The context of accounting irregularities is broad, which includes unintentional errors that result in immaterial effects. This article provides explanations as answer to a more specific question: “What are accounting/audit irregularities in financial statement fraud?” Read on to find out.

Statements on Auditing Standards (SAS): Definition of Accounting Irregularities

What are accounting/audit irregularities and why do they create a tremendous impact in stock market trading? Are accounting irregularities the same as fraudulent financial reporting practices?

Basically, SAS No. 53 defines accounting irregularities as “intentional misstatements or omissions of amounts or disclosures in financial statements.” Accordingly, a mere violation of the generally accepted accounting principles (GAAP) , is considered as an irregularity because it denotes a breakdown of the elemental foundation of a sound accounting system.

What Factors Characterize Accounting Irregularities as Fraudulent?

During audit examinations and prior to the formal submissions of financial reports, deviations from GAAP rules may be discovered and initially judged as unintentional errors. As a matter of procedure those errors are corrected or adjusted before the financial statements merit any professional certifications.

Audit reports and certifications that accompany the statements are significant, since they attest to the veracity of the financial data. They likewise serve as endorsements of a business entity’s financial conditions and the results of its operations–that the statements embody fair and accurate presentations.

If such deviations from GAAP rules are used to support financial reports that were professionally certified as GAAP compliant but in truth largely violated the GAAP rules, then the deviations are considered accounting irregularities, inasmuch as they intend to mislead those who make use of said statements as a basis for investment decisions.

As a rule, however, accounting irregularities have to be administratively proven by civil or criminal proceedings, such as those brought to court by the SEC or the IRS, before they are adjudged fraudulent accounting manipulations used for financial misrepresentation.

The Impact of Accounting / Audit Irregularities

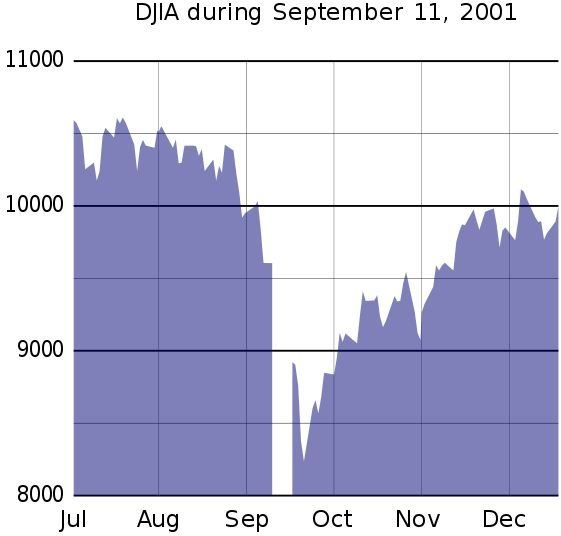

The tumultuous stock market events that resulted from the 2001-2002 spate of accounting scandals have since then caused investors to react strongly to issues associated with orders for financial restatements. These are issued by the SEC due to evidence of accounting irregularities in publicly traded companies.

Based on COSO’s (Committee of Sponsoring Organizations of the Treadway Commission) report for 2010, accounting irregularities that were later proven as fraudulent financial reporting practices continued to exist up to 2007. The magnitude of their impact consequentially brought the American economy to a downturn, as companies went into bankruptcies while the number of unemployed increased.

Hence the importance of understanding the essence of accounting irregularities extend not only to investors but to employees as well, inasmuch as inside information can help alleviate the impact of accounting manipulations used as tools for misleading the public.

Accounting/Audit Irregularities Defined

After delving into fraudulent characteristics and their impact, we can now provide an answer to the question “What are accounting/audit irregularities in financial statement fraud?”

Accounting irregularities are acts committed in a concerted and organized accounting system that deviate from the generally accepted accounting principles, in order to create a financial illusion of a business entity that has the capacity and capability to sell more and at lower cost than their competitors. The illusion is further sustained by creating an image of a company that owns more resources to support its profitable operations as it aims to project an enhanced credit worthiness and eligibility for substantial borrowing.

The manipulation of accounting records to show profit where there is none and to classify expenses as assets, as a means to cover-up debts and losses, fabricates an image of a highly profitable company with a favorable debt-to-equity portfolio.

Who Benefits from Accounting Irregularities in Financial Statement Frauds?

Of the 1,335 public companies identified by the Securities and Exchange Commissions (SEC) in its Accounting and Auditing Enforcement Release (AAER), one thousand seventeen (1,017) were directly linked to fraud cases and 347 were subjected to analysis in the COSO report.

It was disclosed that 21% of the Chief Executive Officers (CEOs) involved in the accounting irregularities proven as financial statement frauds were indicted, and that 64% of those indicted were convicted. On the other hand, only 17% of the Chief Financial Officers (CFOs) were indicted, of which 75% were actually convicted.

In our compilation of overviews about the ten major accounting scandals , in a separate article bearing the same title, most CFOs eventually turned state witness and were incarcerated for lesser terms than their CEOs.

The rationale behind this is that the CEO benefit the most from fraudulent financial reporting. As those at the highest level among the senior executives, they stand to gain substantially by way of profit shares and bonuses in accordance with their compensation arrangements. Hence, their interests are directly linked to financial statement measurements in terms of revenue generation, which clearly define their motives in collaborating with their CFOs to commit accounting irregularities. Another article, " A Detailed Look at the Enron Accounting Scanda l," reveals how the company’s CEO, Kenneth Lay, gained from all the accounting manipulations.

The investors and employees are at the losing end. However, regulating bodies deem that the latter are in better positions to prevent substantial economic losses by blowing the whistle on their company bosses.

The Sarbanes Oxley Act (SOX) Section 806 – Whistleblower Protection

Sec. 1514A of the SOX Act provides whistleblower protection for employees of publicly traded companies by prohibiting the company, its officers, employees, contractors or subcontractors, or its agents to demote, suspend, threaten, harass, or discriminate against an employee because of any action taken by the latter to provide information that may lead to investigations or assist in the ensuing investigations pertaining to a violation of the SOX Act or any rules or regulations of the SEC, or of any federal law for frauds committed against shareholders.

The accounting system was basically designed with standard procedures and methodologies that provide built-in checks and balances against errors. However, the difficulty in their discovery is often aided by the element of connivance to cover-up those that have been intentionally committed in order to perpetuate fraud.

Based on COSO’s 2010 report, the implementation of the SOX Act in 2002 did not create the expected impact. Despite the increased responsibility and liability of a public company’s key officers in ensuring the accuracy and veracity of financial statement reports, fraudulent financial reporting were still prevalent through 2007. Hence the whistleblower protection clause was inserted to encourage employees in taking direct and immediate action by providing insider information, or even causing to provide information, that may lead to the curtailment of white-collar fraud.

If in doubt as to what are accounting/audit irregularities, and to determine whether they are intended to perpetuate fraudulent financial misrepresentation, its definition and characteristics will serve as guides.

Reference Materials and Image Credits

References:

- Fraudulent Financial Reporting 1998-2007 An Ananlysis of US Public Companies by Mark S. Beasley, Joseph V. Carcello, Dana R. Hermanson, and Terry L. Neal — https://www.coso.org/documents/COSOFRAUDSTUDY2010.pdf

- SOX-online: The Vendor-Neutral Sarbanes-Oxley Site Sarbanes-Oxley Act Section 806:Whistleblower Protection – https://www.sox-online.com/act _section_806.html

Image Credits: