How do you determine where you should claim the mortgage interest on your rental property to minimize your tax liability? This article will help guide you by covering the Schedule A and Schedule E mortgage interest deductions and when to use each.

Rental Property Benefits

With the 2010 tax season coming right around the corner, it’s important for you to learn how to minimize your liability and maximize your return. If you purchased a rental property, or converted a property to a rental property during the 2010 year, you will have additional forms to fill out. Besides having additional income, there are several other benefits associated with owning and managing rental property. One of those benefits is in respect to your taxes. One question that homeowners may be asking, is can you claim mortgage interest on rental property? The answer is complex, but undeniably yes. Let’s look at some of the benefits of rental properties with respect to taxes.

If you are one of the lucky few who are able to turn a profit on a rental property from the beginning of your holdings then you may find that on your taxes, you will still incur a net loss. Why is this? The reason is that the property itself is a depreciable item and depreciation is considered an expense in regard to rental properties . Depreciation as an expense will work to offset the income you receive from your property. The IRS yearly publishes Publication 527 which details residential rental property taxes, to find the 2009 publication, click here .

To try to explain how you could incur an overall loss, but still have cash in the bank at the end of the year, let’s look at an example. Let’s say that you earn rent of $10,000 for the entire year. Also assume that mortgage payments total $6,000 and maintenance payments come to a total of $500. Altogether, you have offset your rental income by $6,500 leaving you with a profit of $3,500. However after taking into consideration the depreciation of your home over the life of the home, you may find you have $4,000 of depreciation to claim, leaving you with a net loss of $500 ($3,500 - $4,000). So not only do you end up with money in your pocket, but the IRS says your activities on the rental property left you with $500 less of income last year. Counterintuitive, but you’ll take it! That’s $500 less that you have to pay taxes on.

Now, how do you claim all of these expenses and overall losses? Those familiar with itemizing deductions will remember that mortgage interest can be claimed on a Schedule A. However, whether or not you are able to, or will even want to, claim your rental property mortgage interest on a Schedule A will depend on a lot of different factors. So, let’s first take a look at what you can claim on your Schedule A.

Schedule A Interest Deductions

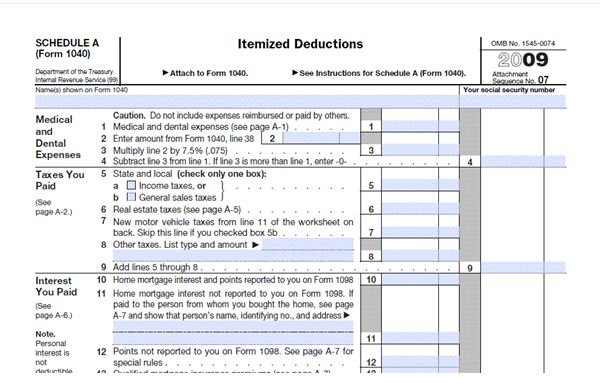

When filing your individual taxes, you may remember that you have the option of itemizing your deductions or taking a standard deduction. If you itemize your deductions, then you will use a form called the Schedule A. When using software or a paid service, this form is typically auto generated for you. For a look at the 2010 tax year Schedule A, click here . On the Schedule A, lines 10 and 11 allow you to deduct mortgage interest as a valid expense paid throughout the tax year being filed. You will receive a 1098 from your financial institution stating how much mortgage interest you paid and can subsequently claim on your tax return. The mortgage interest you are allowed to claim on a Schedule A is mortgage interest for a primary or a secondary home.

There are two cases when you could claim rental mortgage interest on the Schedule A. If your rental property is used for personal use more than 14 days or 10% of the amount of time that it is rented while it is in service as a rental property, then it may be treated as a secondary home. As a secondary home, the mortgage interest can be claimed on a Schedule A. Also, if your home was converted from personal use to a rental property during the year, then the mortgage interest that was paid while it was in service for personal use can be claimed on a Schedule A. If neither of these are the case, then the mortgage interest paid on your rental property would not be claimed on a Schedule A, rather the Schedule E. In most situations, though not all, it is more beneficial for you to claim mortgage interest on a Schedule E. You will want to figure out your final tax liability using both methods, if allowed, before making a final decision. To view the IRS instructions for the Schedule A from 2010, click here .

Tax Implications of a Rental Property

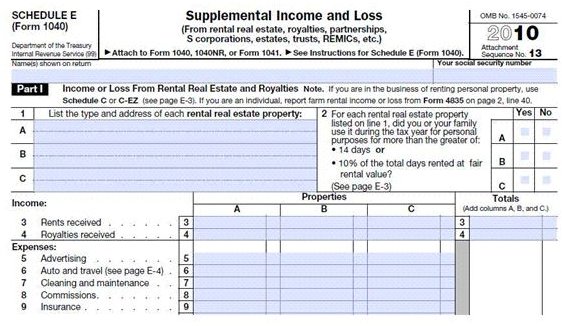

As previously mentioned, when filing taxes for a rental property, the form you will need to use is the Schedule E. In most cases, the Schedule E will offer the best tax benefit for rental property owners. If you lived in your rental property for more than 14 days or 10% of the time it was used as a rental, then you may not claim expenses exceeding income. What this means is that if you incurred expenses of $10,000 but only received income of $5,000 then you can only claim $5,000 of expenses to offset the income. In some cases, it may be more beneficial to treat your rental property as a second home, if it qualifies, and claim the expenses on the Schedule A . The only way to know which way is more beneficial is by calculating your taxes using both methods, and finding out which allows you the most deductions.

If your rental property does not qualify as a secondary home, and was rented for the entire year or the entire time after it was converted to a rental property, then you will need to file a Schedule E to claim the gain or loss that was incurred from your rental activity. To find the Schedule E for 2010, click here . The Schedule E helps you to maximize the amount of expenses that you deduct. Can you claim mortgage interest on rental property with a Schedule E form? Yes, line 12 under Expenses allows you to deduct mortgage interest paid for the rental property. The Schedule E has many other facets, so before you fill the form out and miss some expenses, make sure to read the instructions, here .

Conclusion

When determining whether or not you can claim mortgage interest for a rental property, the answer is undeniably a yes. The answer of where is a complex one depending on your situation. In conclusion, you will fall into one of a few categories:

1. The property was rented for the entire year.

2. The property was converted mid-year into a rental property.

3. The property is a vacation home which may be considered a secondary home or a rental property.

In each of these cases, you will find different answers to the question of where to claim mortgage interest. However, the answer will always be either the Schedule A or the Schedule E.