Preparing an itemized list of tax deductible medical expenses require thorough knowledge of what medical costs to include. You can also include your spouse’s & your dependents’ medical expenditures. It’s important to know who & what to qualify, so you can

How to Determine Deductible Medical and Dental Expenses

Medical expenses are treatment costs and other health maintenance or health care expenditures you incurred during a particular tax year. These expenses are qualified for inclusion under the itemized deduction method for filing your ITR . However, these expenses could be varied and may include not only yours but also that of your spouse and your dependents. Not only that, there are also conditions to be met when it comes to including your spouse’s or dependents’ medical or health care costs.

Below is a guide to tax deductible medical expenses to serve as an easy reference when sorting out health related costs to include in your Form 1040. However, since all our information was based on IRS Publication 502 for 2009, this guide is subject to changes should the IRS issue a revised publication for medical and dental expenses for the 2010 income tax returns.

Whose medical costs can you include as your tax deductible?

Medical expenses cover treatment costs and expenditures for health betterment, paid by you during the taxable year if the treatment was:

Yours – as the taxpayer; all medical expenditures included in the IRS’s list of allowables..

Your spouse’s –which can be based on any of these conditions:

-

The person whose medical costs you’re claiming is your legally wedded spouse, who may be your joint-filer and dependent at the time of claiming.

Advertisement -

The medical costs you paid for was for treatment costs received by a former spouse at the time when he or she was still your dependent.

-

Ex. Your former wife passed away with some unpaid hospital bills which you were able to settle in full only in 2009. If you remarried in 2009; any medical treatment your new wife receives from 2009 onwards and for as long as you are married, could form part of your joint returns or included as your tax deductible if your spouse will not claim it in a separate return. This means you have two sets of medical expenses to claim for two spouses as dependents for 2009.

Advertisement

That of your dependents’- Each of your dependents may be a child or relative who meet the criteria set forth by the IRS for “qualifying dependents”.The medical expenses you shouldered for their medical and other health treatments during the tax year, qualify as your tax deductibles.

Who qualifies as your dependent child?

Inasmuch as the costs of health and medical services of a dependent child can be included as your tax deductible, the following guidelines should be observed when considering as to who qualifies as your dependent child:

-

Your child/children- who may be a son, daughter, adopted child, foster child or stepchild, provided he or she is below 19 years or younger than you in case the person you are claiming as dependent is not a natural child.

Advertisement -

The child had lived with you for more than six months during the tax year.

-

You have provided more than half of your child’s support during the tax year even if he or she did not live with you during the year in reference. That is, if you and your spouse are legally separated under a decree or under a separation agreement and have lived apart for at least six months during the tax year.

Advertisement -

The child did not provide for his or her own support during the tax year nor filed a return for the said year.

-

Your adopted child received medical attention at the time the adoption became legal .

Advertisement -

The medical expenses of the adopted child being claimed as tax deduction is part of an adoption agreement; to reimburse the adoption agency and was made during the tax year.

-

In the absence of an agreement or documents to substantiate that the cost of the medical service is for your adopted child, you cannot claim said reimbursements as your medical deduction.

Advertisement -

A foster child, adopted child or a stepchild is younger than you and meets all the conditions of your natural child.

-

A foster child, adopted child or a stepchild who is a full-time student, qualifies as a dependent if the person is younger than you and meets all the other conditions of your natural child; although the former may be more than 19 years old but less than 24 years of age.

Advertisement -

A dependent maybe a foster child, adopted child or a stepchild who is younger than you, and meets all the other conditions of your natural child and can be of any age if totally and permanently disabled.

Who qualifies as your dependent relative?

The treatment or health care costs of another group of individuals may be considered as your tax deductibles if he or she belongs to the group of dependents who meet the criteria set forth by the IRS for “qualifying relatives”:

-

Your younger brother, sister, stepbrother, stepsister, nephew, niece, grandchild or any other descending extensions of this generation may qualify as your dependent if they meet all the qualifications of your natural child and provided they were not claimed as dependent by another taxpayer.

-

Qualifications as dependent include those who are less than 19 years old but whose financial support and subsistence are dependent on you as members of your household..

Advertisement

-

Qualifications as dependent include full-time student relatives who had lived with you for more than half of the tax year provided, he or she is not more than 24 years old or did not file any income tax return for the current tax year.

-

Qualifications as a dependent relative include those who are permanently or totally incapacitated to fend for themselves, where impairment may be physical or mental and the individual can be of any age. Provided also that if the support provided is under a Multiple Support Agreement, the amount you claim as tax deductible medical expenses is in accordance with your share under a previously agreed sharing scheme. (See separate explanation for Multiple Support Agreement).

-

Qualifying relatives include your mother, father, grandmother, grandfather, mother-in-law, father-in-law or ancestors whether of lateral or vertical ascent who are still living and relying mainly on you for subsistence and financial support. The amount of claim for medical expenses as tax deductibles under the M_ultiple Support Agreement_, will also apply if the same is true for this group of dependents.

What is a Multiple Support Agreement?

A Multiple Support Agreement is an arrangement between family members to reimburse the main provider of a dependent relative for a portion of the costs he or she incurred to support the qualifying dependent.

-

If such an agreement exists, the main provider of the support will claim as tax deductible only up to the unreimbursed portion.

-

However, the co-providers to this agreement cannot claim any portion of the medical costs regardless of the reimbursement they paid.

-

If the co-providers would like to claim tax deductibles based on their share of the medical costs paid for the dependent relative, payments for the medical expenditures should be done individually in order to qualify the expense as their tax deductible medical expenses.

