Do Subchapter S Corporations have retained earnings? Ask a CPA how to calculate S corp retained earnings and they’ll probably look at you funny and say, “Do you mean your Accumulated Adjustments Account or AAA?" Jean Scheid, owner of an S Corporation explains retained earnings in an S Corp.

Does an S Corp Have Retained Earnings?

The answer to this is yes and no. If you’re already confused, it’s best to understand first what an S corporation is and how it is taxed. S or Subchapter S Corporations are pass- through entities where stockholders receive a K-1 statement showing the company’s profit (or loss) once adjustments are made to the AAA account. Each shareholder’s K-1 is then used as part of calculating his or her personal tax return and the S Corporation is not taxed. If you’re still confused, skip a regular balance sheet that would have owner equity accounts like this:

- Common Stock

- Additional Paid-in-Capital

- Retained Earnings

- Current Year Profit (or Loss)

In an S Corporation, the Additional Paid-in-Capital and Retained Earnings accounts are removed so you end up with:

- Common Stock

- Accumulated Adjustments Account

- Current Year Profit (or Loss)

Retained Earnings Versus the Accumulated Adjustments Account

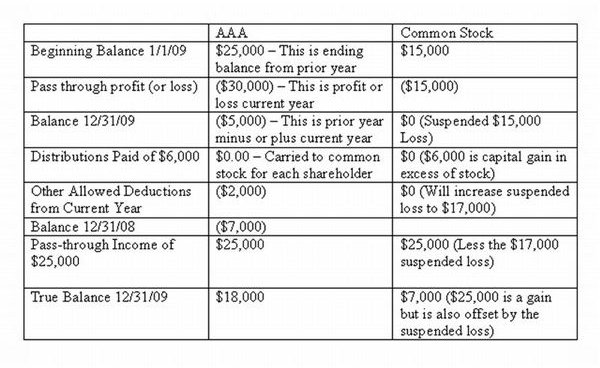

If we look a very basic S Corp owner’s equity including both the Common Stock and the AAA, it would look something like the diagram here. In order for you to understand all the elements of this diagram, before you continue reading, please download the Retained Earnings Chart from our Media Gallery.

Now that you’ve printed out your Retained Earning Chart example and have it in front of you, always keep in mind that the AAA account should be treated as you would your checking balance register . The AAA account simply keeps track of profits, losses and equal dividends paid to all shareholders. The Common Stock only measures each stockholder’s equity in the business. To find out if you will pay tax with an S Corporation, which will be passed to your K-1 for your personal tax return, the ending balance (profit or loss) of the AAA account is taxable to all shareholders based on percentage of stock owned. Here the $18,000 would be the profit of the S Corp and the common stock would be calculated at $7,000 plus the suspended $25,000 for a beginning balance for the new tax year of $30,000.

Because the $25,000 gain is offset by the $17,000 suspended loss, the pass-through S Corporation income is $18,000, which is split between each shareholder. When the next accounting year begins, say, January 1, 2010, the AAA account will sit at $18,000 and the Common Stock will be $30,000. Adjustments to common stock can also be made via cash contributions by any stockholder or equipment with a purchase price according to IRS guidelines for an S corporation that are allowed deemed as capital contributions.

Summing Up S Corporations and Retained Earnings

While the example here is very basic, it should give you an idea how the AAA account works and how the Common Stock is affected. If this example were in more detail and had numerous columns for various stockholders in the S Corp, cash or capital contributions would make the common stock for each shareholder rise or fall depending upon which stockholder made the capital contributions, however everything passes through the AAA account.

In an S Corporations, unlike LLCs or C Corporations , any dividends taken must be equal, but distributions are based on how much stock each shareholder owns. For example, where our template states distributions were $6,000, if one shareholder owned 30% stock and one owned 70% of company stock, the 70% stockholder would receive $4,200 and the 30% stockholder would receive $1,800. Distributions and dividends in an S Corp are two different things.

The ending balance or profit or loss in our example of $18,000 is what can be considered “retained earnings” and what is taxable to each shareholder. It is also the amount that will be carried over as the beginning balance for the new tax year.

Because Subchapter S Corporations have enormously difficult tax laws that change each year, it’s best to ask your CPA how to calculate retained earnings for an S Corp so you don’t make any errors on your 1120S tax return.