Capitalization policies for fixed assets of a corporation are essential for a company’s property acquisition, management & disposition. They provide a set of guidelines that ensure consistency & uniformity in accounting for the company’s fixed assets, deemed necessary for fair & accurate reporting.

The Importance of Fixed Assets Capitalization Policies

A set of capitalization policies for fixed assets in a business organization is important in order to maintain consistency in the valuation treatment and control of all assets acquired through all the years of its operation as a going concern.

-

Creating a set of policies in accordance with the applicable capitalization rules and regulations prescribed by the Internal Revenue Service (IRS) and the Securities and Exchange Commission (SEC), can lessen the occurrence of non-conformity to accounting and reportorial requirements.

Advertisement -

It also ensures uniform compliance by the entire business organization to all procurement, capitalization, depreciation, and disposition rules in a specific business industry, for purposes of safeguarding the company’s physical assets.

-

In fact, the Sarbanes Oxley Act’s broad 404 conditions require all companies to include in their reports a statement issued by the company’s management that all internal controls, IT processes, and underlying systems are entirely in accordance with the generally accepted accounting principles and standards.

Advertisement

This therefore involves the review and tests of the fixed assets capitalization policies , as conducted by both internal and external auditors through their respective audit examinations. Any adverse results should have been properly addressed and included as a disclosure, if they materially affect the financial condition of the company.

Overviews of the Capitalization Policies for Fixed Assets

The entire set of the company’s fixed asset policies should be assigned with a clear and specific title to denote the purpose for which the policies were created. The aim is to immediately impress in the minds of the user the main intent of the policies – do they present guidelines for adherence, or are they basic standards considered for business projections?

1. As an introduction to the body of the policies, there should be a clear statement that the set of policies aim to achieve uniformity on the accounting and management of the fixed assets of the company . This includes the ultimate goal of ensuring that the financial reports are supported by accurate records, assigned with values determined on the basis of generally accepted accounting principles and procedures.

2. Part of the capitalization guidelines should include a clear definition about the concept of fixed assets and how they exist in the company’s entire environment as tools or implements for business operations.

3. If possible, a list of the business’s known and existing fixed assets that are covered by the policies is incorporated.

4. There should be clear and concise statements about capitalization guidelines by stating the following:

-

The acquisition, construction, or development values or costs as bases for capitalizing the fixed asset;

Advertisement -

The number of future years’ benefits that can be expected from a particular equipment or fixture; and,

-

That the asset being considered is definitely not for the purpose of resale or part of the company’s merchandise inventory but will be used in carrying out the business’s operations.

Advertisement

5. The applicable methods of depreciation on how a particular fixed asset is depreciated should likewise be specified. The method should also state the residual life to be deducted from the asset’s estimated useful life, for purposes of computing the amounts of depreciation.

6. In determining the depreciation of the fixed asset, the set of policies should provide the following as considerations for calculations:

-

The exact description of the asset to be depreciated ;

Advertisement -

The amount expected as residual value or book value or scrap value of the asset; and

-

The estimated useful life of the asset.

Advertisement

7. Other costs related to acquisition, construction, or development of the asset, i.e. shipping, storage, licensing, interests, and other similar expenditures should have definite policies on how they should be treated, whether as part of the acquisition cost or as outright expenses.

8. Some assets like computer equipment comprise components and peripherals in order to make the asset operational. Varying acquisition costs are involved and thus technically present the overall acquisition value of the asset. Hence there should be specific guidelines as to which component or peripheral shall be capitalized or treated as outright costs.

9. The same considerations shall be made for buildings and each building’s service components, although this aspect should focus on how the components shall be depreciated, whether as intangible fixed assets or as part of the building’s construction costs. It would be best practice to have a separate chart of estimated useful life for the building and building service components, according to what actually exists in the company’s premises.

10. Defining the capitalization and depreciation of improvements on leasehold is also important, in case the company is operating in a leased property.

12. Repairs, renovations, and overhauls must be clearly distinguished as to when such expenses are capitalizable, in order to preserve the consistency by which the assets are valued.

13. Policies to establsih the procedures by which obsolete and retirable assets are determined should state who determines if the assets are due for retirement, the procedural actions involved from point of determination, to point of final asset disposition. The rules and the designation of authorized personnel must be clearly stated to avoid the misuse or abuse of this particular procedure.

These are the main areas of consideration when developing and creating capitalization policies for fixed assets for a business organization. Readers will find a related article, entitled: Example of Corporate Capitalization Policy for Fixed Assets, in which they can find a link to a free downloadable template for fixed assets capitalization policies.

Reference Materials and Image Credit Section:

References:

- Internal Revenue Code Sec. 1.263A-1 Uniform capitalization of costs – https://www.timbertax.org/research/regulations/26cfr1.263A-1/

- Administrative Accounting Section 6. Property and Equipment Accounting – https://www.irs.gov/irm/part1/irm _01-035-006.html

- Wiley GAAP for Government 2010 – https://books.google.com.ph/books?id=A-pGy2dwUiIC&pg=PA281&lpg=PA281&dq=The+significance+of+having+a+set+of+Fixed+Assets+Capitalization+Policies&source=bl&ots=J0a7dCfQLo&sig=sT1WNnOWgcgCVFg6q6DI-BuuQ6M&hl=en&ei=qqIOTbz5OIm3cImtqcoK&sa=X&oi=book _result&ct=result&resnum=8&ved=0CEYQ6AEwBw#v=onepage&q&f=false

Image Credits:

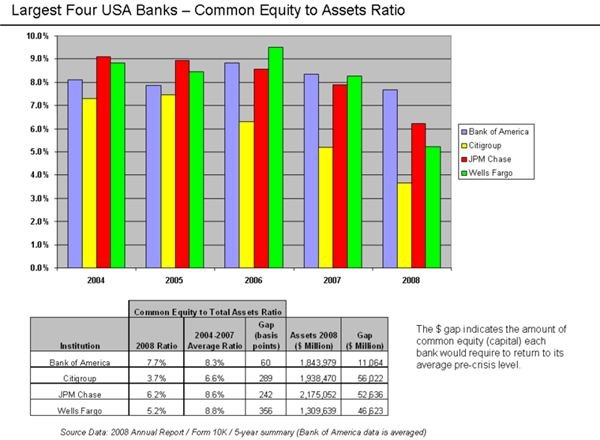

- [Bank Common Equity to Assets Ratios 2004 - 2008.png](https://commons.wikimedia.org/wiki/File:Bank_Common_Equity_to_Assets_Ratios_2004_-_2008 . png)

- Gold seal for official policy (v4)

- Computer-aj aj ashton 01