth in any way.

Financial Model – This refers to the mathematical equations used to come up with representations on how different economic situations or conditions will impact the business. It may also be used as a tool for analyzing business decisions that entail committing funds to an investment or business undertaking.

Financial Projection – See Financial Forecast

Financial Ratio – This is a mathematical tool used for determining proportions between two financial components. The numerical objective is derived by dividing the financial statement balance of one account over the balance of another financial statement account.

Financial Ratio Analysis – The interpretation of the financial ratio proportion, which depends on the analyst’s objective in terms of profitability, liquidity, or stability.

Financial Reporting – The required financial statements submitted by business entities, for review or perusal by regulatory bodies, public investors, creditors, employees, and all others who may have vested interests in a business entity.

Financial Risk – The connotation of risk means the probability of negative outcomes for a financial venture such as investments, or the amount of money lent or any form of undertaking from which yields are generally expected.

Fixed Asset Turnover – This refers to a measure of profitability by determining how effectively the fixed assets are being utilized to generate revenues for the business. This is determined by dividing net sales (sales - discounts/refunds) over the value of fixed assets.

Fixed Asset Unit – Refers to every single item classified as a tangible asset capitalized as a fixed asset cost. Examples include machinery, delivery equipment, office furniture, computers, and the like.

Fixed Asset-to-Equity Capital Ratio – The ratio is looked into by investors who are interested in determining how much of the capital has been infused in fixed assets that are used for business operations. It indicates if management is harnessing capital funds on resources for the purpose by which the company operates and not on speculative investments.

Fixed Budget – The predetermined plan that has been resolved as non-adjustable regardless if there are any deviations in the conditions that affect a company’s ability to realize the income that was projected.

Flotation Cost – This is defined as the monetary considerations involved in the issuance of a new security. This pertains not only to the administrative expenses paid in order for the new security to have a physical presence in the capital market but also the yield that will be paid out to investors who will buy the newly released investment product.

Gross Margin – This refers to the difference between the selling price of the goods and the actual cost of the goods being sold; simply put, it’s the price mark-up quantified by the number of goods sold.

Gross Margin Pricing – An approach to selling price-calculation by adding mark-ups based on a percentage of the product’s total cost.

Gross Margin Ratio – The measure of proportion between the remaining sales revenue or gross profit (Sales – Cost of Goods Sold) to the total sales revenues. A favorable proportion indicates that the goods are selling at competitive mark-up prices.

Gross Price Method – This is a method of determining selling price mark-up by basing the percentage on the invoiced amount of the cost of goods sold, ignoring any cash discounts.

Gross Profit Margin – The difference between the sales revenues and the cost of goods sold; as a profit margin, this denotes the limit by which operating expenses are to be incurred to ensure profit realization.

Growth Rate – This is the percentage by which the results of the business operations have improved, achieved by making a comparative analysis of the company’s annual common-size financial statements . See Horizontal Analysis.

Financial analysis terms & definitions beginning with H-I-L-M are found on the next page.

Financial Analysis Terms Beginning with H-I-L-M

Hedge Fund – This refers to a more sophisticated type of mutual fund, where high-minimum investment resources are pooled into a single investment undertaking but are restricted to no more than 100 investors for each pool or fund. In addition, hedge funds are subject to fewer restrictions, which allows the hedge fund managers to place the pooled funds in more aggressive forms of investment strategies like short-selling, swaps, leverage-buyouts and arbitrage (simultaneous buying and selling of securities in capital markets). This is usually available to the more affluent investors or to well-established institutions, since the minimum placement per hedge fund may range from $250,000 to $1 million.

Horizontal Analysis – This is a form of comparative financial statement in which the measure of changes for at least three years are presented and expressed in terms of percentage. Some horizontal analyses make use of the first year as the basis for presenting the changes throughout the three-year period to denote growth, let’s say from inception to date. Others, however, present changes from year to year; hence the base year used would be the previous year and the growth or regression presented is from previous year to the current year.

Hurdle Rate – The rate of return by which an investment will yield profits as necessary data for a cash flow analysis .

Industry Standards - These are otherwise known as benchmarks as they represent the study of track records of performances among successful businesses in their respective industries. They provide the figures against which small business’s financial data can be compared.

Inventory Turnover – This financial ratio determines the number of times that a company’s inventory is sold and restocked by dividing the total sales over the average inventory. A high rate of turnover would mean efficiency in selling and restocking of goods. However, the results should be proportionate to the cost of goods sold.

Investing Activities – Refers to a company’s use of capital funds by way of purchasing and/or selling additional assets with potentials to yield profits as a means to achieve financial growth. Examples of capital fund investments include new machinery, new products, branching out, diversifying into new product lines, and marketable securities if the capital funds being invested are idle funds.

Leverage – See Financial Leverage

Leveraged Buyout – This is a type of high-end financing usually resorted to by companies, whose need for funds is basically for survival purposes. In such cases, a company agrees to put up its assets as collateral for a substantial loan amount. However, others see this as a form of predatory lending because the borrowing company will be made to pay exorbitant amounts of interest, hence making it impossible for the distressed company to pay off the loan Accordingly, the actual objective of the lending group is not to help out the distressed entity but to buy out the company without the need to assume its other debts or obligations, by simply foreclosing the assets.

Managed Earnings – This refers to a company of which the earnings and expenditures are manipulated as a means to project financial growth. Its management makes use of business projections as bases for financial presentation manipulations and not as the bases for budget allocations. Find a related article entitled A Detailed Look at the Enron Scandal about fraudulent manipulations that present a classic example of managed earnings.

Marginal Analysis – A type of analysis that delves into the costs of different alternative investment undertakings and the benefits or yield that will be derived from such costs by studying the growth effect on the revenues and expenditures of the investing company. Investment decisions will be made based on the study of the factors that spur the financial growth and which factors have the likeliest possibility of bringing in more marginal profits within an established safety level.

Margin of Safety – This refers to the established safety level used for investment decisions based on marginal analysis. It is derived by calculating the company’s breakeven point and then extracting the figures from actual sales. The excess amount is considered as the margin of safety; and the higher the excess of actual sales against breakeven point, the higher the level of margin of safety presented.

More financial analysis terms & definitions continuing with M and also N are on the next page.

Financial Analysis Terms: M, Continued, and N

Marginal Cost – This represents the cost of an investment undertaking wherein direct costs plus fixed operating expenses have been considered as those that can be absorbed at the break-even point. The marginal costs then are computed from break-even point level plus the variable costs.

Markdown – A business strategy that entails the reduction of a product’s selling price to stimulate buying activities from customers and attract more consumers.

Markup – This represents the amount added to the invoice price of the goods purchased in order to come up with the selling price.

Market Value – The price that willing buyers would pay for a commodity if put up for sale in the market.

Money Market – Refers to the capital market where securities such as shares of stocks, short-term debts, and bonds are traded. The money placed in short-term debts is called money market placements.

Mutual Fund – This is the term used to describe money that has been pooled by an investment company coming from several investors in order to build an investment fund that has the ability to generate higher-yields by taking advantage of the substantiality of the amount. Any income earned from a mutual fund shall be distributed among the investors according to the proportion of their monetary contribution to the pooled funds after deducting the fees of the investment company.

NASDAQ – The acronym stands for National Association of Securities Dealers Automated Quotation System but has outlived the meaning of its foundations as a securities trading place using the first electronic screen-based equity securities listing that could be traded over the counter. It has evolved into a licensed national exchange as a component of the capital market.

Negotiated Price – This refers to the price mutually agreed upon by both seller and supplier after agreeing on certain conditions that may be demanded or rejected by any or both parties, in which negotiations may include price reduction as a means to extract compliance or price increment as a condition that would compensate for the exclusion of a condition.

Negotiated Transfer Price – This is a form of managerial accounting in a company in which the management of costs and income are decentralized in each division. In this situation, each division is given the right to trade its supplies or services with other divisions at a negotiated transfer price, inasmuch as selling price does not apply where there is no actual selling activity taking place. This then will allow each division to optimize its resources by generating internal profits that would enhance its financial performance within the organizational set-up.

