In the case of consumers making payment arrangements to settle past due debts, do payment arrangements stop credit reporting automatically? As a general rule, the answer to this is “no, they don’t”. There are rules governing credit reports about unpaid debts, which this article explains. Be informed

Understanding the Mechanics of Credit and Credit Reporting

To understand why making payment arrangements to stop credit reporting will not help, the consumer-borrower needs more insight about the mechanics of credit and credit reporting. Here we answer the question, “Do payment arrangements stop credit reporting?”

Basically, a person whose application for credit was approved was considered a responsible borrower. Otherwise, the following conditions apply once a person defaults on his credit payments:

-

If a loan payment becomes delinquent, the lending company’s leverage against the borrower in order to enforce payment is to add interest and late payment charges.

Advertisement -

If, in spite of the late payment fees and interests , the borrower still failed to settle his debt up to the date of maturity, the company classifies the account as past due . This stops the company’s accounting system from accruing interest income that will not be realized .

-

At this point, or before the lender reports the past due account to the credit reporting bureau, the borrower still has the chance to make payment arrangements to stop any credit reporting related to his delinquent loan. Otherwise, lack of any initiative to communicate or make payment arrangements is construed as total abandonment of his obligations as a borrower. The lender then proceeds to submit a past due report to the credit reporting bureau.

Advertisement -

The credit history of a borrower who caused his loan or debt to become past due will carry this information in his credit report for seven (7) years. Any payments made to settle this obligation will only be described as Paid Past Due Loan, in order to properly reflect the borrowers paying habits.

What Happens Next if a Past Due Loan Has Been Reported to the Credit Bureau?

If after six months or an equivalent of 180 days, the borrower still did not make any communications or payment arrangements with the lending company, the latter resorts to the following courses of action:

(1) Write-off or charge-off the unpaid debt as a bad debt account and then submit a report to the credit bureau, containing information that the past due account was charged-off. The credit report now carries the past due amount under the Charged-Off Debt. This has a greater impact on the credit score of the borrower, since it indicates there was no effort to settle the obligation.

(2) The rationale behind the company’s action to charge-off or write off the past due account is to minimize its losses by converting the bad loan into an expense item. As an expense, the company uses the amount as a deduction to its taxable income. This does not mean, however, the loan between the borrower and the lender has been extinguished. The lending company still has the right to enforce collection in every way it can.

(3) If the amount involved is substantial, which depends on the company’s policy on what it considers substantial, a lawsuit can be filed by the lender against the borrower in order to enforce its right to collect the unpaid debt. In this situation, however, the report submitted to the credit reporting bureau provides information about the past due loan or charged-off debt, and the corresponding lawsuit filed in court.

Continuation of section entitled: What Happens Next if a Past Due Loan Has Been Reported to the Credit Bureau?

- The credit bureau carries all this data in the borrower’s report for seven years, counting from the date the account became past due, which is the date when the borrower made his last payment. If the lending company succeeds in collecting the bad debt, any payments received have no effect in the reporting system. The only change that can be expected to take place, relevant to the successful collection of the charged-off debts, is the change of classification from mere “Charged-Off Debt” to “Paid Charged-off Debt”.

(5) Even information about a lawsuit that was withdrawn from court trial proceedings pursuant to an amicable settlement is not removed from the credit report. The lending company merely submits a report to inform the credit bureau that the lawsuit has been withdrawn; hence, the credit report will add the withdrawal information in the borrower’s credit history.

The Fair Credit Reporting Act Guidelines on Payments Made for Bad Debts

Bear in mind, credit reports are furnished in order to provide information and protection to other individuals or entities who consider entering into a contract with an individual. In view of this, the Fair Credit Reporting Act was implemented to ensure that the reporting company, bureau or agency will report only what is fair, true and correct.

Credit-reporting bureaus or agencies are required by law to report factual information as it occurs. The information should be presented in a manner that allows the reader of the report, like banks, investors or employers, to discern easily the paying habits of the individual. There are no provisions in the enactment that allow or recognize payment arrangements entered into with a lender as having the capacity to stop credit reporting.

Removal of information is allowed only after the seven-year or ten-year prescriptive period has expired whereby the information is considered obsolete. That way, those who are trying to reestablish their credit records are given the chance to start with a new slate.

Simply stated, the expirations of the seven or ten year prescriptive periods are the only instances in which previous negative credit reports can be stopped, unless prevented by exceptional cases. Now that you know more about the process, you can answer for yourself the question, “Do payment arrangements stop credit reporting?”

Reference Materials and Image Credit Section

Reference Materials:

- The Fair Credit Reporting Act — https://www.cardreport.com/laws/fcra/fcra.html#605

- How Long Can Bad Credit Remain — https://www.cardreport.com/credit-problems/time.html

- Collection of Bad Debts — https://www.cardreport.com/credit-problems/time.html

Image Credits:

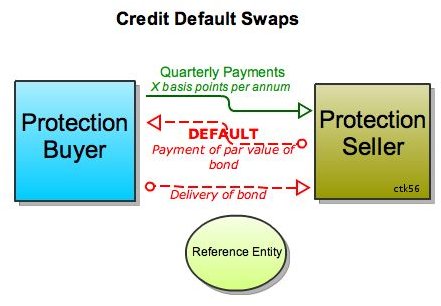

- https://commons.wikimedia.org/wiki/File:Basic _Credit_Default_Swap_(CDS)_diagram.svg

- https://upload.wikimedia.org/wikipedia/commons/c/c3/Main _Credit_Ratings.png

- https://commons.wikimedia.org/wiki/File:Credit-score-chart.svg