If trade credits are great, then why do businesses fail to meet their obligations? Credit arrangements are supposed to bring benefits to an entrepreneur; then something must be amiss if a business entity finds itself falling into a credit trap instead. Explore the credit concept through this article

Understanding the Implications of Borrowing

A supplier’s credit gives the entrepreneur the benefit of short-term borrowing sans the rigid requirements imposed by financial institutions. If a business owner applies for a bank-financed loan, he will be asked to pay processing fees and submit different documentation just to show proof that he has the capacity to pay.

Thereafter, the loan if approved and granted will bring funds that cost more than their actual face value, with interest added. If the borrowed money will be used as additional working capital for inventory purchases and other operational expenses, the actual costs incurred would be more than the COD price. As a result, the borrower-entrepreneur will be constrained to pass on the costs of money to his customers by increasing the selling price of his goods. This of course would make the borrower’s business less competitive or less profitable.

This stands opposed to the concept of trade credit, in which payment is deferred without being burdened by onerous interest and processing fees. If the business owner manages his cashflow and his inventory level well, he can even realize a reduction or discount of the actual amount that was technically loaned out to him.

Typically, suppliers offer incentives for early payment of credit purchases, let’s say 2/10-30, being the most common. This denotes that if the purchaser on credit pays his obligation within ten days of a 30-day credit term, a two percent discount or reduction of liability will further reduce his costs.

As a competing entrepreneur, he can likewise reduce his selling price by two percent in order to increase customer patronage. If goods purchased on credit have a high rate of inventory turnover, both the supplier and credit purchaser will enjoy the benefits of a positive cash flow.

However, the key factor to its efficiency is not just the trade credit, but the orchestration of several business management disciplines, i.e.:

- Development of business projections or forecasts that are sensible and workable;

- Maintaining appropriate levels of inventory;

- Preserving good business relationships with both customers and suppliers;

- Choosing the best financing options and services;

- Effective management of working capital and cashflow;

- Accurate and timely recordkeeping.

To give further emphasis, study the case sample below as it illustrates in part how a business can benefit from trade credit by managing its cost.

Case Study

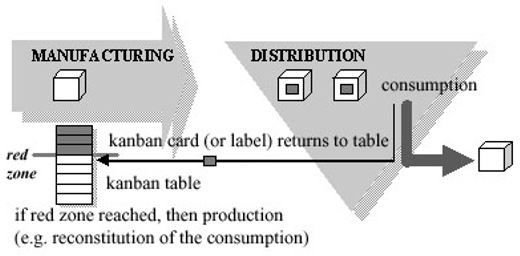

This case study advocates the use of the “just-in-time” or “kanban” method of managing inventory level along with the “rolling forecast method” of managing the cash flow. The objective is to keep the facts and figures closer to what is actually and currently taking place in the entity’s own business scene.

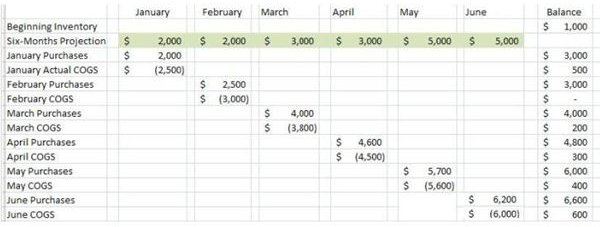

Using the following forecast data , we will quantify the benefits realized if the terms 2/10-30 will be observed in its purchasing activities for the first six months:

- January - $2,000

- February - $2,000

- March - $3,000

- April - $3,000

- May - $5,000

- June - $5,000

Total Projected Purchases for the first six months = $20,000

Assuming that all purchases were made on credit from a single supplier and all obligations were settled within ten days. The estimated savings during the six-month period from a single credit supplier would be $400 ($20,000 X 2%).

To appreciate this amount, let us presume further that the two percent trade credit discount was used to offer a promotional reduction of the entity’s selling price. The business is likely to pick up since the marketing strategy will tap into the customers’ natural attraction to promotional discounts.

In carrying on with the presumption, the $20,000 worth of goods are all sold at a promotional 18% price mark-up instead of the regular 20%. This denotes that the company’s gross profit by the sixth month will be $3,600 ($20,000 X 18%). The total value of the benefits derived from the $20,000 credit purchase would be the $3,600 gross profit plus the $400 savings or a total of $4,000. Take note that it is equivalent to the gross profit that would have been generated at the regular mark-up of 20% ($20,000 x 20% = $4,000).