Net Cash Inflow – The excess amount of the actual cash received from business operations after all the necessary operating expenses have been met. This analysis is commonly used by a company that resorts to fund borrowing and is into monitoring if the additional funds invested in a new project are generating enough cash to pay off the related debt incurred.

New York Stock Exchange – Considered the leading stock exchange center for having evolved into NYSE Euronext. NYSE’s merger with several major capital markets operating in Europe is considered the largest combination of global resources to create the most liquid global marketplace for stock exchanges.

Non-Controllable Risk –The risk instigated by forces or influences from external sources which are beyond the company’s control. A psychological response to a product as a reaction to a past negative incident is an example of non-controllable risk.

Non-Public Company – A company that does not trade its shares of stock in the trading floors of the capital market.

Number of Days Inventory is Held – Refers to the calculation of the average number of days that an item is held as inventory in order to determine the opportunity cost incurred while in its inventory state. It follows that the more days a stock inventory is held on hand, the more unfavorable its implications, since the days will be converted into its equivalent opportunity cost or the revenue lost.

Find more definitions for financial analysis terms & definitions beginning with O-P on the next page.

Financial Analysis Terms Beginning with O-P

Opportunity Cost – The yield of an investment alternative; or an opportunity to generate income that is foregone by taking a different course of action or by deciding on a different alternative.

Open Market – A trading condition during which sellers and buyers exchange goods and services for monetary considerations based on the impact of supply and demand; as opposed to a closed market where there are restrictions to observe before a seller or buyer can actively participate.

Open Investment Company – This is also known as Open-Ended Investment Company (OEIC) where the investors are allowed to pool their investment funds and place them in different types of investment securities. A shareholder who wishes to sell his share in the pooled funds will base his selling price on the value of the OEIC’s net portfolio value per share. In the US, this type of company is popularly referred to as open-ended mutual funds .

Penny Stock – These are the shares of stocks that are traded over the counter by way of Over-the-Counter-Bulletin Boards and pink trading sheets. They do not participate in the major capital market because of their relatively low price, which can even be lower than a dollar. Investments on penny stocks are considered highly speculative because the company’s capital funds are basically dependent on investors’ contributions.

Period of Redemption – In financial investments, this refers to the specific period or date on which the investor may collect the amount of money invested as a bond or to technically collect a debt.

Price Index – This is the short term for Consumer Price Index or the weighted average of the consumer’s costs or prices paid for basic necessities, like food, medical care, rent, etc. The weight given to their value is according to their degree of importance, and any changes for individual items will be considered and a new weighted average will be computed. Based on this, the CPI is the price value used for computing the cost of living in a given sector.

Prime Rate – This refers to the interest rate extended by the bank to its prime borrowers or those who are considered credit-worthy. The latter are usually large corporations who are into self-liquidating ventures; hence the money exposed to lending risks is extended to the prime borrower at lower rates of interest. This can also be the default rate for small borrowers who have relatively the same qualities as the prime borrowers.

Pro Forma Statement – A form of financial statement used for business projections to illustrate earnings and growth potential in terms of assets, liabilities, income, and expenses. Start-up companies are encouraged to use pro-forma statements in order to have a visual projection of their business plans and as a medium for pinpointing the areas that may be hampering their business’s growth.

Prospecting – In financial investments, a reference to prospecting is basically applied to junk bonds or securities that have a relatively high degree of risks but with high-yields. Decisions on the securities to prospect on are usually made after careful analysis indicates that there are greater probabilities that the investment will pay-off.

PS Ratio – This is the short term for Price to Sales Ratio, which is the measure of a company’s performance that is based on the actual sales generated by the company ; hence the earnings per share are based on the sales revenue instead of the net income. This is based on the premise that a company will find it more difficult to manipulate the gross sales figures that are free of any deductions.

Find more financial analysis terms & definitions, continuing with P and also R-S on the next page.

Financial Analysis Terms: P, Continued

Public Offering – The act of presenting a company’s shares of stock and other investment instruments to the capital market with the understanding that the money being solicited will be used by the offering company for additional business ventures or expansion projects that are expected to have high yields of return on the investors’ placement.

Portfolio – This is the entire assortment of investment instruments and undertakings of an organization, entity, or individual that comprises diverse investment strategies as a means for limiting the risks being taken.

Preferred Shares of Stock – A company’s shares of stock to which the holders are given the privilege of earning higher yields and of having higher priority in terms of dividend payouts. Preferred shareholders are also ahead in the order of hierachy for claiming rights to the company’s assets if compared to the common stockholders

Ratio – A measure of the relationship between two quantities usually derived as a quotient of a mathematical equation and interpreted as the direct proportion or size of one aspect to another, but not with the intention to interpret the quotient as a fractional part.

Sales Forecast – This is generally construed as a prediction of future sales based on the figures of historical performances on how past sales were generated. In making forecasts, the analyst carefully considers the variables that contributed to their increases and decreases.

Security/Securities – These are documents that serve as proof of stakes or claim as part owner of a business corporation, in proportion to the number of securities he holds. In addition, these documents are likewise proofs of entitlement to dividend payouts.

Self-Liquidating – A project or venture is considered as self-liquidating if it will yield funds that the business can use in carrying out its business activities, including the potential to pay off the funds borrowed to finance said projects. In such cases, the recovery of the amount invested is realized at the soonest time possible.

Short Sell – To short sell in financial activities is to sell shares of stocks at a lower price than the stocks are worth. They are securities that one borrows from a stockholder’s portfolio or that of another investor. If the price of the stocks drops in the process, that will be the chance to buy back the stocks. Buying back the short-sold stocks at an even lower price gives the speculator a good chance to profit. Once the stock’s price rises above the amount of one’s short-selling strategy, he can then sell the stock but this time at a higher price than the buy-back or short-sell price. The proceeds cover the amount that has to be returned to the broker while the difference is the short-seller’s gain.

Sensitivity Analysis – This is a method of analyzing the responses, reactions, and impact of variables if they occur under a different set of conditions.

Short-Term – A business venture, undertaking, placement, or loan-out is said to be short-term if the period is for one year or less.

More definitions for financial analysis terms & definitions continuing with S plus T-U-V are in the final page of this article.

Financial Analysis Terms: S, Continued (Final Page)

Simulation – A simulation in financial analysis is a business model structured by mathematical computations wherein the conditions calculated will produce expected variables. The analyst runs a simulation by inputting different projected data in order to establish the effects presented by each forecast. The results will serve as the analyst’s basis for comparisons regarding the different degrees of risk presented by each business projection or proposal.

Slack – This term refers to regression or slowing down of the activities being analyzed.

Speculation – This refers to an undertaking that does not present a comfortable degree of safety and which requires greater attention to the analyses of its probabilities.

Spoilage – This refers to wastes, scraps, or the cost of errors that stem from mishandlings and are not considered part of the standard’s allowance for such.

Spreadsheet Analysis – This refers to the use of electronically generated worksheets or formats that contain rows and columns where data can be analyzed with expediency by imputing formulas in each relevant cell. The use of the formula functions will automatically generate answers to mathematical calculations with a greater degree of accuracy.

Statistics – The branch of mathematical science that deals with data collections, selection, analysis, and explanation for the numerical data calculated in order to come up with presumptions or projections about their probabilities.

Time Value of Money – This refers to the calculation of how much present money will be worth by computing the yields it is expected to earn if placed in a particular money placement or investment for a particular period. This can be derived by compounding the balances as…

Turnover Ratio – This refers to the number of times that a particular component will undergo changes to indicate that the business is taking a positive course of direction as far as profitable operations are concerned.

Variance – The state of being different from the standard or the norm; the latter’s occurrence takes place under normal conditions without any influencing factors that can affect the pattern of its occurrences.

Vertical Analysis – This is a type of common-size financial statement presentation that shows a percentage analysis of each account in relation to the net income. Beginning from the Cash account of the Balance Sheet Statement and going vertically down to the Stockholders’ Equity account, the respective balances are divided by the base amount in order to derive their proportion to the net income generated.