Some homeowners are still struggling with high interest rates on loan amortizations, since they owe more than the value of their homes due to the 2009 value decline. Get help via HARP or FHA refinancing programs, these are affordable mortgage loan refinance programs to assist qualified homeowner

The Borrower’s Low-Home-Value Dilemma

A mortgage loan refinance became an option that went beyond the reach of borrowers whose properties were affected by the spate of home value decline in 2009. As a result, they ended up owing more than the value of their homes, which automatically rendered them ineligible for the traditional refinancing loans.

Despite today’s prevailing low-interest rates, these homeowners are still struggling to meet their loan obligations because they couldn’t get their interest rates lowered. If you’ve been faced with this dilemma, then it is high time you took notice of the government’s HARP and FHA Short Refinance programs, which expires on June 30, 2012.

Program Overview

The Home Affordable Refinance Program ( HARP)

This is part of the “Making Home Affordable Program” launched by President Barack Obama in early 2009. It aims to help credit-worthy but cash-strapped homeowners qualify for refinancing at the current low-interest rates and obtain a 30 or 15 year mortgage loan despite the decrease in their home’s value.

In addition, the refinanced loan will remain at a stable fixed rate to avoid unforeseen increments in their future monthly amortization through its maturity.

This is new in refinancing since the program requires the lender to include a “Good Faith Estimate” and a “Truth in Lending Statement” in the documentation. These additional documents will detail the borrower’s new interest rate and new schedule of amortization payments as well as the entire amount the borrower will pay through the date of the new loan maturity.

In order to qualify, the HARP program requires that:

- The borrower has stayed up-to-date in paying his existing mortgage loan;

- He or she is still the owner of the property being refinanced.

- The borrower has the capacity to pay the new terms.

- The borrower’s account is secured or guaranteed by Fannie Mae or Freddie Mac as a conforming loan.

As a note, the term conforming loan simply means that it meets the government’s guidelines or criteria, for which the loan limit for a one-unit single-family residence either as a detached home, condo, rowhome or townhome is $417,000.

Homeowners are still advised to evaluate the entire amount of the package and consider if the new terms will give them better benefits when compared to the remaining balance and terms of their current borrowings.

FHA Short Refinance

This program is for borrowers with negative equity; thus, failure to qualify under the traditional refinancing at the current low-interest rates. The FHA Short Refinance provides assistance to borrower-homeowners facing this dilemma by negotiating with the current lender on in behalf of the homeowner.

Lenders are requested to participate in the proposed refinancing scheme, in which the borrower’s first mortgage loan will be converted into an affordable FHA-insured mortgage loan refinance. Under the program, the lender is required to reduce the borrowing to no more than 97.75 percent of the home’s current value.

To qualify, borrowers must meet the following eligibility requirements and conditions:

- The decline in the value of the property resulted in a loan obligation that is more than the property’s current worth.

- The mortgage loan is not currently guaranteed by Fannie Mae, Freddie Mac, FHA, VA or USDA

- The lender is a participant or agrees to participate in this FHA program.

- The borrower is up-to-date with his or her payments.

- The low-value home to be refinanced is the borrower’s primary residence.

- The debt qualifies as a conforming loan.

- The loan obligation does not exceed fifty-five percent of the borrower’s monthly gross income.

- The borrower must not have been convicted of any criminal acts related to or in connection with a mortgage or any real estate transaction fraud, within the last 10 years.

Basic Prerequisites

The HARP may be a new refinancing scheme but the eligibility prerequisites are basically the same. First-time applicants should acquaint themselves with the standard requirements to determine if they’ll qualify for the low rate offers:

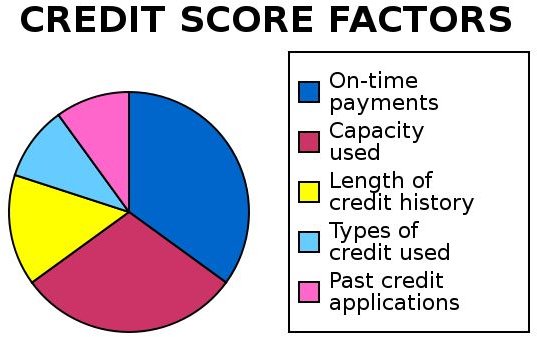

I. FICO credit score of at least 720 or higher.

FICO stands for Fair Isaac & Co., which is the company that developed a credit scoring method to establish a borrower’s ability to pay or a borrower’s credit track record. FICO summarizes a borrower’s credit history into a single number known as his or her credit score and is allowed by the Federal Trade Commission not to disclose the details on how an individual’s credit score is computed .

The accompanying credit reports, on the other hand, contain the following information:

1. The borrower’s credit dealings (if any).

2. The borrower has a good performance as far as settlement of credit is concerned.

3. The borrower pays his or her loan but is “slow”, which means there were instances that payments were made beyond due dates.

4. The borrower has an unsettled debt with a financial institution.

Bases for Credit Score Calculations

-

The amount of default payments and the length of time it took the borrower to settle the defaults.

Advertisement -

The length of time the loan has been outstanding or whether it is still outstanding as of the time of credit checking.

-

How much of the approved loan was taken or availed.

Advertisement -

How long the borrower has been residing in his present place of residence.

-

Other negative credit information such as bankruptcy, charge-offs and collection lawsuits.

-

Important Tips before Submitting the Credit Report:

There are three credit bureaus that furnish credit reports, namely :TransUnion, Equifax, and Experian. The reports are provided free of charge, although a requesting individual has to pay extra if a credit score is to be included.

-

Upon receiving the report, one must check the accuracy of the data. If there are any errors, it is best to get in touch with the issuing bureau and have them correct the error by showing your proof of payment.

-

If the credit information and low credit score are correct, a person may show proof that he or she has improved in his or her paying habits by showing the lender records of one’s most recent credit dealings.

-

Credit scores can be corrected or refuted for as long as the individual concerned can show proof to the credit report bureau and to the lender.

Still, one shouldn’t be too optimistic about getting approved for really low-interest rates if the credit score doesn’t meet the requirement.

2. At L****east Twenty Percent Home Equity

Twenty percent equity means the borrower has already paid at least equal 20 percent or more of the current appraised value for the property being refinanced.

Borrowers with home equity that is below 20 percent can still apply for the low-interest refinancing arrangement by making additional payments on the loan principal. This is one way to meet the disparity between total payments made against the 20 percent equity requirement.

3. Payment of Closing Costs on the Old Mortgage Loan

Refinancing requires the payment of closing costs , which generally include the following:

(1) Application fee, (2) Loan Origination fee, (3) Discount points, (4) Appraisal fee, (5) Title Search fee, (6) Title Insurance fee, and (8) Prepayment Penalty on existing mortgage.

The first three costs depend on the lender’s current policies. It is advisable to ascertain whether the lender guarantees said costs as fixed or subject to changes during the loan processing. Request a written and guaranteed quote regarding the closing costs involved, since they can sometimes reach a hefty amount.

Based on the information furnished here, homeowners whose properties suffered from the 2009 home value decline can determine their eligibility for the government’s HARP and FHA refinance assistance program.

References

- Image: Credit-score-chart by User:Pne/ Wikimedia CCA-SA 2.0 Generic

- Lower Your Rate at Making Home Affordable.Gov – http://www.makinghomeaffordable.gov/programs/lower-rates/Pages/default.aspx

- Image: Subprime Crisis Diagram - X1 by Farcaster/ Wikimedia CCA-SA 3.0 Unported