There are some good reasons to file for Social Security before the age needed for full benefits. There are also some benefits in delaying filing until older than that age. Making the best financial choice does not require a financial planning expert, but it does mean exploring multiple factors.

Getting Started Online

The U.S. Social Security Administration has a several helpful calculators plus explanations on how to figure your Social Security benefit based on when you retire and how much you have earned over the highest 35 years of income subject to Social Security taxes. The following options exist:

* a worksheet you can do on paper

* a quick online calculator that does not require you to log in to your account

* a detailed calculator downloadable to your computer

* If you are willing to set up online access to your own account, an online calculator will do some figuring based on actual income over your working career.

Links to these are in the Additional Resources section.

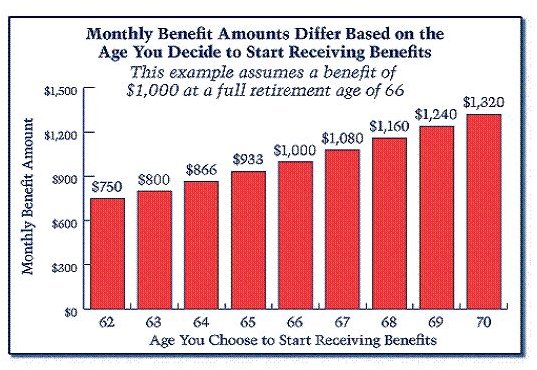

The government website also gives a simplistic example showing that if you start getting benefits at 62, the amount is reduced by 25 percent. If you wait until 70, the benefit is 32 percent more than at the current full retirement age of 66. If you really want to know the full financial impact on your future income under Social Security, using these calculators is only the beginning.

The Basics

The minimum retirement age at which someone could file and get full benefits was 65 for many years. Now, for anyone born between 1943 and 1954, it is 66. For births between 1955 and 1959, the age limit increases by two months for each year. Birthdates from 1960 on set 67 as the minimum age for full benefits.

The easiest way to get an initial estimate comparing retirement choices is the Social Security’s “Quick Online Calculator” (see Additional Resources). This still gives you only a limited rough estimate. Here is one example, based on a person earning $40,000 in the current year who was born in 1950. It takes into account existing projections of Social Security increases. The calculator can show results in current dollars or adjusted for price and inflation increases. The latter option is based on questionable assumptions. It is safer just to use the current dollar method. Based on this for the example, the full retirement monthly income retiring at 66 in 2016 would be $1,277. Retiring in 2012 the amount is $913, 71 percent of the full amount. Wait one more year to claim and the amount jumps to $987, 77 percent of the full amount. If this person waits until 67, the amount is 9 percent more than at 66. By age 70, this individual will get 37 percent more. Nevertheless, anyone who lives out a normal expected life span, based on actuarial tables, will get approximately the same total amount no matter when you begin. It is just the difference between receiving smaller sums for longer times or larger sums for a shorter period.

The Other Factors

All of these estimates by the Social Security Administration are helpful in getting an overall idea of retirement income. What the estimates do not take into account are other factors. These include the time value of money, for instance whether you can save even a small amount of money from retirement income, both Social Security and another pension; the opportunity cost (what is the cost of passing up the next best choice); and your own health status.

If you want to spend the additional time, there are ways to get a better estimate by including these parameters. The coming second part of this series shows how to get a more real-life picture on which to base your decision about when to start drawing Social Security.

Additional Resources

Social Security Quick Calculator

Social Security Detailed Calculator

This post is part of the series: How to Make the Best Decision about When to File for Social Security Benefits

Deciding whether to file for Social Security income at the earliest age, 62, sometime between 62 and full retirement age, now 66, or even a few years later is more than a matter of using the Social Security Administration’s benefits calculator. Use the hints in this series for a more accurate idea.