-

Here is an example of a Multiple Support Agreement where every provider could claim a share of the medical expenses. One sibling will shoulder all medical prescriptions, while another sibling will take care of the medical check-up plus the cost of transportation incurred. Still another will pay for the nurse who monitors the dependent’s health condition. All the minor expenses will be for the account of the main provider. This way, each sibling has proof of the medical expenses they incurred in relation to a family member’s medical treatment. .

What Medical Expenses are Qualified for Inclusion as Tax Deductible?

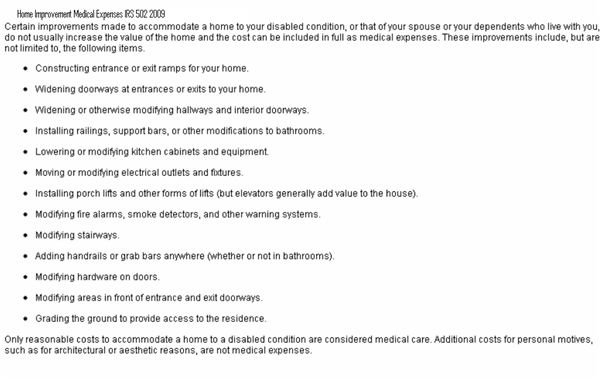

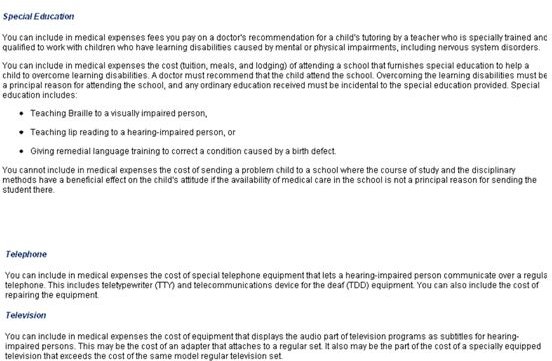

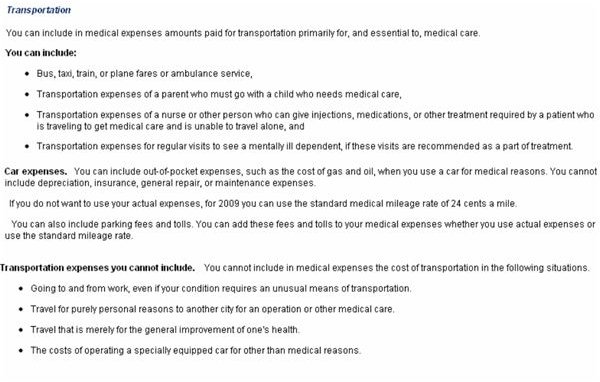

There is a long list of medical expenses you can refer to when determining which of these or how much of your deductibles could be included as expenses. In addition, there are certain expenses that have an equally longer list of specifications as to the type of medical expenses that qualify.

Click on the screenshot images of IRS Publication 502 for 2009, for a list of the includible medical costs as well as several other images that furnish further details about a particular medical expense. This will help you determine which of them will be included in your computation for allowable medical and dental expenses.

How to Calculate the Tax Deductible Medical Expenses

Keep in mind, the first criteria in sorting out medical expense receipts are the dates they were incurred. They should be for the tax year for which these preparations are being made.

Based on the list of allowed tax deductible medical expenses, perform the following:

(1) Make a schedule by listing the date, the receipt number, the nature of the expense and the amount.

(2) Get the sum of all the expense amounts you have listed in the schedule. Double-check the dates and the nature of the expenses.

(3) Deduct any insurance reimbursements received in connection with the medical expenses incurred during the year.

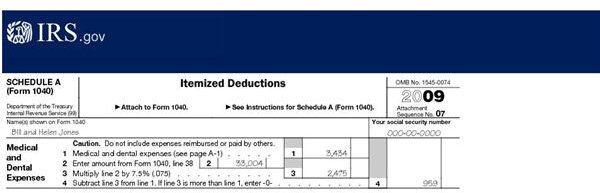

(4) Enter the total net medical expenses on line 1 of Schedule A, Form 1040A.

(5) Fill line 38 with your Adjusted Gross Income or AGI amount.

(6) Multiply the AGI by 7.5% or .075 and enter the result on line 3.

(7) Compare the total medical expenses on Line 1 and the 7.5% threshold limit of the AGI on Line 3; if Line 3 is greater than Line 1, enter zero (0) as the result for line 4

(8) If the amount on Line 1 is greater than the amount on Line 3, simply extract the difference between the two amounts. The resulting figure will be the amount of your medical and dental deduction. Hence, if you have more medical expenses allowable as deductions for your ITR than you were aware of; work along the rules so you can increase your tax deductibles.

There are other more complex scenarios or conditions involving medical and dental expenses. Knowing the allowable tax deductions comes in useful when filing income tax return under itemized deduction method.

The guide to tax deductible medical expenses presented here is only brief and basic since they are subject to future changes in the 2010 IRS Publication. However, the methodology in determining your deductible amount will be basically the same.

Reference Materials and Image Credit Section

Reference Materials:

- https://www.irs.gov/publications/p502/15002q04.html

- https://www.irs.gov/taxtopics/tc502.html

- https://www.irs.gov/publications/p502/ar02.html#en _US_publink1000178863

- https://www.irs.gov/publications/p502/ar02.html#en _US_publink1000179116

Image Credits:

- All images are courtesy of Wikimedia.Commons