The primary objective, however, is to create an advantage over the competitors who are also in the business of selling the same products or be competitive with those who can afford to sell the same product at reduced prices.

Forecasting Using the Just-in-Time Method and Rolling Forecast Technique

If a business aims to increase customer patronage, due consideration should be taken to prevent over or under projections of inventory level. These are two scenarios which should be avoided, since they are often the pitfalls of most entrepreneurs once their nouveau businesses start picking up:

-

Overstocking of goods– as this will tie up the cash funds for a longer period over the short-term of the trade credit.

Advertisement -

Understocking of goods – because the inability to meet demands not only creates a negative impression on the part of the customer but also equates to opportunity lost. Profit which could have been realized is foregone and perhaps gone to the competitor.

Just-in-time method or “kanban” means keeping the inventory level as needed. Although this is often used in manufacturing, the same principle can be applied in retailing by keeping one’s forecast up to date. The technique is known as “rolling forecast” as actual costs are rolled over as the next month’s forecast. (Kindly click on the image to view the monitored levels of the stock inventory)

January:

Supposing that as of January, the beginning inventory was valued at $1,000 and business started picking up as a result of the promotional discount. The total goods available for the month would be $3,000, comprising the purchase of the $2,000 projection plus the beginning inventory of $1,000.

The total cost of goods sold for the month is worth $2,500 which results in an ending inventory level of $500 worth of goods.

February:

In order to meet the rising demand, the amount of the purchase ordered for February will be based on the actual cost of goods sold of $2,500, as incurred in January, instead of sticking to the original forecast of $2,000. Thus, the total goods available for February will be $3,000 (February purchase of $2,500 plus current inventory balance of $500).

The cash flow statement for the month of February should likewise be adjusted to provide management with an up-to-date figure regarding the amount of cash that the business will be working on for the current month.

Supposing further that the actual cost of goods sold for February is worth $3,000; this means that at the end of the month, the stockroom is depleted. This depicts the understocking scenario, where the entity fails to supply the demand and there will be opportunity lost. Monitoring and timeliness of orders and deliveries should be given utmost attention to avoid such occurrences.

March:

The projected purchase for the month of March should therefore be adjusted to $4,000 instead of the $3,000 originally projected for the month of March. The amount is based on the depleted inventory beginning of $1,000 plus the actual cost of goods sold in February. In using this method, however, management should ensure that:

- The supplier’s services and ability to deliver on demand is bankable.

- The inventory records are reliable.

- The sales records and cash balance show the same proportion of trend in terms of increases.

- The cash flow is up to date with its projections.

April to June:

Adjustments in forecasts should also take into consideration the seasonal demand. Let us presume that by April to June, the sales continue to be robust. Hence, the purchases for these months should also be based on the actual cost of good sold of the previous month plus adjustments in inventory level, if necessary.

Thereafter, due caution should be applied when making forecasts for the succeeding months that are considered “lean”. This is the time of year when most consumers will be saving up for the coming holidays in addition to weather conditions that could bring about negative effects.

Choosing the Right Sources of Credit

Trade credits are granted by suppliers to speed up the rate of their inventory turnover while the early payment incentives are in place to ensure that their own cash position will not be jeopardized by poor collection of receivables. However, be wary of suppliers who tend to put pressure on their customers to increase their purchase orders, on the pretext of pending price increases.

Be forewarned that there are suppliers who make use of future price increases as a marketing strategy. Obviously, it’s a ploy to increase their own sales. Communicate and negotiate instead of simply giving in; or better yet look for other suppliers if you feel you are being pressured into buying more than what you actually need. This emphasizes the need to choose one’s source of trade credit aside from maintaining a good relationship with those who can provide the best services.

Reference Materials and Image Credit Section:

References:

- Short-TermFinancing Chapter 20 – https://webcache.googleusercontent.com/search?q=cache:y0KhojbmvrMJ:www.cob.sjsu.edu/devinc_w/Bus%2520170%2520PwrPts/GA3ECH20.ppt+cost+of+trade+credit&hl=en&gl=ph

Image Credits:

- By Farcaster / Wikimedia Commons

- By Kenneth Allen / Wikimeida Commons

- By Jean-Baptiste Waldner

- Main Credit Ratings.Creative Commons Attribution/Share-Alike License ;/Wikimedia Commons