Bankruptcy, foreclosures and unemployment have made a huge dent in credit scores in recent years, but there are steps to rebuilding credit scores and taking control of our financial future. Taking these steps is well worth the effort to obtain low interest rates on mortgages and personal loans.

Understanding Credit Reports and Protecting your Credit

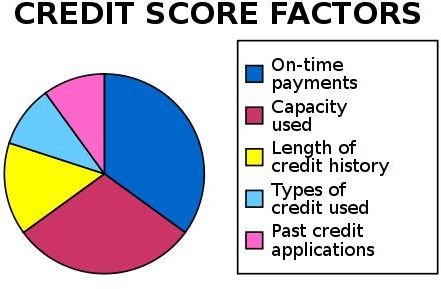

In this section we explain how your credit history is obtained by the three major reporting agencies; Equifax, Experian and TransUnion. We also look at how the information is updated and how your FICO score is determined based on your income-to-debt ratio. Keep in mind that you are only a name on a piece of paper and financial institutions rely heavily on the contents and interpretation of your credit report to determine your credit worthiness.

Credit reports can be wrong, seriously wrong. An error in the reports can cost you thousands of dollars over the length of a mortgage or personal loan and even preclude you from obtaining the home of your dreams or a much-needed form of transportation. Reporting agencies accumulate data provided by companies you do business with, but there are times when those reports are erroneous. It is your responsibility to obtain a free credit report from all three major reporting agencies and immediately request they correct inaccurate information. Also, be aware that someone could be impersonating you and using your social security number and other vital statistics data to get credit in your name and, recklessly, ruin your credit for years to come.

Tip: If you are a teenager, it is important to understand that once your name is on a credit card or debit card, you are beginning to build up a credit history that will follow you for decades. Credit card companies are very adept at getting young teens to sign up for credit cards on college campuses. This often leads to overwhelming debt at a very early age.

-

Your Credit Score: How Is It Determined?

Advertisement -

Protect Yourself: Follow These Steps to Prevent Identity Theft

Advertisement -

The Painful World of Phishing and Identity Theft: What Can You Do About It?

-

How to Manage Money as a Teenager

Advertisement

Build and Improve Your Credit: Use Credit Responsibly

There is a common sense approach to building a solid credit history and working towards improving not-so-stellar numbers. We will show you how to reduce credit card debt and diversify your debt in a way that makes sense so your available credit and debt works to your benefit, not against you. Credit card use is a necessity, but you need to know why you are using plastic and do so responsibly.

Tip: Be careful when asking friends or relatives to add you to their credit history since not having enough information about their own ratings can just as easily impact negatively on you and even harm your employment opportunities.

-

5 Tips: Do You Want a Better Credit Score?

Advertisement -

Advertisement

-

Ethical Use of Credit Reports in the Hiring Process

Advertisement

FICO Scores and Mortgage Lenders

Simply stated, the higher your credit rating, the greater borrowing potential at lower rates. However, when you get your credit report for free, you may not be able to see the FICO score assigned to your credit rating by the three major reporting agencies. It can be maddening getting three different credit ratings, but even more disconcerting getting three different FICO scores and wondering which one the bank used to grant or deny a loan.

Tip: You need to know what your FICO score is and how to get it. Any loan you apply for will take this number into consideration and you want to make sure your loan officer uses your highest numbers. It is easier to negotiate a mortgage rate and terms from a position of strength and save thousands of dollars in interest in the process.

-

Variations in Credit and FICO Scores From Reporting Agencies

Advertisement -

How Do FICO Scores Affect VA Home Loans?

Advertisement -

What Credit Scores Do Mortgage Lenders Want Before They Offer a Prime Loan?

Debt Reduction, Negotiating Debt and Income-to-Debt Ratio

It is important to understand the mix of your credit as seen in a credit report from a lender’s perspective. Lenders want to see a high score and a balance between your take-home pay and monthly debt. While the terminology may seem confusing, the examples provided will ensure that you do the same simple math as it pertains to your finances so you can see what the lender sees.

Tip: Do this before you blindly apply for a loan. It is best to avoid excessive inquiries into your credit report since each “hard pull” on your credit record counts against your credit score by the reporting agencies.

*Note: A hard pull is denoted on your credit report as a process that you started, giving the lender permission to thoroughly look at your credit history. A “soft pull” is a cursory glance, not initiated by you, but typical of lenders who want to make you financial offers. Soft pulls do not go against your credit rating.

Do not be ashamed if you find yourself in a hard financial situation due to accruing monthly debt and the inability to pay. You are not alone. Medical bills are the number one reason for people to claim bankruptcy, lose their homes or be forced to negotiate their existing debts with creditors in order to survive financially. In this section we show you how to negotiate the debt, manage your creditors and explain the confusing tax liability that comes with a short-sale on a house in which the bank forgives part of the debt.

Joint Credit and Cosigning Loans

There are times when debt and poor credit ratings have nothing to do with our own spending, but the financial habits of other people.

Verbal agreements and good intentions mean nothing to debt collectors, the only thing that matters is the name of the people on the signature line on the loan documents. Credit scores can be easily damaged by cosigning for someone’s car loan or by the termination of a marriage if we are not careful.

Tip: Do not cosign a loan unless you know exactly what you are getting into and are willing to pay off the loan yourself in case the other party does not meet your expectations. Examine how cosigning with another person affects your credit score and how your credit score affects them.

People of wealth routinely sign prenuptial agreements to protect their assets in the event of a divorce; you may not want to go that far, but you do need to be aware of your spouse’s current financial spending and saving habits. Take a good look at each other’s credit reports to assess if combining credit or having separate credit histories would work out better in the long run.

How Is Your Credit?

Your credit and FICO scores are only a window to your finances. You know if you need to save more or need to borrow money to consolidate debt at lower interest rates. If you need information to borrowing money, feel free to browse our Guides to Obtaining Personal Loans and Low Interest Rates in order to make an informed decision that works for your lifestyle and current financial situation.

Please feel free to share your financial successes or post any questions we have not answered in the Comments section below.

References

-

Images:

Cosigning a Loan by vichie81 / FreeDigitalPhotos.net

Calculating Debt by Michelle Meiklejohn / FreeDigitalPhotos.net

FICO by FICO [Public domain ]

Credit Score by User:Pne CC-BY-2.0 via Wikimedia Commons