Essentially, for any new venture, the venture capital investing process is all about minimizing risks and maximizing rewards. This investing process is discussed in this article from the entrance stage to the exit stage.

Venture capitalists play the role as an important financial intermediary by providing capital to firms that might otherwise experience difficulties in attracting funds from pre-inception to post operations. Subject to other things being equal, firms seeking venture capitalist backing are generally small but typically young and high risk oriented because of their possessing inadequate. New firms usually have little or no tangible assets and are characterized by a knowledge gap between what the entrepreneurs and investors know about each other. A natural corollary of this, venture capitalists finance in real terms, and seek high risk oriented projects that have a potential for big rewards. The mode of finance usually involves the purchase of equity or equity linked stakes from such privately held firms. In order to minimize the risk and maximize the rewards, the venture capital industry has developed a variety of mechanisms , which in other words, can be stated as the venture capital investing processes.

Investment Pattern

There are no universally defined and accepted rules relating to the investing process of venture capitalists and they can at times, be even arbitrary. Within these limitations, what one can do, is to discern a pattern in them which are key to obtaining venture capital investment interest. The first process is to seek an investment which provide funds even before a company starts functioning. Such investments are based on a single individual who combines both the idea and expertise but does not possess enough capital and a venture capitalist steps in to bridge this gap.

This is followed by a start up investment stage , which concurs with the functioning of the company, but before revenues are generated. Then comes the early growth phase that corresponds to the period wherein revenues start coming in but they are not enough to become a major source of finance to sustain operations. This leads to follow on or what the industry terms as the “mezzanine” stage, wherein the venture capital firm steps in to enable sustainment of the operations. When the firm matures, the final stage emerges which involves the turning around of the investments and leveraged buy outs.

Time

There is again no hard and fast rule on timelines in the venture capitalist investing process. With each process, in a normal scenario, the first three stages are covered within a period of one year. The intermediary processes involve anywhere from two or more years. The special purpose investments is of the nature of a one-time financing that is made anytime after the previously mentioned processes are completed.

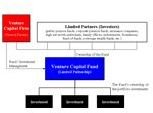

Visualization

While it may be concluded that such processes can be visualized as a cycle that consists of a primary function of raising capital, the intermediary process of monitoring cash flows, and then followed by a process of exit. It should be noted the actual factors that weigh in the decision-making process of venture capital firms are not that simple. Though the scope of this article does not permit to deal each one of them, one important aspect that needs mentioning is that most of the firms receive venture funding from more than one firm, which is known as a “syndication process.” Venture capitalists take into account a number of propositions before taking a decision either to accept or reject outright a project or to seek a syndication if the prospects fall somewhere between acceptance and rejection.

Image Credit: Venture Capital Fund Diagram - https://commons.wikimedia.org/wiki/File:Venture _Capital_Fund_Diagram.png